What Does Commercial Auto Insurance Cover?

What Does Commercial Auto Insurance Cover?

At a Glance: Commercial auto insurance covers liability for injuries and property damage your business vehicles cause to others, optional physical damage protection (comprehensive and collision) for your own vehicles, medical payments for drivers and passengers, and uninsured/underinsured motorist coverage. These costs are influenced by factors including vehicle type, business operations, driver qualifications, and selected coverage limits.

Commercial auto insurance provides coverage for businesses that use vehicles in their daily operations, including liability, physical damage, and specialized risks that personal auto policies exclude. Unlike personal auto insurance, which is designed for individual commuting and personal use, commercial policies address the unique exposures businesses face when vehicles serve as tools for generating revenue, transporting goods, or providing services to customers.

In the United States, businesses operating vehicles must carry

minimum liability coverage, though state minimums rarely provide adequate protection for the assets and earning capacity most businesses need to safeguard. Understanding what commercial auto insurance covers enables business owners to make informed decisions about protection levels and avoid paying for unnecessary coverage or leaving dangerous gaps in protection.

Basic Commercial Auto Coverage Components

Liability Coverage

Bodily Injury Liability

This is the foundation of commercial auto insurance, paying medical expenses, lost wages, and pain and suffering when your business vehicles cause injuries to others. This coverage extends to pedestrians, occupants of other vehicles, and anyone injured by your vehicle's operation, protecting against potentially devastating personal injury claims that could otherwise bankrupt your business.

Property Damage Liability

This covers repair or replacement costs when your vehicles damage others' property, including other vehicles, buildings, fences, or any other tangible property. State minimum requirements establish baseline coverage levels, but these minimums often prove inadequate for serious accidents. Many businesses carry liability limits of $1 million or more to protect substantial business assets and future earning capacity.

Legal Defense Costs & Settlement Coverage

Commercial auto policies typically cover attorney fees, court costs, investigation expenses, and settlement negotiations, which can equal or exceed actual damage awards. This defense coverage applies even when claims prove groundless, protecting businesses from frivolous lawsuits that still generate substantial legal expenses.

