What Is Business Owner's Policy Insurance?

What is Business Owner's Policy Insurance?

At a Glance: A business owner's policy (BOP) bundles property insurance, general liability coverage, and business interruption insurance into a single package designed for small to mid-sized businesses. While a BOP covers the most common business risks, certain exposures like workers' compensation, commercial auto, and cyber liability still require separate policies.

Small business owners often need multiple types of insurance coverage, but purchasing separate policies for each risk can be complicated and expensive. A business owner's policy, commonly known as a BOP, bundles essential coverages into a single, convenient package designed specifically for small to mid-sized businesses.

BOPs typically combine property insurance, general liability insurance, and business interruption coverage at a lower cost than purchasing each separately. Understanding what a BOP covers and whether it meets your business needs helps you make informed decisions about protecting your company.

What Is a Business Owner's Policy?

A BOP is a packaged insurance policy that bundles multiple coverages into one policy designed specifically for small to medium-sized businesses. It combines property insurance, general liability insurance, and business interruption coverage, providing streamlined protection with one policy, one premium, and one renewal date. This single policy document covers multiple risk categories, simplifies administration with unified policy terms and conditions, and allows claims to be handled under one policy regardless of which coverage type is involved.

Insurers offer BOPs because they provide an efficient way to deliver essential coverages to small businesses. For businesses new to commercial insurance, a BOP serves as an attractive entry point that covers the most common risks without requiring complex policy structures.

What Does a Business Owner's Policy Cover?

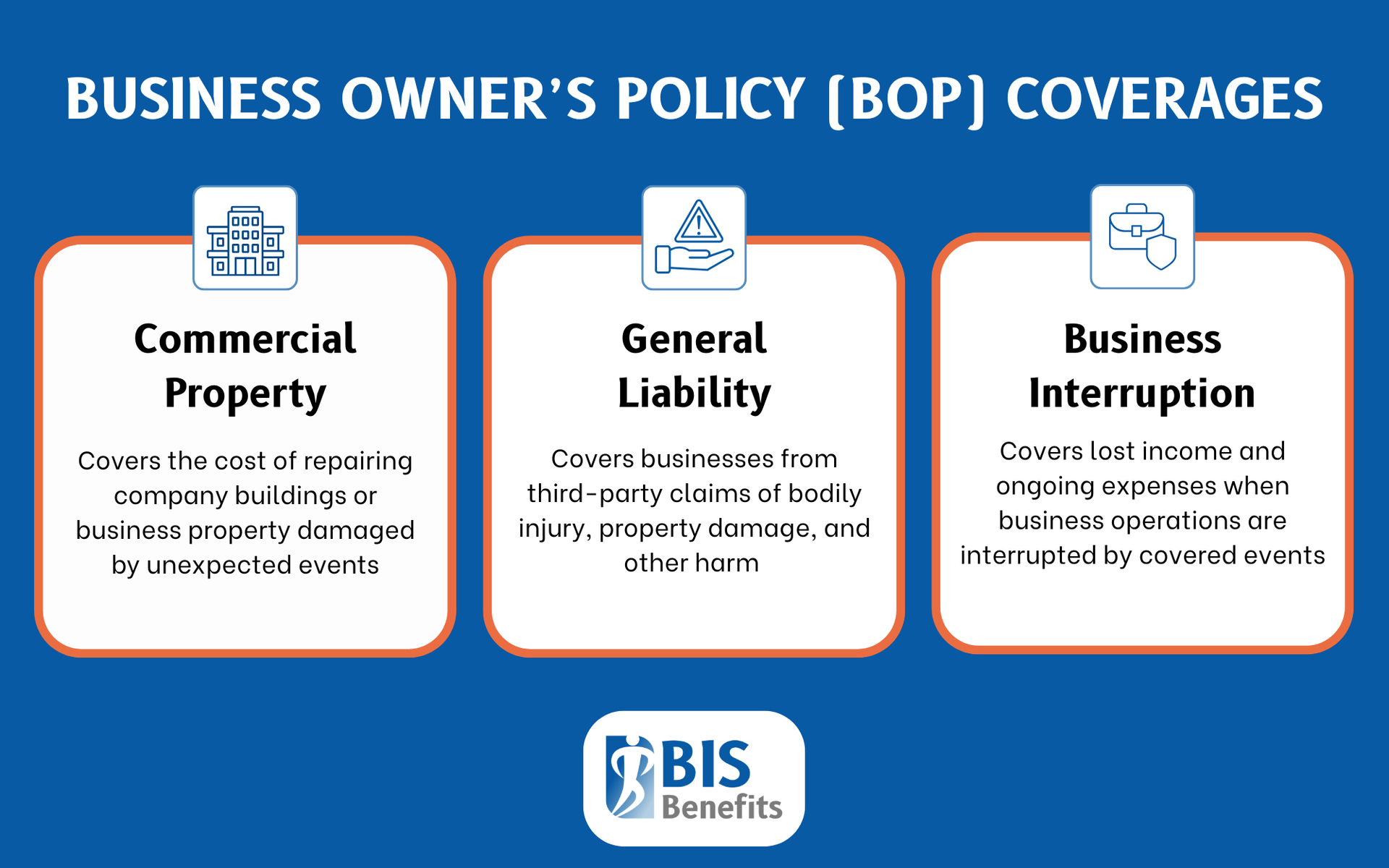

Commercial Property Insurance

A BOP provides coverage for buildings owned or occupied by the business and protection for business property, including equipment, inventory, furniture, and fixtures. Coverage extends to property of others in your care, custody, or control, and protects against fire, theft, vandalism, and other covered events. Many policies also include coverage for outdoor signs, fencing, and other structures on the property.

