What is an Indemnity Plan? A Guide for Employers

What is an Indemnity Plan?

At a Glance: An indemnity plan is a health insurance model that reimburses medical expenses based on services received, allowing employees to see any licensed provider without network restrictions or referrals. These plans come in two forms: traditional indemnity plans that serve as primary health coverage and fixed indemnity plans offered as voluntary benefits.

As healthcare costs continue to rise, employers are under pressure to offer benefits that support employees without driving up premiums or administrative complexity. Many organizations are rethinking how they structure health benefits and looking beyond traditional managed care options. One category gaining renewed attention is the indemnity plan.

Indemnity plans have been used for even longer than

Health Maintenance Organization (HMO) and

Preferred Provider Organization (PPO) plans. What is new is how employers are using them today. Some organizations explore indemnity plans as a primary option for flexibility. Others add hospital indemnity insurance as a supplemental insurance plan or voluntary benefit to help employees manage out-of-pocket costs.

What Is an Indemnity Plan?

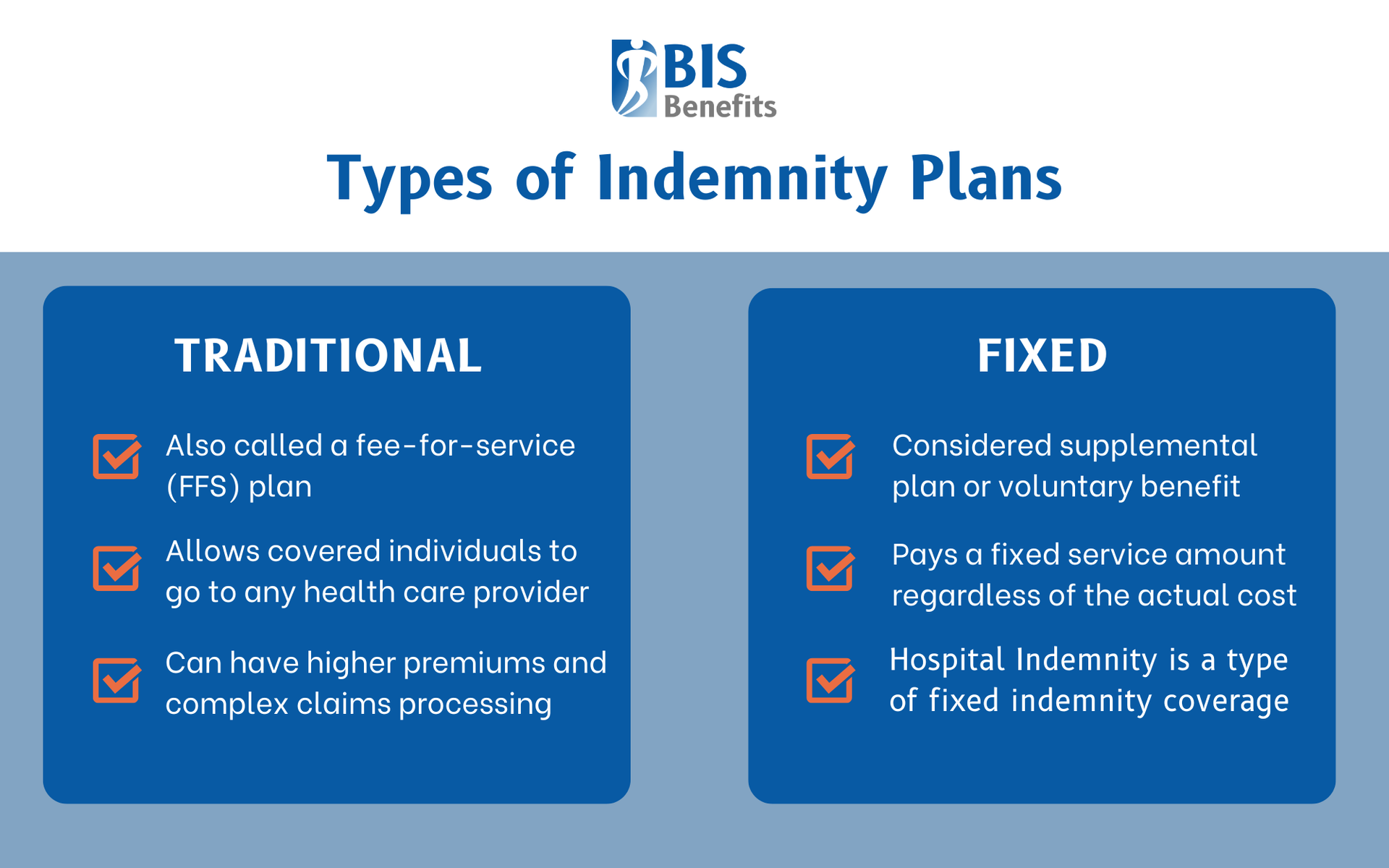

An indemnity plan, also called a fee-for-service plan, is a traditional health insurance model that reimburses medical expenses based on specific services received rather than limiting care to a provider network.

The defining feature of an indemnity insurance policy is provider choice. Each covered person can see any licensed doctor, specialist, or hospital without network restrictions or referrals. This level of flexibility was once one of the standard health coverage options before managed care models became dominant.

Unlike HMOs or PPOs, traditional indemnity plans do not negotiate discounted provider rates. Instead, the plan pays a set amount or a percentage of what it considers reasonable and customary charges. If the provider bills more than the plan pays, the employee is responsible for the remaining balance.

For employers, indemnity plans generally fall into two categories:

- Traditional indemnity plans used as primary health insurance

- Fixed indemnity plans offered as supplemental plan or voluntary benefit

- Hospital Indemnity Insurance Plans:

- Supplemental/voluntary benefits plans may be considered alongside indemnity insurance

- Accident Insurance Plans

- Critical Illness Insurance

Understanding the differences between these two types is critical when evaluating how they fit into your benefits offering.

Traditional Indemnity Plans for Employers

