Are Health Insurance Payments Tax-Deductible?

Are Health Insurance Payments Tax-Deductible?

At a Glance: Health insurance payments are often tax-deductible, but the rules depend on your employment status, how you obtain coverage, and whether premiums are paid pre-tax or after-tax. Premiums already paid pre-tax through an employer or subsidized by premium tax credits cannot be deducted again.

Health insurance is one of the largest expenses for many individuals and businesses in the United States, which makes it important to understand whether those payments can reduce your tax burden. The deductibility of health insurance payments depends on several factors, including how coverage is obtained, employment status, and how premiums are paid.

In many cases, health insurance payments are deductible, but the rules vary based on individual circumstances. Understanding the tax treatment of health insurance premiums is essential for individuals, self-employed workers, and business owners who want to maximize their tax benefits.

Understanding Health Insurance Tax Deductions

Health insurance premiums may be deductible depending on your circumstances. Tax treatment varies for employees, self-employed individuals, and business owners. The method of payment (pre-tax deduction vs. after-tax deduction) significantly affects deductibility. Federal and state tax rules may also differ, so understanding the rules that apply to your situation helps maximize tax benefits.

Deductibility is important because it reduces taxable income and overall tax liability. For those with high premium costs, deductions can result in significant tax savings. The ability to deduct health insurance also affects financial planning and budgeting for medical care and is an important consideration when choosing how to obtain coverage.

When Health Insurance Payments Are Deductible

Itemized Medical Expense Deduction

Taxpayers who itemize deductions can deduct medical expenses that exceed 7.5% of their adjusted gross income (AGI). Health insurance premiums count toward total medical expenses, including premiums for medical, dental, and long-term care insurance. To claim this deduction, you must use Schedule A and itemize deductions rather than taking the standard deduction. Other qualifying medical costs such as copays, prescriptions, and out-of-pocket expenses can be combined with premiums to reach the 7.5% threshold.

Business Deduction for Employer-Paid Premiums

Employers can deduct health insurance premiums paid for employees as a business expense. These premiums are deductible as ordinary and necessary business expenses, reducing business taxable income. This applies to corporations, partnerships, and sole proprietors with employees. Businesses with less than 25 full-time equivalent employees may be eligible for the Small Business Health Care Tax Credit, which can be worth up to 50% of the cost of employees’ premiums.

Self-employed individuals without employees can use the

Self-Employed Health Insurance Deduction.

Health Savings Account (HSA) Contributions

Contributions to an HSA are tax-deductible or made pre-tax through payroll deductions. HSA funds used for qualified medical expenses are tax-free, providing a triple tax advantage: deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses. To contribute to an HSA, you must be enrolled in a qualified High-Deductible Health Plan (HDHP), and annual contribution limits apply.

Health Reimbursement Arrangement (HRA) Benefits

Employer contributions to HRAs are tax-deductible for the business, and reimbursements to employees are tax-free. Employees cannot deduct expenses reimbursed through an HRA since they have already received a tax benefit. Multiple HRA types are available, including Qualified Small Employer HRAs (QSEHRA) and Individual Coverage HRAs (ICHRA), each with different rules and benefits.

When Health Insurance Payments Are Not Deductible

Pre-Tax Premium Payments

Premiums paid through employer pre-tax payroll deductions are not deductible on your tax return. These premiums already reduce taxable income before taxes are calculated, so you cannot claim an additional deduction for amounts already excluded from taxable income. This is common with employer-sponsored cafeteria plans (Section 125 ). Double deductions are not permitted under tax law.

Premium Tax Credit Recipients

Individuals receiving Affordable Care Act premium tax credits cannot deduct the subsidized portion of their premiums. Only the amount paid out-of-pocket after credits may be deductible. This applies to coverage purchased through the health insurance marketplace, and you must account for advance premium tax credits received during the year when calculating any potential deduction.

