How to Get Bonded and Insured for a Small Business

How to Get Bonded and Insured for a Small Business

At a Glance: Getting bonded and insured for a small business involves two distinct protections: bonds serve as financial guarantees that you'll fulfill contractual obligations (protecting your clients), while insurance provides coverage when accidents or unforeseen events occur (protecting your business). Small businesses typically need various combinations of bonds and insurance coverage depending on their industry, legal requirements, and client demands.

Bonds and insurance are fundamental risk management tools that every small business owner should understand. While these terms are often mentioned together, they serve distinctly different purposes in protecting your business.

Insurance provides financial protection when accidents, damages, or unforeseen events occur, covering losses and liabilities that could otherwise devastate a small business.

Bonding, on the other hand, serves as a financial guarantee that you'll fulfill your contractual obligations, protecting clients and project owners if you fail to deliver on your promises. Together, these protections create a safety net that enables small businesses to operate confidently while meeting client expectations and regulatory requirements.

Why Bonding & Insurance Matter for Small Businesses

Operating a small business without proper bonding and insurance exposes you to potentially catastrophic financial risks that could destroy years of hard work in a single incident. A customer slip-and-fall accident could result in medical bills and legal fees totaling hundreds of thousands of dollars. A data breach affecting client information might trigger regulatory fines, notification costs, and lawsuits that exceed your business's entire annual revenue. Product defects, employee injuries, or professional errors can generate claims that quickly overwhelm a small business's financial resources.

Beyond protecting against financial ruin, bonding and insurance requirements often determine which opportunities your business can pursue.

- Commercial Clients: Many clients view adequate coverage as a basic professional requirement and will refuse to work with unbonded or uninsured contractors.

- Government Contracts: These typically mandate specific bonding and insurance minimums before allowing companies to bid on projects.

- Industry-Specific Licenses: Many industries require proof of bonding or insurance coverage to maintain legal operating status.

State and local regulations frequently mandate specific coverage types for particular business activities:

- Workers' Compensation: This type of insurance is legally required in most states for businesses with employees.

- Errors & Omissions (E&O): Professional service providers may need this insurance coverage to comply with licensing board requirements.

- License & Permit Bonds: Contractors often must obtain these bonds before receiving authorization to perform certain types of work.

Failing to maintain required coverages can result in license suspension, contract termination, or legal penalties that effectively shut down business operations.

Bonded vs. Insured — What's the Difference?

Understanding the fundamental distinction between bonds and insurance is crucial for making informed coverage decisions.