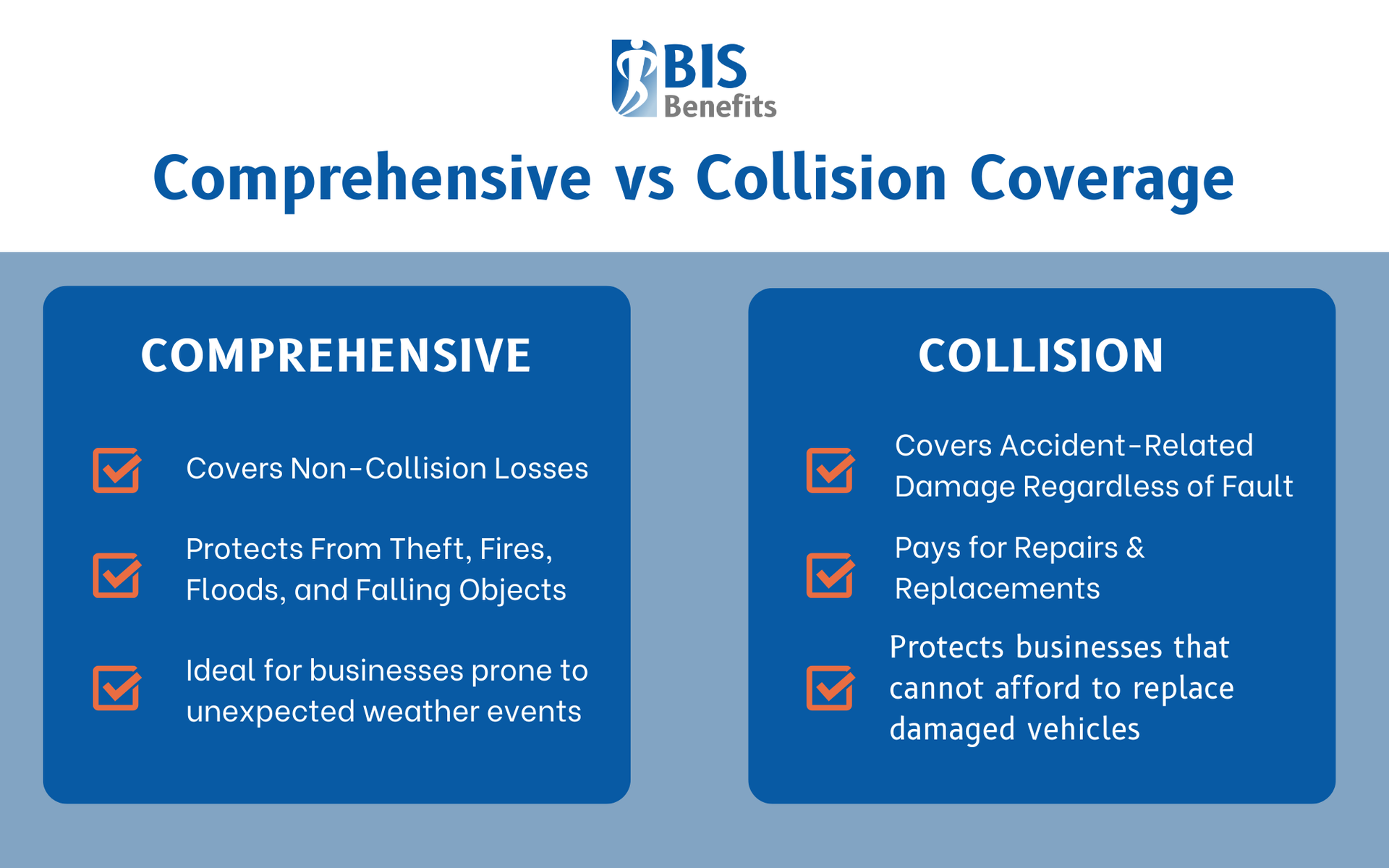

Comprehensive Coverage

Comprehensive coverage protects your vehicles against non-collision losses, including-

- Theft

- Vandalism

- Fire

- Flood

- Hail Damage

- Falling Objects

- Animal Collisions

This coverage proves particularly valuable for businesses operating in areas prone to weather events or vehicle theft, providing financial recovery when unexpected events damage or destroy company vehicles.

Collision Coverage

Collision coverage pays for accident-related damage regardless of fault, repairing or replacing vehicles damaged in crashes with other vehicles, fixed objects, or rollover accidents. While optional in most states, collision coverage provides essential protection for businesses that cannot afford to replace damaged vehicles from operating funds.

Deductible Selection

In most cases, higher deductibles reduce premiums while increasing out-of-pocket expenses when claims occur. Businesses must balance immediate affordability against potential claim costs, considering factors like financial reserves, fleet size, and loss history. Actual cash value settlements account for depreciation, while agreed value coverage guarantees specific payouts regardless of depreciation, though at higher premium costs.

Medical Payments

Medical payments coverage provides immediate payment for medical expenses incurred by drivers and passengers in covered vehicles, regardless of who caused the accident. This no-fault coverage pays for emergency treatment, hospital stays, surgical procedures, and follow-up care up to policy limits, typically ranging from $1,000 to $10,000 per person.

Personal Injury Protection

Personal Injury Protection (PIP) offers broader coverage than medical payments, including lost wages, replacement services for household tasks the injured person cannot perform, and funeral expenses in fatal accidents. State requirements for PIP vary dramatically, with some states mandating coverage while others make it optional or unavailable.

Coordination with health insurance and workers' compensation prevents duplicate payments while ensuring injured parties receive appropriate coverage. Commercial auto policies typically specify whether they provide primary or secondary coverage relative to other available insurance, affecting how claims are processed and paid.

Uninsured and Underinsured Motorist Coverage

Despite legal requirements for auto insurance, millions of drivers operate without coverage, leaving businesses vulnerable to uncollectible damages without uninsured motorist protection. Underinsured motorist coverage applies when at-fault drivers carry insurance insufficient to cover your full damages. As medical costs and vehicle values increase, state minimum liability limits often prove inadequate for serious accidents, making this coverage increasingly important for adequate protection.

Hit-and-Run

If an unknown driver flees the scene of a collision, the accident coverage falls under uninsured motorist provisions, protecting businesses when unknown drivers flee accident scenes. This coverage applies to both bodily injury and property damage components, depending on policy structure and state regulations.