General Liability Insurance

General liability coverage includes bodily injury claims from customers, visitors, or third parties, as well as third-party property damage caused by business operations. It also covers personal and advertising injury, which includes claims of libel, slander, and copyright infringement. The policy pays for legal defense costs for covered claims and includes products and completed operations liability.

Business Interruption Insurance

Also called business income insurance, this coverage helps your company survive financially when operations are disrupted by a covered event. It covers lost income during the closure period and pays for ongoing expenses like rent, utilities, and payroll. The extra expense coverage it provides helps minimize downtime by paying for costs to get the business running again quickly. This coverage is typically tied to property damage from a covered peril and provides critical support during the recovery period.

Additional Coverages

To provide added protection and address potential risks that many small businesses face, some BOPs include more coverages, such as:

- Equipment breakdown coverage

- Electronic data loss protection

- Coverage for valuable papers and records

- Accounts receivable coverage

What a BOP Does Not Cover

Several important coverages require separate policies:

- Workers' compensation insurance (which is required in most states)

- Commercial auto insurance for business vehicles

- Professional liability insurance, also known as Errors and Omissions (E&O) coverage

- Employment practices liability insurance

- Directors and Officers (D&O) insurance

- Cyber liability insurance

- Health insurance and employee benefits

Common exclusions that typically require separate coverage include:

- Damage from weather or natural disasters (floods, earthquakes, etc.)

- Intentional acts or criminal conduct

- Professional services errors

- War and terrorism

- Employee injuries (covered by workers' compensation)

- Auto accidents (covered by commercial auto)

BOPs have coverage limitations that businesses should understand. Policy limits may be insufficient for larger businesses. Certain high-risk industries may not qualify for standard BOPs, and home-based businesses may face restrictions. Some specialized equipment or inventory may need additional coverage beyond what a standard BOP provides.

Benefits of a Business Owner's Policy

Cost Savings

Bundled coverage typically costs less than purchasing policies separately because insurers pass administrative efficiencies on to policyholders. Discounts for combining coverages in a single package make BOPs attractive, and competitive pricing is designed with small business budgets in mind.

Convenience & Simplicity

BOPS have one policy to track instead of several, with a single renewal date and premium payment, making them easier to manage for some businesses. Unified policy terms and conditions simplify understanding your coverage, and the claims process is more straightforward. The overall coverage structure is easier to understand and explain to stakeholders.

Comprehensive Protection

BOPs address multiple common business risks in one package. They are designed to cover the most frequent small business exposures and provide baseline protection that can be customized with endorsements. This approach reduces gaps in coverage that can occur when managing separate policies with different terms and conditions.

Flexibility & Customization

With a BOP, endorsements are available to add optional coverages to address industry-specific exposures, and coverage limits can be adjusted to match business requirements. This allows businesses to tailor their policy to fit their specific needs.

BOP Coverage Limits and Deductibles

The coverage limits for BOPs are typically lower compared to other plans. However, the exact amounts can vary depending on the business’s income, property value, and risk profile.

Limits

Choosing appropriate limits requires careful consideration. Higher limits provide greater protection but increase premiums.

Property limits should reflect the replacement cost of buildings and contents. Liability limits should consider your exposure level and any contractual requirements from landlords, clients, or partners. Higher limits provide greater protection but increase premiums.

Consider an

umbrella policy for additional protection above BOP limits if your exposure warrants it.

Deductibles

Deductibles represent the amount your business pays out of pocket before coverage applies. Higher deductibles lower premium costs but increase your financial responsibility when claims occur. Choose a deductible level your business can afford to pay in the event of a claim. Deductibles may vary by coverage type within the policy.

BOP vs. Separate Policies

A BOP makes sense for small businesses with straightforward coverage needs and budget-conscious businesses seeking cost-effective protection or simplified policy management.

Separate policies may be better for larger businesses exceeding BOP eligibility thresholds or companies needing higher coverage limits than BOPs provide. Businesses with specialized or complex risk profiles may need tailored coverage that a standard BOP cannot offer.

Comparing Policy Options

Before making a decision, businesses should:

- Obtain quotes for both a BOP and separate policies

- Compare total premiums, coverage limits, and deductibles

- Consider the administrative costs of managing multiple policies

- Factor in potential coverage gaps that can occur with separate policies

Managing Your BOP Coverage

Annual policy review helps ensure your coverage keeps pace with your business. Review coverage limits annually to reflect growth, update property values to account for new equipment, inventory, or improvements, and reassess liability limits based on current operations and contracts. Add endorsements as business needs change over time.

Businesses should update coverage when significant changes occur, such as:

- Moving to a new location

- Making significant equipment purchases or property improvements

- Experiencing revenue growth or expansion of operations

- Adding new products or services

- Changes in contractual insurance requirements

Working with a qualified insurance broker helps ensure you have the right coverage. Brokers experienced with small business insurance can provide guidance on your specific situation. These professionals can discuss specific risks and coverage needs for your industry and help you learn more about available endorsements and customization options.

Discover Coverage Solutions with a Business Insurance Broker

A business owner's policy bundles property insurance, general liability, and business interruption coverage into a convenient, cost-effective package for small to mid-sized businesses. BOP insurance provides comprehensive baseline protection that can be customized with endorsements to address specific business requirements. However, many businesses require additional types of coverage to fully meet their needs.

Working with an experienced insurance professional can help you determine what insurance plan is right for your business. At BIS Benefits, our

insurance brokers work closely with you to explore your coverage options and find the best plan for your specific risks and operations. If your business is located in Georgia and has at least 15 employees,

Request a Quote today.