Traditional indemnity plans provide broad health coverage and function as primary insurance. While less common today, they still play a role in certain employer populations.

How Traditional Indemnity Plans Work

A traditional indemnity plan reimburses a percentage of covered medical expenses. For example, the plan may pay 80 percent of reasonable and customary charges, while the employee pays the remaining 20 percent. If a provider charges more than the insurer’s defined limit, the employee may also be responsible for balance billing.

Employees can choose any licensed provider without worrying about in-network or out-of-network distinctions. This flexibility can be valuable for employees who travel frequently or live in areas with limited provider networks.

Employer Considerations

Traditional indemnity plans come with trade-offs. Premiums are often higher than HMO or PPO plans because there is no cost containment through negotiated provider rates. Claims processing can also be more complex, as reimbursement is based on submitted charges rather than preset fee schedules.

From an employee perspective, unpredictable out-of-pocket expenses can be a concern. Even with a high reimbursement percentage, balance billing may create financial uncertainty.

When Traditional Indemnity May Make Sense

Traditional indemnity plans may work well for:

- Employers with a geographically dispersed workforce

- Organizations with employees in rural areas where provider networks are limited

- Companies that prioritize provider choice as a recruitment or retention tool

- Industries where employees value flexibility over lower premiums

While traditional indemnity is no longer the default option, it can still align with specific workforce needs.

Fixed Indemnity Plans as a Voluntary Benefit

Fixed indemnity coverage, including hospital indemnity insurance, is becoming more common as a supplemental health benefit. Unlike traditional indemnity, fixed indemnity plans are not designed to replace primary coverage.

What Is Fixed Indemnity Insurance?

Fixed indemnity insurance covers a set amount for eligible medical events and services. No matter what the final bill ends up being, the covered payment will stay the same under a fixed plan.

How Hospital Indemnity Plans Work

Hospital indemnity plans typically pay a daily or per-event cash benefit, such as a set amount for each day an employee is hospitalized. The payment goes directly to the employee, not the hospital or medical provider. The payout is not tied to the actual medical bill. Instead, the plan pays a predetermined amount based on the benefit schedule.

Employees can use the funds however they choose. Common uses include deductibles, copays, coinsurance, lost wages, travel costs, or childcare expenses during recovery.