Types of Vehicles Covered

Business-Owned Vehicles

Cars, trucks, and vans owned by the company receive straightforward coverage under commercial auto policies, with protection extending to all vehicles listed on the policy declarations page. Specialized vehicles, including delivery trucks, service vehicles, and equipment haulers, require accurate description and valuation to ensure appropriate coverage limits.

Vehicle Fleets

Multiple unit coverage provisions enable businesses to add and remove vehicles throughout the policy term without individual policy amendments for each change. Newly acquired vehicle automatic coverage provides immediate protection for additions to your fleet, typically for 30 days while you formally add vehicles to the policy.

Hired and Rental Vehicle Coverage

Short-term vehicle rentals for business use receive coverage through hired auto provisions, protecting businesses when employees rent vehicles for business trips, temporary replacements, or special projects. Leased vehicles and long-term rentals may require specific listing on policies depending on lease duration and contractual requirements.

Employee rental car coverage while traveling extends protection to rental vehicles employees use for business purposes, preventing gaps between personal auto policies that exclude business use and commercial policies that might not automatically cover rentals.

Non-Owned Vehicle Coverage

Employee personal vehicles used for business create liability exposure for employers even though the business doesn't own the vehicles. Non-owned vehicle coverage provides contingent liability protection when employee personal auto policies prove insufficient to cover accident damages.

Temporary use of other people’s vehicles receives protection through non-owned provisions, covering situations where employees borrow vehicles for business errands or use vehicles provided by clients or vendors. This employer liability protection proves essential for businesses whose employees regularly drive for work without using company vehicles.

Specialized Commercial Auto Coverages

Motor Truck Cargo Coverage

Motor truck cargo coverage pays for damaged or stolen goods during transportation, with coverage extending through loading and unloading operations that present heightened loss exposure. This provides protection for goods in transit and addresses the substantial liability businesses face when transporting customer property or inventory.

Garage Coverage and Transportation Services

Auto dealers and repair shop protection requires specialized garage coverage addressing unique exposures including customer vehicle custody, service operations, and sales activities. This coverage protects customer vehicles while in your care, custody, or control, whether for service, storage, or display.

Public & Livery Services

This coverage serves taxi, rideshare, and limousine operations with specialized provisions addressing passenger liability and commercial transportation requirements. These policies must satisfy airport and municipal licensing requirements while providing adequate protection for unique passenger transportation exposures.

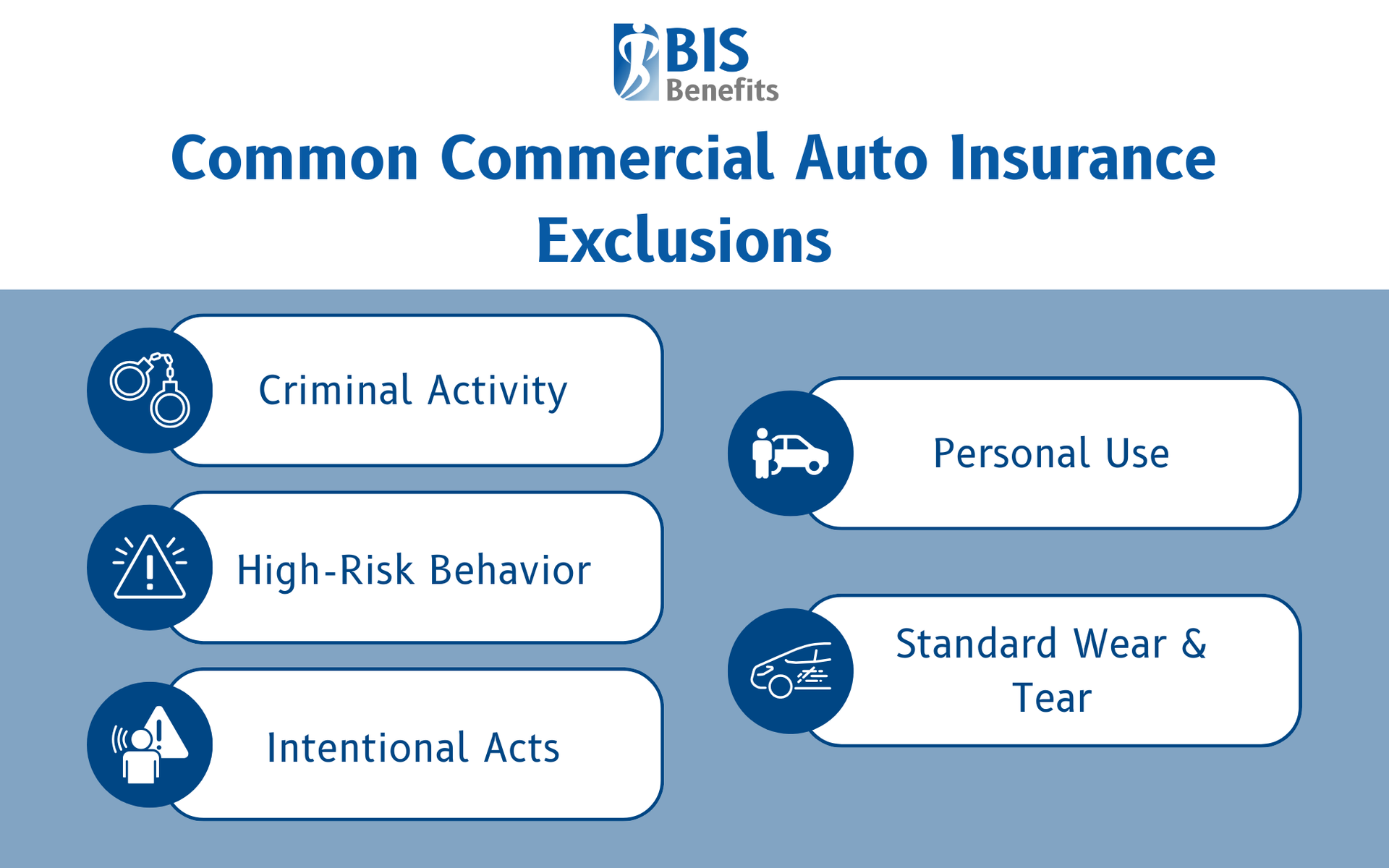

Understanding Coverage Limitations

Understanding the limitations of commercial auto plans prevents unpleasant surprises when claims occur under excluded circumstances. Most policies exclude-

- High-Risk Behavior: Racing, off-roading, competitive events, and other reckless actions

- Intentional Acts: Damages that are expected or intended by the insured

- Criminal Activity: Damages that occur while an employee is breaking the law, including driving under the influence

- Personal Use: Injuries or damages that occur while an employee is using a company car for personal use

- Ineligible Wear & Tear: Standard damages that falls outside insurable risk parameters

- Business-Specific Exclusions: pollution liability, products liability during transportation, and professional services liability often require separate coverage

- Geographic & Use Limitations: Personal use of commercial vehicles, out-of-territory operations, and unauthorized drivers are usually not covered

Factors Affecting Coverage Costs

Some business operations factors that affect commercial auto insurance premium costs include-

- Vehicle Characteristics (Type, Age, Value, Safety Features)

- Industry Classification

- Vehicle Use Patterns

- Geographic Location

- Driver Qualifications

Liability limits, deductibles, and optional endorsements provide control over costs versus protection levels.

Risk Management

Proactive risk management demonstrates commitment to loss prevention that insurers reward through reduced premiums. This can also produce premium savings exceeding program costs while reducing accident frequency and severity. Some risk management factors for commercial auto insurance include-

- Driver Safety Programs

- Vehicle Maintenance Protocols

- Claims History

Find Commercial Auto Insurance in Georgia with BIS Benefits

Commercial vehicle insurance provides essential protection through liability coverage, physical damage protection, and specialized endorsements addressing unique business exposures. Adequate insurance coverage protects business assets, maintains operational continuity, and provides peace of mind that vehicle-related incidents won't threaten your business's financial stability.

BIS Benefits helps Georgia businesses navigate commercial auto insurance complexity, identifying appropriate coverage levels, comparing carrier options, and structuring policies that provide comprehensive protection at competitive costs. We offer brokerage services for

general liability insurance,

workers' compensation insurance, and more commercial insurance options so you can find coverage options for your specific business needs.

Request a Quote today and one of our brokers will review your commercial auto insurance policy.