What Georgia Businesses Need to Know About Errors & Omissions Insurance

What Georgia Businesses Need to Know About Errors & Omissions Insurance

At a Glance: Errors & Omissions (E&O) insurance protects businesses from claims that their services caused financial harm due to mistakes, missed deadlines, or inadequate advice. Understanding how E&O works and how state regulations affect coverage helps Georgia professionals manage risk and protect their livelihoods.

Errors & Omissions (E&O) insurance, also known as professional liability insurance, protects businesses and professionals against claims of inadequate work, negligent actions, or mistakes in the professional services they provide. For Georgia businesses offering professional advice, consulting, or specialized services, E&O coverage has become increasingly important as litigation risks continue to grow.

The modern business environment exposes professionals to numerous liability risks. Even when professionals successfully complete their work, dissatisfied clients may file lawsuits alleging negligence or breach of duty. Legal fees alone can devastate a small business, making E&O coverage a critical safeguard.

Georgia's business-friendly legal environment attracts companies across many different industries, but this growth brings increased professional liability exposure. State-specific considerations, including licensing requirements and regulatory mandates, make understanding E&O insurance particularly important for Georgia professionals.

Understanding E&O Insurance Fundamentals

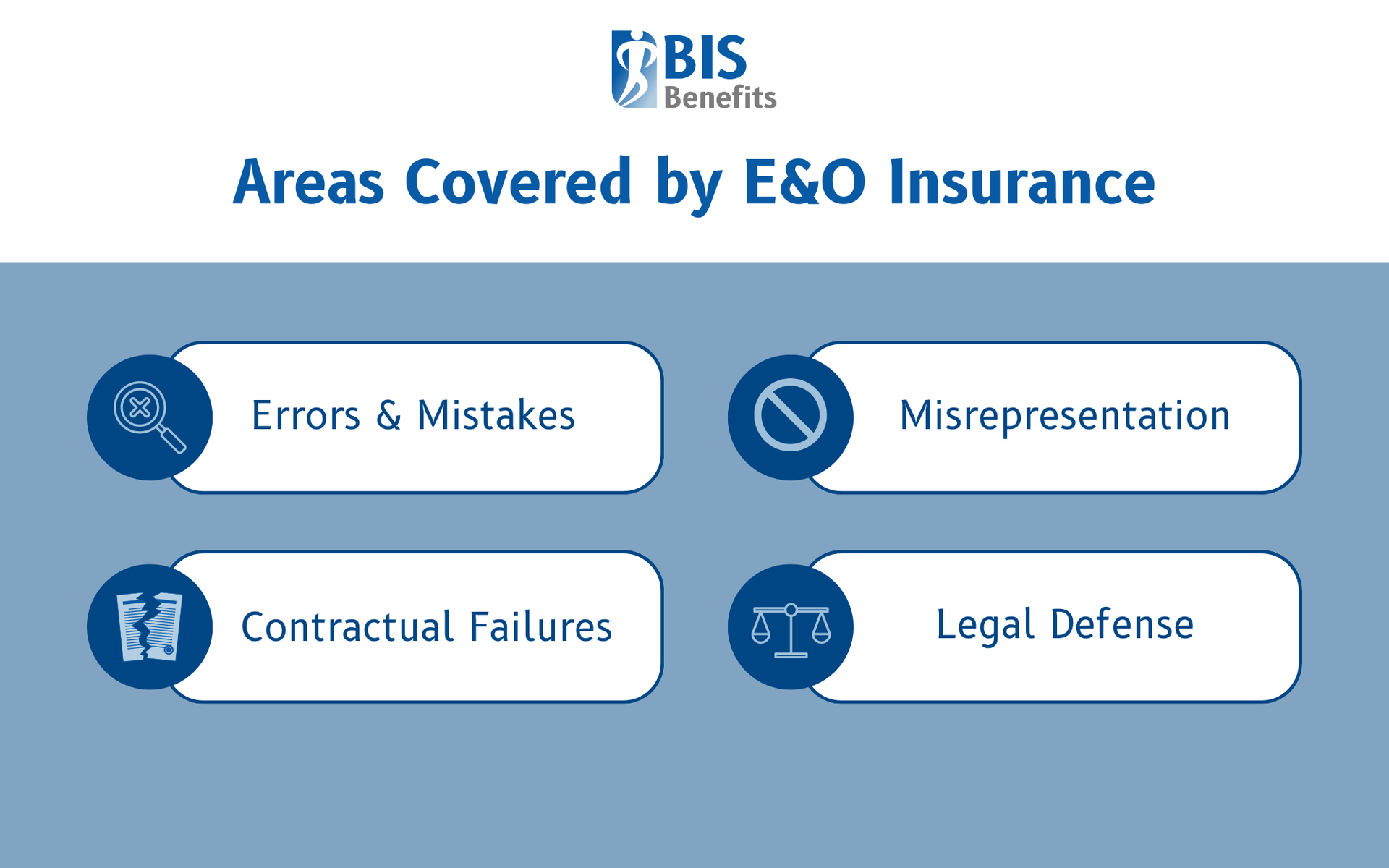

What E&O Insurance Covers

E&O insurance provides protection when clients allege that professional services caused them financial harm. Coverage typically includes:

- Professional Mistakes: E&O insurance covers a range of errors and negligent acts by the business.

- Contractual Failures: If a business fails to deliver promised services or meet contractual deadlines, E&O insurance provides protection.

- Misrepresentation: Breach of professional duty claims are covered when clients allege they received incorrect advice or inadequate information.

- Legal Fees: Even groundless claims require expensive legal defense, and most E&O policies cover court costs, attorney fees, expert witnesses, and settlements or judgments up to policy limits.

How Errors & Omissions Coverage is Different from General Liability

E&O insurance is fundamentally different from general liability coverage. General liability addresses bodily injury and property damage claims, physical accidents involving people or property. E&O covers professional negligence claims involving financial losses from inadequate services or advice. General liability policies exclude professional liability claims, leaving businesses without E&O coverage exposed to potentially catastrophic losses.

Claims-Made Policies

E&O policies typically use claims-made coverage triggers, meaning the policy in effect when a claim is filed provides coverage, regardless of when the alleged error occurred. General liability's occurrence-based coverage covers incidents occurring during the policy period regardless of when claims are filed. Understanding this distinction is crucial for maintaining continuous coverage and avoiding gaps.

Key Policy Components

Important elements of E&O policies include:

- Coverage limits specifying maximum amounts payable per claim and in aggregate during the policy period. Common limits range from $500,000 to $5 million depending on business size and risk exposure.

- Deductibles represent out-of-pocket amounts businesses pay before insurance coverage applies.

- Extended reporting periods, called "tail coverage," allow businesses to report claims after policy expiration for incidents that occurred during the policy period.

Claims-made coverage requires understanding retroactive dates, which is the earliest date for which coverage applies. Maintaining continuous coverage with the same retroactive date ensures protection for past work.

Georgia Industries That Need E&O Insurance

Professional Services

- Accounting: Tax preparers risk claims from preparation errors, missed deductions, or audit triggers.

- Architecture & