How Do Construction Bonds Work for Small Businesses?

How Do Construction Bonds Work?

At a Glance: Construction bonds are specialized surety bonds that guarantee contractors will fulfill their contractual obligations, protecting project owners from financial losses if contractors fail to complete work or deliver substandard results. Small construction contractors need construction bonds to bid on public projects, demonstrate credibility to clients, and access larger commercial opportunities that require bonding as standard practice.

What Is a Construction Bond?

A construction bond is a specialized type of surety bond designed specifically for the construction industry, serving as a financial guarantee that protects project owners when contractors fail to meet their contractual obligations. Unlike insurance that protects the policyholder, construction bonds protect the project owner or client from financial losses caused by contractor default, poor workmanship, or failure to complete projects as agreed.

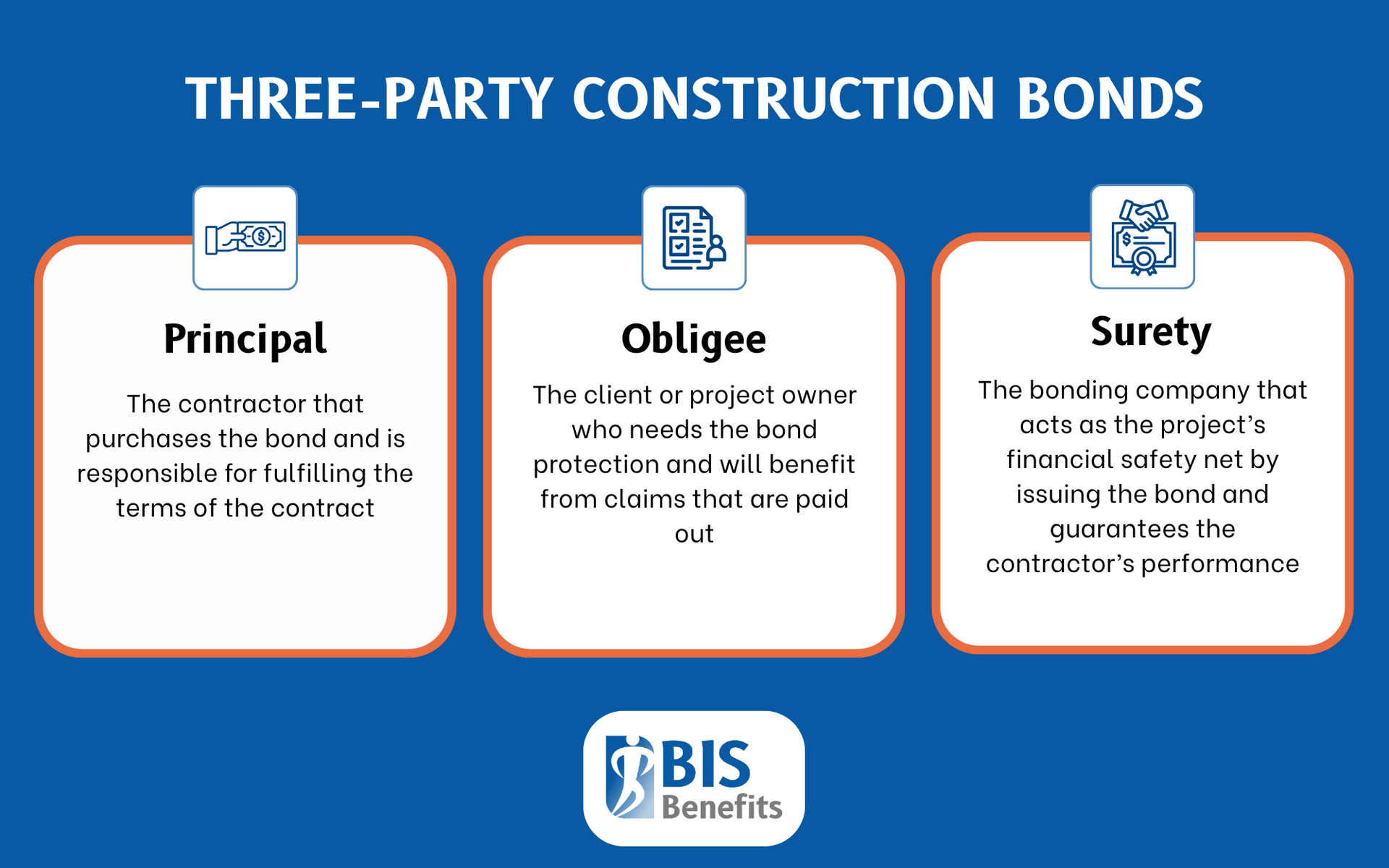

Construction bonds operate through a unique three-party relationship that distinguishes them from traditional insurance policies. The principal is the contractor who purchases the bond and is responsible for fulfilling the contract terms. The obligee represents the project owner or client who requires the bond protection and will benefit from any claims paid. The surety is the bonding company that issues the bond and guarantees the contractor's performance, essentially acting as a financial safety net project.

Through this structure, the surety company assumes responsibility for ensuring project completion or compensating the project owner for losses, but ultimately holds the contractor liable for any payments made on their behalf. This arrangement provides project owners with confidence that their investments are protected while creating accountability for contractors to maintain high-performance standards.

Why Small Business Contractors Need Construction Bonds

Construction bonds have become increasingly essential for small business contractors seeking to compete in today's construction marketplace.

Legal Requirements

Many public sector projects, including federal, state, and local government contracts, legally require contractors to provide construction bonds before bidding. The Miller Act mandates bonding for federal construction projects exceeding $100,000, while individual states have enacted "Little Miller Acts" with similar requirements for state and local projects.

Business Development

Construction bonds serve as tools that demonstrate financial reliability and professional credibility. When small contractors can provide bonding, they signal to potential clients that they possess the financial stability, technical expertise, and track record necessary to complete complex projects. This credibility becomes particularly valuable when competing against larger, more established firms with extensive bonding capacity.

Small Business Benefits

Construction bonds also provide small businesses with access to larger projects that would otherwise be unavailable. Many private owners, particularly those undertaking significant commercial or industrial projects, require bonding as a standard practice to protect their investments. By obtaining bonding capacity, small contractors can pursue projects that offer better profit margins and growth opportunities than smaller, unbonded work.

Through a surety bond company's underwriting evaluation, thorough financial and operational assessments are conducted that often reveal areas for business improvement. This analysis can help small contractors identify weaknesses in their financial management, project management systems, or operational procedures.

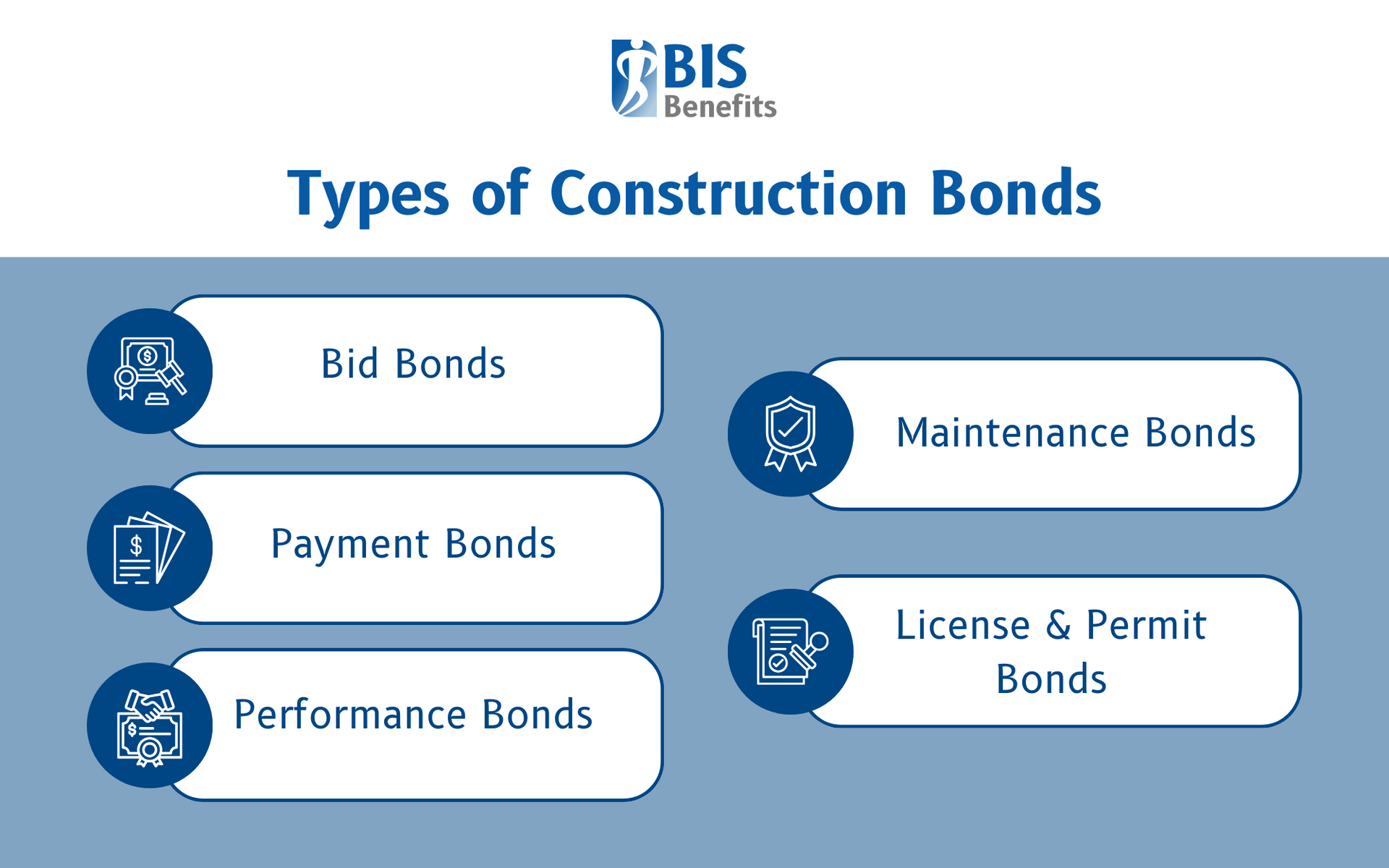

Types of Construction Bonds

The construction industry utilizes several distinct types of bonds, each designed to address specific risks and project phases. Understanding these different bond types helps small contractors determine which bonds they need for particular projects and clients.

Bid Bonds

Bid bonds protect project owners during the competitive bidding process by guaranteeing that winning contractors will accept the contract and provide required performance and payment bonds. Typically ranging from 5-10% of the bid amount, bid bonds prevent contractors from submitting unrealistic bids or withdrawing after winning contracts. If a contractor fails to honor their bid, the surety compensates the project owner for the difference between the winning bid and the next lowest acceptable bid.

Performance Bonds

Performance bonds, the most comprehensive construction bond type, guarantee that contractors will complete projects according to contract specifications, schedules, and quality standards. These bonds typically equal 100% of the contract value and remain in effect throughout the construction period. If contractors default, the surety can hire replacement contractors to complete the work or compensate project owners for additional costs incurred.

Payment Bonds

Payment bonds ensure that contractors pay subcontractors, suppliers, and laborers involved in bonded projects. These are equal in bond amount to performance bonds and protect project owners from mechanics liens and legal disputes from unpaid project participants. These bonds are particularly important for public projects where property liens may not be available to unpaid parties.

Maintenance Bonds

Also known as warranty bonds, these bonds extend protection beyond project completion by covering defects in materials or workmanship that appear during specified warranty periods, typically one to two years. These bonds provide project owners with recourse if contractors fail to remedy legitimate defects discovered after project acceptance.

License & Permit Bonds

License and permit bonds represent regulatory requirements that enable contractors to operate legally in specific jurisdictions. These bonds guarantee compliance with local regulations, proper completion of permitted work, and payment of applicable fees or fines. Requirements vary significantly by location and trade specialty.