This flexibility is a major reason hospital indemnity plans are attractive to employees enrolled in high-deductible health plans.

Common Riders and Add-Ons

Many hospital indemnity plans include optional benefits such as:

- Ambulance transportation

- Emergency room visits

- Intensive care unit stays

- Surgical procedures

- Diagnostic testing and imaging

- Outpatient treatments

Why Employers Are Adding Hospital Indemnity Coverage

Hospital indemnity plans align well with modern benefits strategies, especially when paired with high-deductible health plans.

From an employer perspective, these plans are typically offered as voluntary benefits. Employees pay the premiums through payroll deduction, keeping employer costs low.

Other reasons employers add hospital indemnity coverage include:

- Helping employees manage out-of-pocket costs

- Providing financial support during medical events

- Improving benefits satisfaction without increasing employer spend

- Offering a simple benefit that is easy to understand

- Enhancing the perceived value of the overall benefits package

For employees, the predictability of a fixed cash benefit provides peace of mind when unexpected hospital stays occur.

Key Differences Between Traditional and Hospital Indemnity Plans

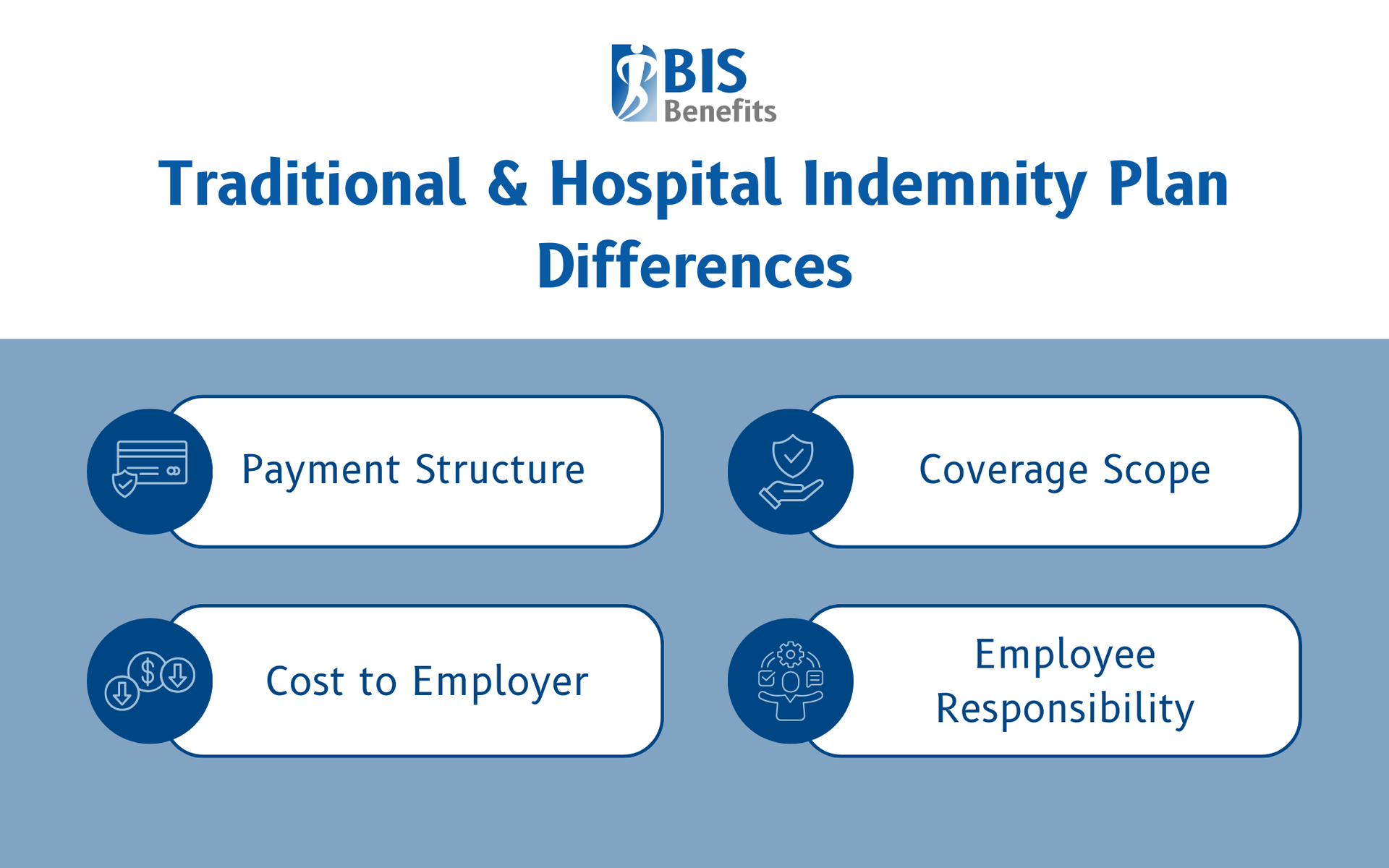

Coverage Scope

Indemnity plans serve as primary coverage for a wide range of medical services. Hospital indemnity plans focus specifically on hospital-related events and are supplemental.

Payment Structure

Traditional indemnity reimburses a percentage of medical bills. Hospital indemnity pays a fixed cash amount per day or per event, regardless of how much the actual hospital bills are.

Role in the Benefits Package

Indemnity can serve as primary health insurance. Hospital indemnity complements existing coverage.

Cost to Employer

Indemnity plans usually require employer premium contributions. Hospital indemnity plans are often employee-paid voluntary benefits.

Employee Financial Responsibility

Indemnity may leave employees exposed to balance billing. Hospital indemnity helps offset a variety of expenses without replacing primary insurance.

Benefits of Offering Indemnity Plans

For Employers

Indemnity health plans can enhance benefits offerings without creating unexpected costs. Hospital indemnity coverage, in particular, allows employers to add value with minimal financial impact.

Other benefits include improved recruitment and retention, increased employee satisfaction, and support for employees during costly medical events.

For Employees

