PEO vs Broker: What's Right for Your Business

PEO vs Broker: What's Right for Your Business

At a Glance: Professional Employer Organizations (PEOs) and brokers both offer employee benefits to businesses. When evaluating these options, you'll need to consider cost (both obvious and hidden), service level requirements, and your specific business needs. The "right" choice varies significantly based on your company size, growth trajectory, internal capabilities, and risk profile.

One of the most important decisions that small business owners and HR professionals will make regarding employee benefits is how to structure and purchase your health insurance. This choice often comes down to two primary options: working with a

Professional Employer Organization (PEO) or partnering with an

insurance broker. Understanding the differences between these approaches can save your company thousands of dollars annually while ensuring your employees receive the coverage they need.

The decision between a PEO and broker affects more than just your insurance premiums. It impacts your HR operations, compliance responsibilities, administrative burden, and long-term flexibility. As healthcare costs continue to rise and regulatory requirements become more complex, making the right choice becomes increasingly critical for your business's success and your employees' satisfaction.

What's the Difference Between a PEO and a Broker?

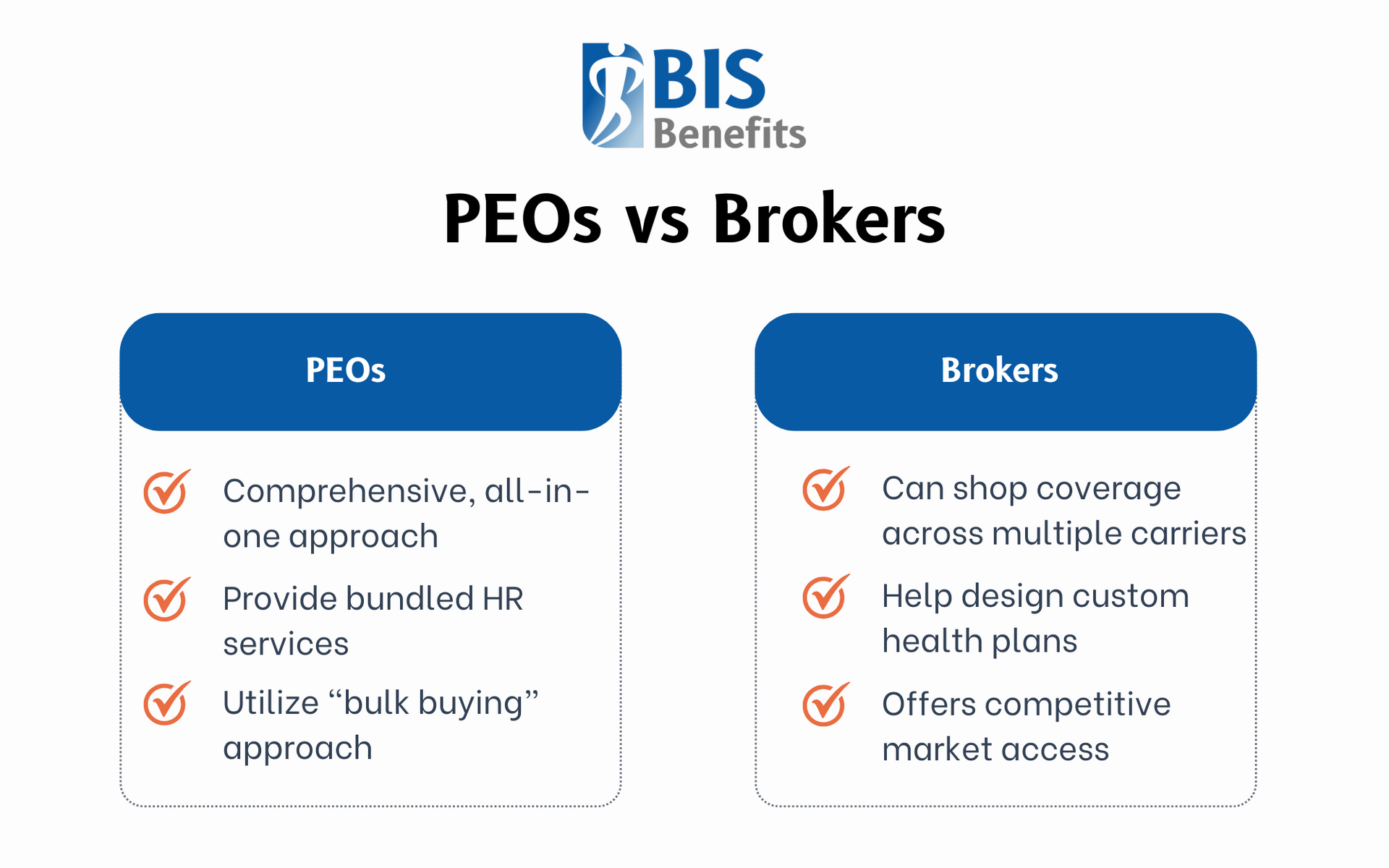

The fundamental difference between PEOs and brokers lies in their relationship with your business and the scope of services they provide. Startups and very small businesses often gravitate toward PEOs for their comprehensive, all-in-one approach, while growing companies with dedicated HR staff typically prefer the flexibility and control that brokers offer.

Professional Employer Organizations (PEOs)

A PEO becomes your professional co-employer, providing bundled HR services including:

- Payroll Processing

- Benefits Administration

- Workers' Compensation

- Regulatory Compliance Under a Co-Employment Arrangement

This means you share legal responsibility for your employees with the PEO, though you maintain control through daily operations.

Many business owners first encounter PEOs through their payroll companies. Major providers like

ADP and

Paychex often expand their relationships by offering PEO services to existing payroll clients. The transition feels natural since you're already working with them for payroll processing.

The "leasing" of your tax ID is a critical concept to understand with PEOs. Your employees become part of a larger group under the PEO's master tax identification number for insurance and benefits purposes, allowing small groups to access benefits typically available only to larger organizations.

Brokers and Agents

Most of the time, insurance brokers operate as independent advisors who help you navigate the complex world of employee benefits without any co-employment arrangement. They maintain relationships with multiple insurance carriers and can shop your coverage across various providers to find the best fit for your company's needs.