Premiums Paid by Employer

Employer-paid premiums are not deductible by the employee. Employer contributions are excluded from the employee's taxable income, meaning the employer takes the business deduction while the employee receives a tax-free benefit. Employees can only deduct their own after-tax premium contributions, not amounts paid by the employer on their behalf.

Certain Types of Coverage

Some types of insurance premiums are not deductible:

- Premiums for policies that pay fixed amounts regardless of medical expenses, such as some indemnity plans, may not qualify

- Cosmetic surgery insurance premiums are generally not deductible

- Premiums for coverage that does not qualify as medical insurance under Internal Revenue Service (IRS) rules cannot be deducted

- Some supplemental policies may also have limited deductibility

Standard Deduction Filers

Taxpayers who take the standard deduction cannot claim the itemized medical expense deduction. The medical expense deduction is only available when itemizing on Schedule A. However, the Self-Employed Health Insurance Deduction is still available as an above-the-line deduction even if you take the standard deduction. You must compare the standard deduction versus itemizing to determine the best approach for your situation.

Deduction Methods Explained

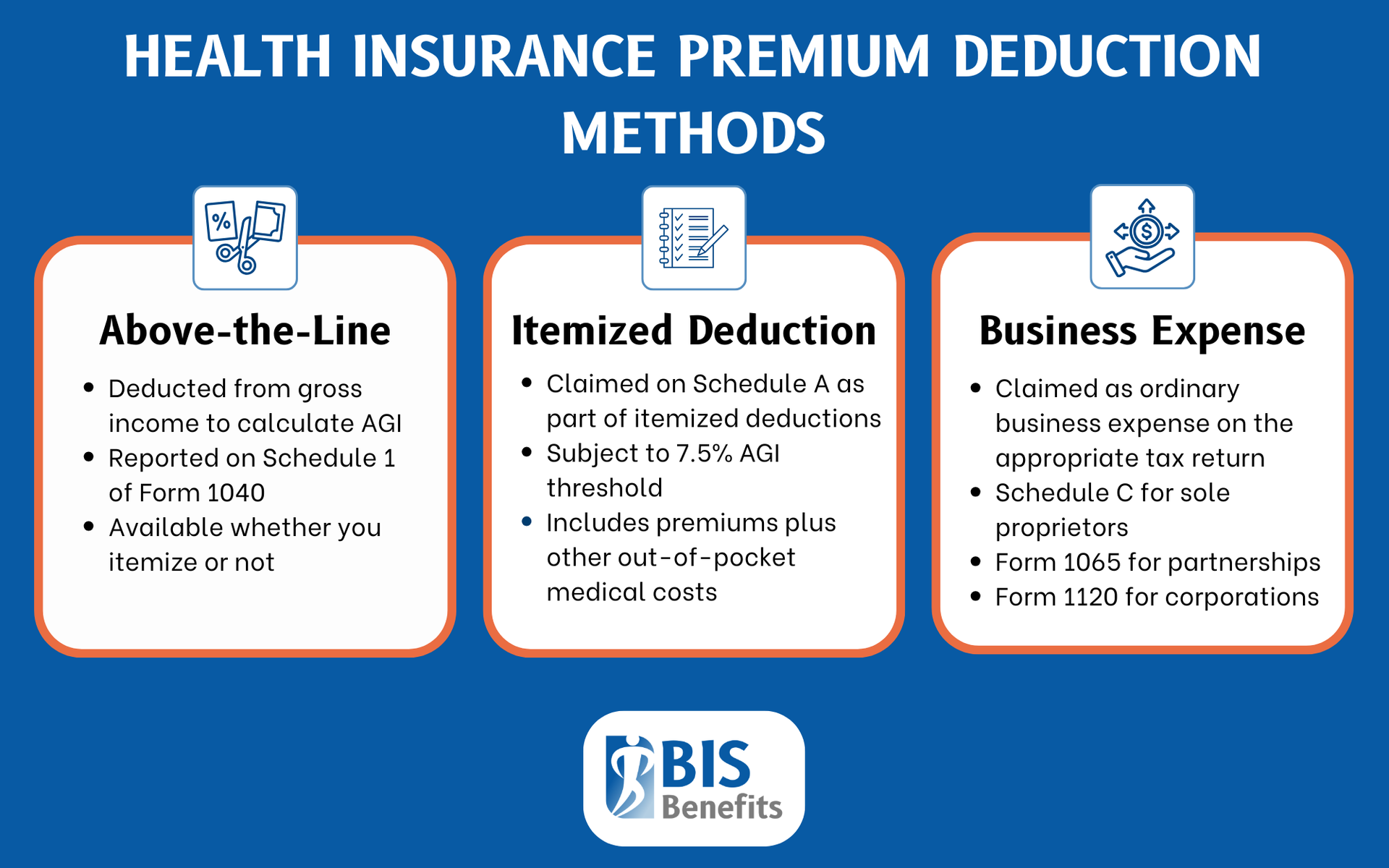

Above-the-Line Deduction

Self-employed individuals can deduct health insurance premiums as an adjustment to income, which is deducted from gross income to calculate AGI. This above-the-line deduction is available regardless of whether you itemize and is reported on Schedule 1 of Form 1040. Because it directly reduces AGI, it can also affect eligibility for other tax benefits. This is the most advantageous method when available.

Itemized Deduction

Medical expense deductions are claimed on Schedule A as part of itemized deductions and are subject to the 7.5% AGI threshold. This method is only beneficial if your total itemized deductions exceed the standard deduction. It requires tracking and documenting all qualifying medical expenses and includes premiums plus other out-of-pocket medical costs.

Business Expense Deduction

Business expense deductions are claimed as ordinary business expenses on the appropriate business tax return:

- Schedule C for sole proprietors

- Form 1065 for partnerships

- Form 1120 for corporations

This deduction reduces business taxable income and is available for premiums paid on behalf of employees. It is subject to standard business expense rules and documentation requirements.

How to Claim Health Insurance Deductions

Gather Documentation

To claim health insurance deductions, start by putting together documentation. Maintain records for at least three years in case of an audit.

- Records of all premium payments

- Form 1095-A (if coverage was purchased through the marketplace)