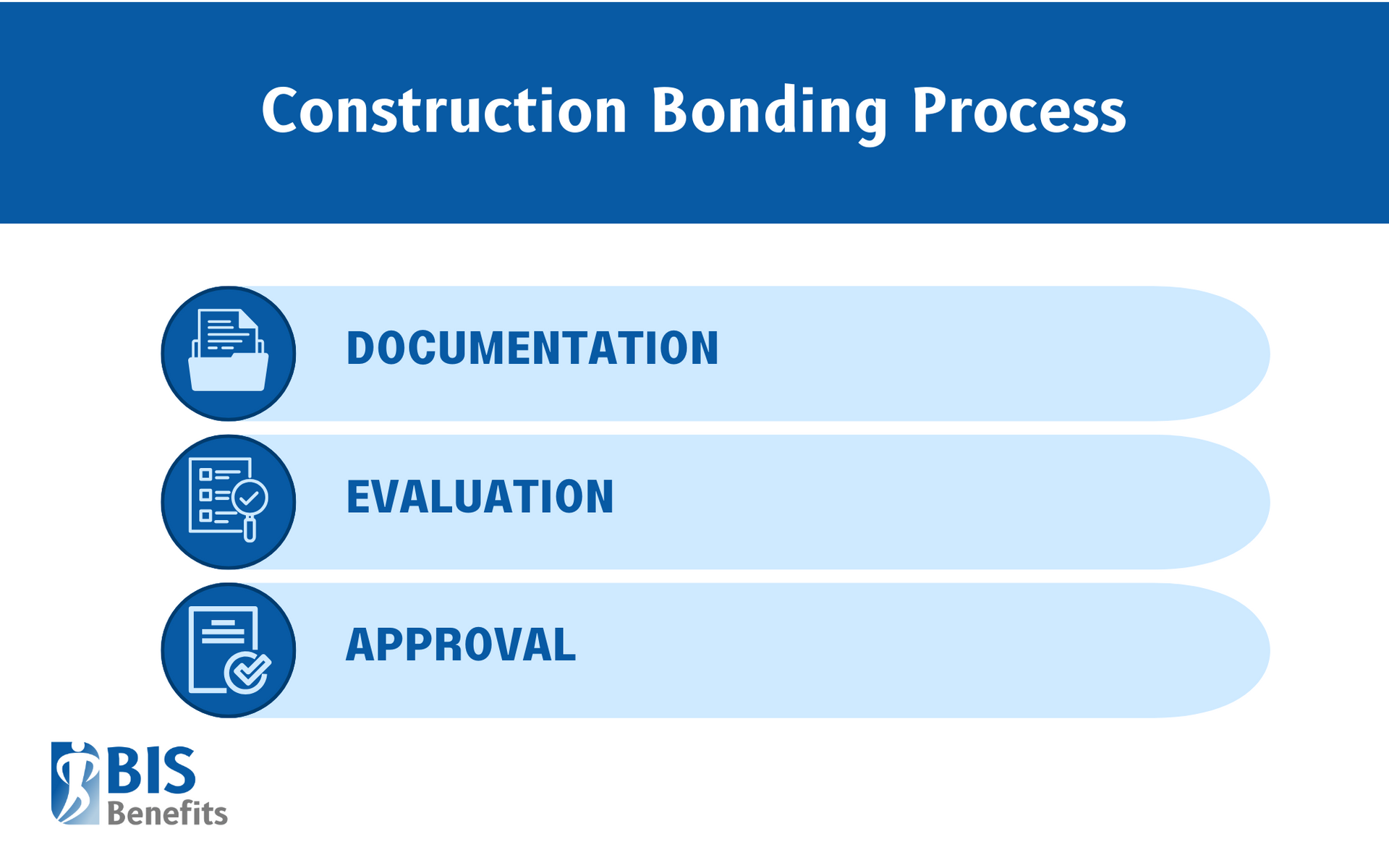

How Construction Bonds Work Step-by-Step

The construction bonding process begins when contractors identify projects requiring bonds and contact licensed surety companies or experienced bonding agents.

1. Documentation

Contractors must submit comprehensive applications including detailed financial statements, business history, project experience, and personal credit information. This enables surety companies to evaluate the contractor's ability to complete bonded projects successfully.

2. Evaluation

Surety underwriters analyze submitted information to assess risk factors including financial stability, management experience, project complexity, and market conditions. This process, known as prequalification, determines whether the surety will provide bonding and establishes the contractor's bonding capacity - the maximum amount of work they can have bonded simultaneously.