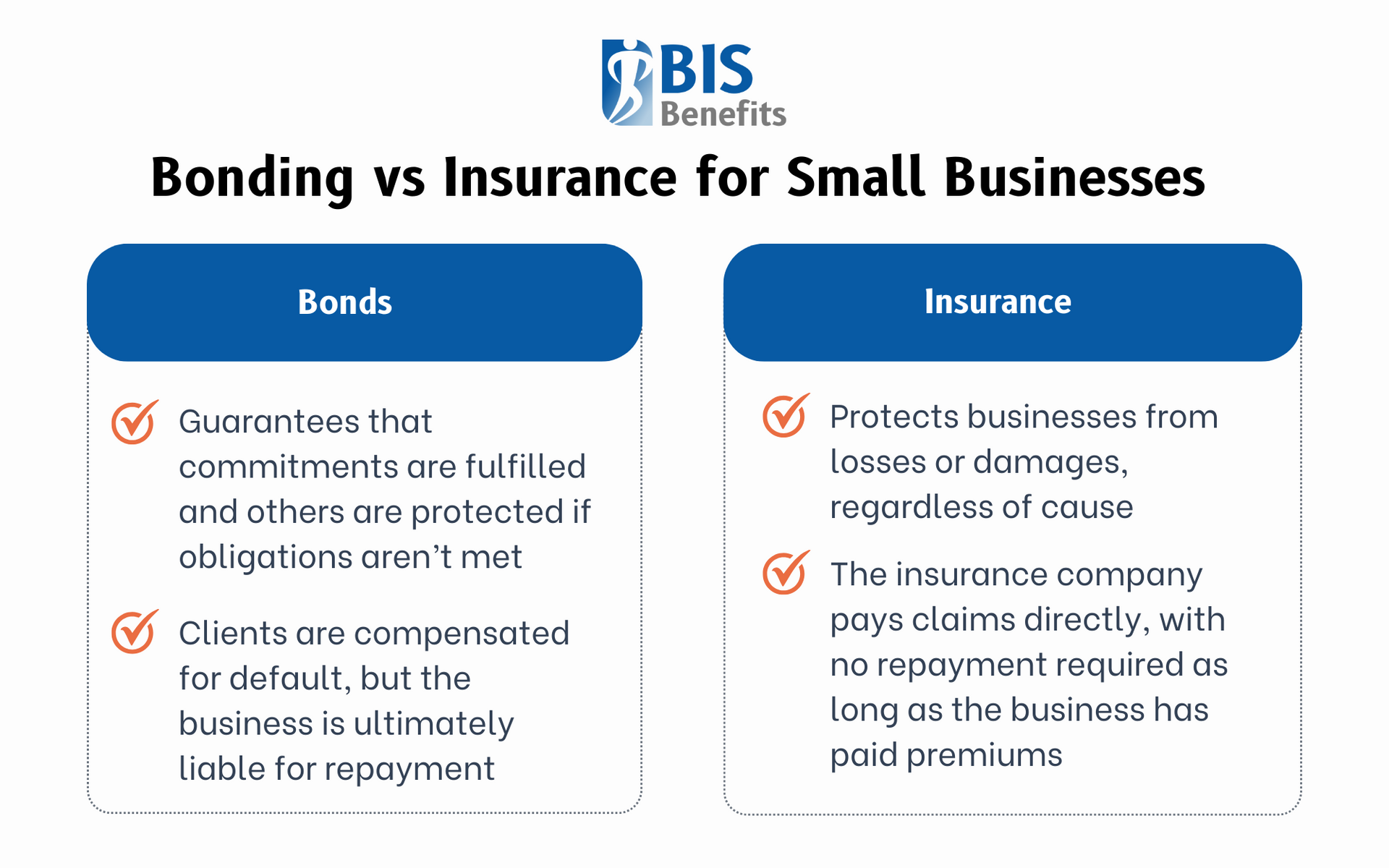

Bonds

A surety bond functions as a guarantee that you'll follow through on your commitments, protecting others from your potential failure to perform. When you're bonded, a surety company promises to compensate your clients if you fail to complete contracted work, violate regulations, or otherwise breach your obligations. However, you remain ultimately liable to reimburse the surety for any payments made on your behalf. These are often used for construction and other long-term service industries.

Insurance

Insurance operates as protection when something goes wrong, covering losses you suffer or damages you cause to others. Unlike bonds, insurance genuinely transfers risk from your business to the insurance company. When covered losses occur, the insurer pays claims without requiring reimbursement from you, assuming you've maintained coverage and paid premiums.

Types of Bonds for Small Businesses

Small businesses might need various bond requirements depending on their industry, location, and client base.

Surety Bonds

The most common type for contractors and construction companies, these guarantee project completion and payment to subcontractors and suppliers. These bonds enable small contractors to bid on larger projects and demonstrate financial reliability to potential clients. Performance bonds guarantee work completion to specifications, while payment bonds ensure subcontractors and suppliers receive compensation for their contributions.

Fidelity Bonds

These protect employers from employee dishonesty, theft, or fraudulent activities. Businesses whose employees handle cash, inventory, or sensitive information often purchase fidelity coverage to protect against internal theft. These bonds are particularly important for retail operations, financial services companies, and businesses that handle client funds or valuable property.

License and Permit Bonds

Satisfying regulatory requirements enables businesses to operate legally in specific jurisdictions or industries. Many trades require these bonds as conditions for obtaining or maintaining professional licenses. Auto dealers, mortgage brokers, collection agencies, and numerous other business types must post license bonds to comply with state regulations.

Contract Bonds

These guarantee performance on specific projects or agreements, providing clients with recourse if contractors fail to deliver promised results. These bonds are common in government contracting, where agencies require assurance that vendors will fulfill their obligations. Private sector clients increasingly require contract bonds for significant projects as standard risk management practice.