- Receipts and statements from insurance carriers

- Documentation of other medical expenses if you are itemizing

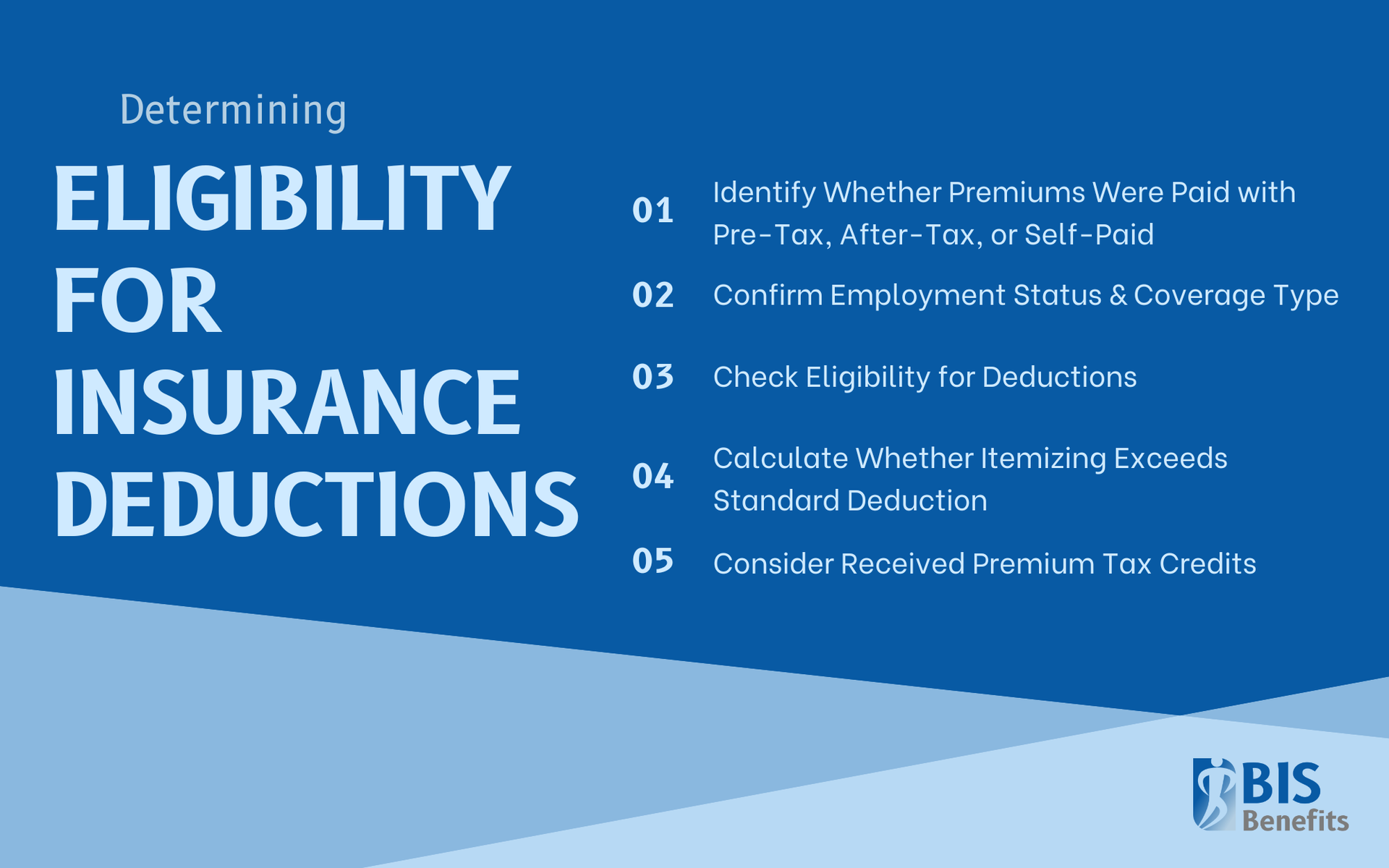

Determine Eligibility

- Identify how premiums were paid (pre-tax, after-tax, or self-paid)

- Confirm your employment status and type of coverage

- Check eligibility for the self-employed health insurance deduction

- Calculate whether itemizing exceeds the standard deduction

- Consider any premium tax credits received

Talk to a Professional

Complex situations benefit from professional guidance. Tax rules change frequently and vary by situation, and professionals can identify maximum deductions while helping you avoid errors that could trigger audits. Investing in professional advice is often worth it for significant tax savings.

Common Mistakes to Avoid

Double Deductions

You cannot deduct premiums already paid pre-tax, employer-paid portions, or amounts covered by premium tax credits. Review your pay stubs to determine whether payments were made pre-tax or after-tax before claiming any deduction.

Missing Available Deductions

Self-employed individuals may overlook their above-the-line deduction, itemizers may forget to include all qualifying medical expenses, HSA contributions may not be maximized, and long-term care premiums may be overlooked. Review all potential deductions carefully.

Poor Recordkeeping

The IRS may disallow deductions without proper documentation, so keep premium statements, cancelled checks, and receipts organized by tax year. Good records support your deductions if questions arise.

Next Steps

Health insurance payments are often deductible, but the rules depend on employment status, how premiums are paid, and whether you itemize deductions. Premiums paid pre-tax or by an employer are not deductible since they already provide tax benefits. Understanding your specific situation is key to maximizing available deductions.

Consulting with a health benefits professional helps ensure you are taking advantage of all available health insurance deductions based on your individual circumstances. At BIS Benefits, we serve businesses in Georgia with at least 15 employees looking for insurance plans that fit their specific needs.

Request a Quote today to receive an estimate from our brokers.