Employees benefit from additional financial protection, flexible use of funds, and affordable premiums. Indemnity plans, where offered, provide unrestricted provider choice.

Considerations for Adding Indemnity Plans

Evaluating Hospital Indemnity as a Voluntary Benefit

Employers should assess whether employees struggle with deductibles, express concerns about healthcare affordability, or value financial protection alongside their primary plan.

Implementation Considerations

Key steps include selecting a carrier, determining benefit amounts, setting up payroll deductions, and coordinating enrollment with existing benefits.

Employee Education and Communication

Clear communication is critical. Employees need to understand that hospital indemnity insurance supplements primary coverage and does not replace comprehensive medical insurance.

Compliance Considerations

Hospital indemnity plans are generally classified as excepted benefits under the ACA, but they must meet specific requirements. Employers should work with a benefits advisor to ensure compliance with federal and state regulations.

Is an Indemnity Plan Right for Your Organization?

Indemnity plans may make sense if your workforce prioritizes provider choice and you are willing to invest in higher premiums. Hospital indemnity coverage may be a good fit if you offer a high-deductible health plan, want to enhance voluntary benefits, and seek to support employee financial wellness.

Questions to discuss with your benefits advisor include:

- Plan design options

- Coordination with existing coverage

- Compliance requirements

- Employee communication strategies

Trust an Experienced Insurance Broker to Find the Perfect Plan

Indemnity plans provide flexibility and financial protection in an evolving healthcare landscape. Hospital indemnity insurance has emerged as a popular voluntary benefit that helps employees manage out-of-pocket costs with minimal employer expense. Traditional indemnity remains an option for organizations that value unrestricted provider choice.

By evaluating workforce needs and benefits gaps, employers can determine whether indemnity options strengthen their overall benefits strategy. Working with experienced benefits brokers can help ensure the right solution for both your organization and your employees.

At BIS Benefits, our brokers can walk you through the different insurance coverage options available for your business. We offer several

Group Benefits and

Business Insurance products to accommodate many different commercial insurance needs. If your business is located in Georgia and has at least 15 employees,

Request a Quote to find out how BIS can help you find the right insurance plan.