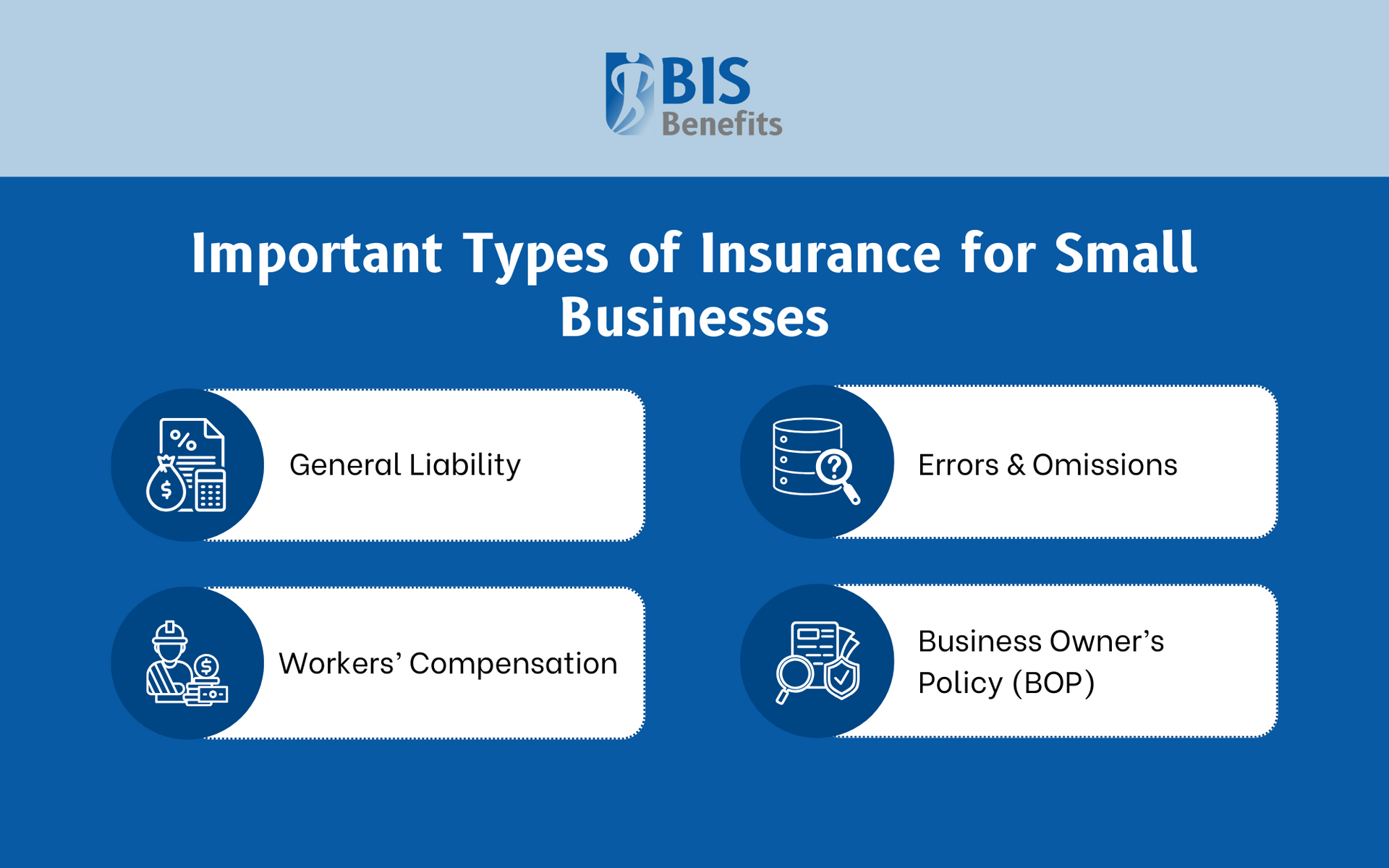

Key Small Business Insurance Policies to Consider

General Liability insurance

This coverage, which is often required by clients and landlords, provides essential protection for most small businesses, covering third-party claims for bodily injury, property damage, and advertising injury. Incidents that this coverage protects against include:

- Customer slip-and-fall accidents

- Product defects that cause injuries

- Allegations of false advertising

Workers' Compensation

This insurance covers medical expenses and lost wages for employees injured during work activities. Most states legally require this coverage for businesses with employees, and penalties for non-compliance can be severe. Workers' compensation also protects employers from lawsuits related to workplace injuries, providing legal defense and settlement coverage.

Errors and Omissions Insurance

Also called professional liability coverage, this insurance protects service-based businesses from claims alleging inadequate work, missed deadlines, or professional mistakes. This coverage is often used by licensing boards and professionals whose advice or services could cause financial losses for clients.