As independent insurance professionals, brokers are compensated through commissions paid by insurance companies, not through monthly fees charged to your business. This compensation structure means brokers have incentives to find you appropriate coverage that you'll maintain long-term.

Brokers provide direct access to multiple insurance providers, including major carriers like

UnitedHealthcare,

Anthem, and

Aetna. They can provide customized quotes based on your specific employee demographics, claims history, and risk factors.

How Each Model Works

The PEO Model in Practice

PEOs operate on a comprehensive service model that handles multiple aspects of human resources under one roof. They create a one-stop solution for business owners who want to focus on their core business operations by managing:

- Payroll Processing

- Benefits Administration

- Workers' Compensation Insurance

- HR Compliance Requirements

The co-employment structure means you share legal employer responsibilities with the PEO. While this might sound concerning, you retain control over hiring, firing, compensation decisions, and day-to-day management. The PEO handles the administrative and compliance aspects of employment.

PEOs bundle your employees with larger groups under their master tax identification number for insurance purposes. This "bulk buying" approach can potentially reduce costs by spreading risk across thousands of employees from multiple companies. However, health insurance pricing doesn't always follow traditional bulk purchasing rules.

The risk pooling aspect means your 15-person company's health insurance rates are calculated based on the health status and claims experience of potentially 10,000+ employees across hundreds of different companies. This can work in your favor if your group has higher-than-average health risks, but it may result in higher costs if your employees are young and healthy.

The Broker Model in Practice

Brokers focus specifically on insurance and benefits without providing payroll or comprehensive HR services. They help you design custom health plans by shopping across multiple carriers to find the best combination of coverage, network access, and pricing for your specific group.

You remain the sole employer under the broker model, maintaining complete control over all employment decisions and HR policies. The broker serves as your trusted advisor and advocate, providing ongoing support in dealing with insurance companies, but your business retains full autonomy over employee relationships.

Individual company rating means your health insurance premiums are based exclusively on your employees' demographics, health status, and claims history. A company with 25 healthy employees in their twenties and thirties could potentially secure significantly better rates than they would get through a PEO.