3. Approval

Once approved, contractors receive bond quotes specifying premium costs and terms. After accepting terms and paying premiums, the surety issues bonds that contractors submit with their project bids or contract documents. Bonds typically include specific project details, contract references, and effective dates that align with project schedules.

Throughout bonded projects, contractors must maintain performance standards and

fulfill all contractual obligations. Project owners may file claims against bonds, triggering surety investigations to determine claim validity. Valid claims result in surety payments to project owners, but contractors ultimately remain liable to reimburse sureties for all payments made in addition to associated costs and legal fees.

How to Get Bonded as a Small Business

Small contractors seeking bonding should begin by selecting surety companies that specialize in small business accounts and understand the unique challenges facing emerging contractors. Regional or specialty sureties often provide more personalized service and flexible underwriting approaches compared to large national companies focused on major contractors.

Successful bond applications require comprehensive documentation demonstrating business stability and competence. This documentation can include:

- Audited or reviewed financial statements

- Business tax returns

- Personal financial statements

- Project references

- Banking relationships

- Resumes highlighting management experience.

Contractors should prepare this documentation carefully and accurately to avoid delays or denials.

Long-Term Strategy for Bonding Success

Small contractors can improve their bonding prospects through several strategic actions, including:

- Maintaining Strong Personal & Business Credit Scores: This demonstrates financial responsibility and reduces perceived risk.

- Establishing Consistent Profitability & Positive Cash Flow Trends: This shows business viability and growth potential.

- Building a Project Portfolio: Even if small, this provides evidence of technical competence and reliability.

- Developing Relationships with Experienced Bonding Agents: Insurance agents who understand surety requirements can provide valuable guidance throughout the bonding process.

How Much Do Construction Bonds Cost?

Construction bond premiums vary significantly based on multiple risk factors that surety companies evaluate during underwriting, including:

Project Size and Complexity: Larger, more complex projects typically requiring higher premiums due to increased risk exposure.- Bond Type: Bid bonds generally cost less than performance and payment bonds due to shorter exposure periods and lower risk levels.

- Contractor Qualifications: Credit scores, both personal and business, are one of the most significant cost factors.

- Financial Indicators: These can include working capital, net worth, and debt-to-equity ratios.

- Business Track Record: Contractors with extensive successful project histories typically qualify for lower rates than those with limited experience or past performance issues.

- Industry Specialization: Technical expertise in specific construction types can influence pricing favorably.

- Market Conditions: Premium rates may decrease during competitive market periods as sureties compete for quality accounts or increase during difficult market conditions following major losses.

What Happens if There's a Bond Claim?

Bond claims typically happen when contractors fail to complete projects according to contract terms, deliver substandard work, or default on their obligations entirely. Common claim triggers include missed completion deadlines, failure to correct defective work, abandonment of projects, or bankruptcy.

Upon receiving claims, surety companies conduct thorough investigations to determine the claim’s validity and the extent of damages. This process involves:

- Reviewing Construction Contract Documents

- Inspecting the Work Performed

- Interviewing Involved Parties

- Assessing the Costs Required to Fix Damages & Defaults

Sureties may attempt to work with contractors to cure defaults before paying claims, particularly when defaults appear correctable.

When claims prove valid, sureties must decide whether to complete projects using replacement contractors or compensate project owners for damages incurred. Completion options often prove more cost-effective for sureties and beneficial for project owners seeking finished projects rather than monetary compensation.

Regardless of how claims are resolved,

contractors remain liable to reimburse sureties for all amounts paid plus associated investigation, legal, and administrative costs. This obligation can create significant financial hardship for contractors and often includes personal guarantees from business owners. Claims also damage contractors' bonding capacity and may result in surety companies declining future bonding requests.

How BIS Benefits Can Help Businesses with Construction Bonds

Navigating construction surety bonds requires specialized expertise that many small contractors lack. BIS Benefits provides comprehensive brokerage services designed specifically for growing businesses seeking to establish or expand their bonding capacity. Our experienced team understands the unique challenges facing small contractors and works closely with surety companies that specialize in small business accounts.

Learn more about how our

Surety Bond and

Construction Business Insurance brokers can help your small business access the bonding capacity necessary for growth and success in today's competitive construction marketplace. If your business is based in Georgia,

request a quote from BIS Benefits today to discuss your construction bonding needs.