Business Owner's Policy (BOP)

This bundled policy combines general liability and commercial property insurance into a single package. BOPs often provide broader protection at lower costs than purchasing separate policies, making them a cost-effective option for small businesses. Additionally, they typically include business interruption coverage, which pays for lost income when covered events prevent normal operations.

How to Get Bonded

The bonding process begins with determining which bonds your business needs based on legal requirements, industry standards, and client demands.

1. Research & Review

Research federal, state, and local regulations that apply to your business activities, as many bonding requirements are legally mandated. Review typical client contracts and industry practices to identify commonly required bond types. Professional associations and trade organizations often provide guidance on standard bonding practices for specific industries.

2. Strengthen Financials and Credit

Strong financials, including positive cash flow, adequate working capital,reasonable debt levels, and personal and business credit scores improve your bonding prospects and reduce premium costs.

- Personal Credit Score: Maintain strong credit by paying bills promptly, managing debt responsibly, and correcting any credit report errors.

- Business Credit Score: Build business credit by establishing trade relationships, maintaining business bank accounts, and ensuring your business is properly registered with credit reporting agencies.

3. Prepare Documentation

Surety companies evaluate your creditworthiness, financial stability, and track record before approving bonds and setting premium rates. Prepare comprehensive documentation, including:

- Financial Statements

- Business Tax Returns

- Personal Credit Reports

- Project References

4. Contact Small Business Insurance Bonding Experts

Once you've identified necessary bonds, contact licensed surety companies or experienced insurance bonding agents who can guide you through the application process.

How to Get Insured

1. Assess Business Risks

Begin the insurance process with a comprehensive risk assessment that identifies potential threats to your business, such as:

- Property Risks: Fire, theft, and natural disasters could damage your premises, equipment, or inventory.

- Liability Exposures: Incidents like customer injuries, product defects, and professional errors could result in lawsuits.

- Business Interruption Risks: Data breaches and other interruptions could halt operations and eliminate income streams.

2. Gather Information

Put together all the information you will need for insurance quotes, including:

- Accurate Descriptions of Business Operations

- Detailed Inventories of Business Property

- Revenue Figures

- Employee Counts

- Property Values

- Prior Loss History

- Safety Programs

- Security Measures

- Risk Management Practices

3. Find the Right Insurance Professional

Qualified insurance brokers help identify appropriate coverage types, compare quotes from different insurers, and negotiate favorable terms. They also provide ongoing support for claims, policy changes, and coverage reviews as your business evolves. Experienced business insurance brokers who understand small business needs can access multiple insurance companies and provide ongoing support for claims, policy changes, and coverage reviews as your business evolves.

Keeping Your Coverage Active

Maintaining active bonding and insurance coverage requires ongoing attention and proactive management.

Proactive Renewal

Late renewals may result in coverage lapses, increased premiums, or policy cancellations that damage your business relationships and bonding capacity. Mark renewal dates on your calendar and begin the renewal process well in advance to avoid coverage gaps that could expose your business to risk or violate contractual requirements.

Maintain Up-to-Date Records

Proper documentation proves coverage existence, supports claim submissions, and helps resolve disputes.

- Keep detailed records of all policies, premium payments, claims, and correspondence with carriers.

- Store copies of current policies in secure, accessible locations. Ensure key personnel know how to access coverage information during emergencies or claim situations.

- Keep your coverage information current by promptly notifying carriers about changes in business operations, revenue, employee counts, or locations.

Plan for Business Growth & Development

Significant business changes can affect coverage needs and premium calculations, including:

- Business Expansion: Growing into new markets, service offerings, or geographic areas may require additional coverage types or higher limits.

- Increased Revenue & Asset Values: These necessitate corresponding increases in coverage limits to maintain adequate protection.

Failing to report material changes might void coverage or result in claim denials when you need protection most. As your business grows and evolves, regularly review your bonding and insurance needs with qualified professionals. Schedule annual reviews with your broker to ensure your coverage keeps pace with your business growth and changing risk exposures.

Finding the Right Bonding & Business Insurance Plans with BIS Benefits

From workers' compensation insurance to commercial auto insurance, our business insurance agents work with many different types of companies and insurance providers.

If your business is located in the Metro Atlanta area, give us a call to find out what our

Surety Bond or

Business Insurance brokerage services can do for you!