Company Factors & Differences to Know

It's important to remember that paying more is not always a poor decision. Factors like business size, cost needs, and risk profiles can play an important role in selecting the right PEO or broker for your business.

Key Decision Factors

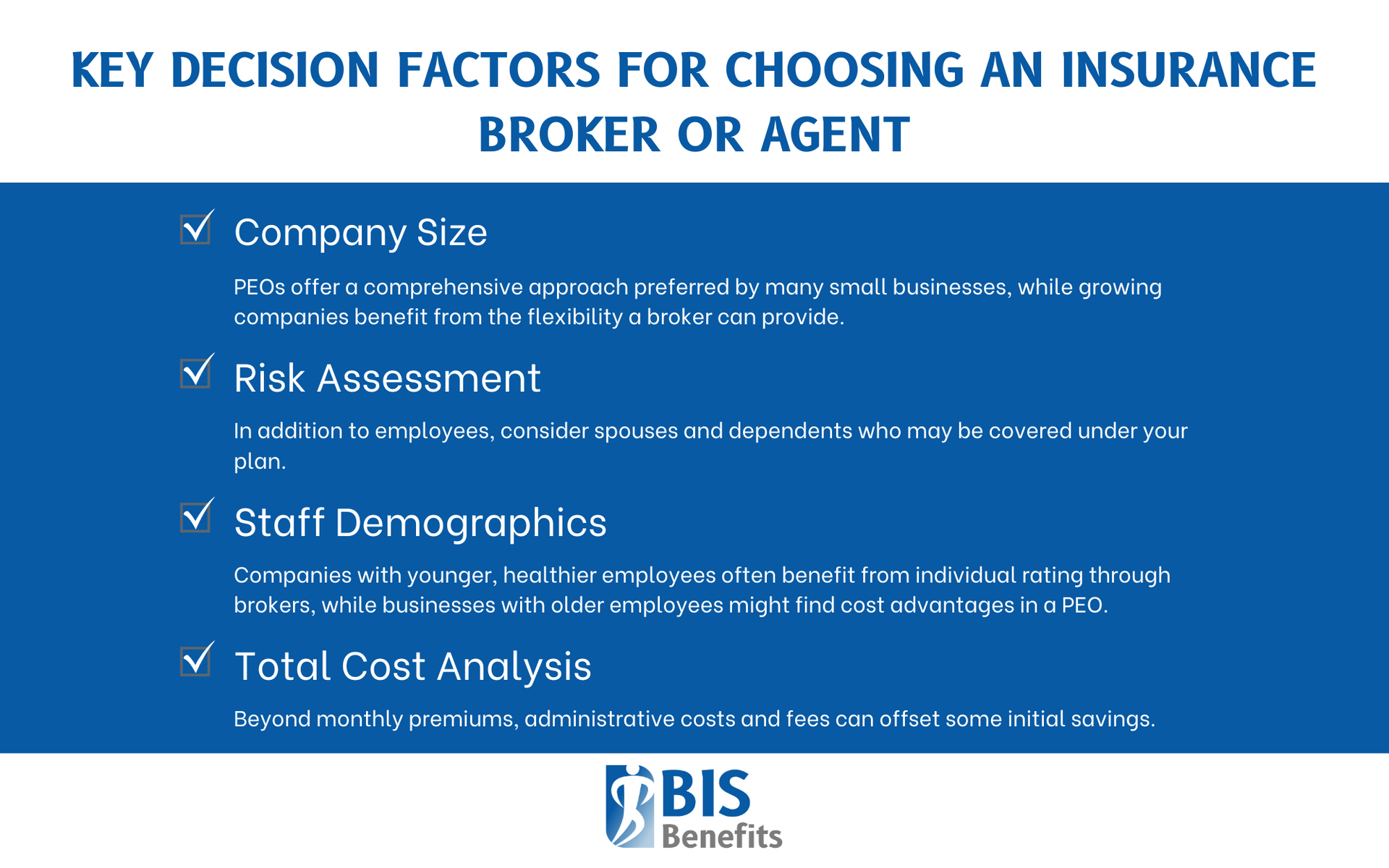

- Company Size and Demographics: The size and makeup of your workforce significantly impact which model works better. Companies with younger, healthier employees often benefit from individual rating through brokers, while businesses with older employees or those with known health issues might find cost advantages in PEO risk pooling.

- Risk Assessment: Understanding your group's health risk profile is crucial. Consider not just your employees' apparent health status, but also their spouses and dependents who may be covered under your plan.

- Total Cost Analysis: Look beyond just monthly premiums. PEO fees can range from $5 to $180+ per employee per month, depending on the services included. These administrative costs can quickly offset any premium savings.

Critical Differences to Understand

- HR Services: PEOs provide comprehensive HR support including compliance assistance, employee handbooks, and guidance on employment law issues. Brokers focus exclusively on insurance and benefits.

- Benefits Access: PEOs offer pooled benefits that may include access to larger group rates but limit your plan customization options. Brokers provide tailored solutions designed specifically for your workforce.

- Employment Structure: PEOs create a co-employment relationship that some business owners find confusing. Brokers maintain your status as the sole employer.

- Flexibility: PEOs typically offer limited plan options from their preferred carriers. Brokers can access the entire market, providing maximum flexibility in plan design and carrier selection.

Pros & Cons

- PEO Pros: PEOs provide operational simplicity through bundled services, built-in compliance support that reduces legal risks, and potential cost savings for small teams or high-risk groups. Additionally, they offer access to enterprise-level benefits that small companies typically cannot access independently.

- PEO Cons: Under a PEO system, you have reduced control over HR policies and benefit plan design, potentially higher or less transparent total costs when fees are included, and co-employment arrangements that some business owners find complicated.

- Broker Pros: Brokers offer maximum flexibility in plan design and carrier selection, competitive pricing through market access, and retention of full control over all employment and HR decisions. Brokers also provide specialized expertise focused specifically on insurance and benefits.

- Broker Cons: With a broker you must handle HR functions separately, compliance support varies by provider, and manage relationships with multiple vendors.

Making the Right Choice for Your Business

Before making this decision, ask yourself what HR services you actually need and how important convenience is versus cost savings and control. Consider your company's growth trajectory and whether your current choice will still make sense in two or three years.

Choose a PEO if:

You have no internal HR capabilities and need comprehensive support beyond just benefits administration.

PEOs work particularly well for smaller companies under 25 employees that want convenience and are scaling rapidly. Companies with high-risk employee populations that might benefit from risk pooling should also consider PEOs.

Choose a Broker if:

You want maximum flexibility in plan design and carrier selection, or you already have HR capabilities in place and only need benefits expertise.

Brokers typically work better for companies outgrowing the PEO model, those with low-risk demographic groups that benefit from individual rating, and businesses prioritizing cost optimization and specialized expertise over convenience.

Implementation and Ongoing Management

Before making a final decision, think about your business’s needs and ask yourself the following questions:

- Do we need comprehensive HR services or just benefits help?

- Are we comfortable with co-employment?

- Do we want control over our benefits package design?

- What's our long-term growth plan?

After making a decision, conduct regular analysis through annual or biannual reviews to ensure your current arrangement still makes sense. Market conditions, your company's risk profile, and available options change over time.

The choice between PEOs and brokers isn't permanent, and the right answer for your business today may change as you grow. Focus on understanding your business's unique needs, evaluating total costs including hidden fees, and working with providers who prioritize your long-term success over their short-term profits.

Find a Commercial Insurance Solution with BIS Benefits

Good brokers will sometimes suggest PEO arrangements when appropriate, and reputable PEOs should acknowledge when companies have outgrown their model so their client can make an informed decision for their business. Working with honest professionals who may recommend the alternative when appropriate helps you prepare for the future, regardless of what state your business is currently in.

At BIS Benefits, we take the time to understand your industry-specific risks, employee makeup, budget, and future goals. Our brokers help companies create a tailored strategy to ensure the right coverage for their business needs. If your company is based in the Metro Atlanta area,

give us a call to find out what our

Group Health Insurance and

Business Insurance brokerage services can do for you.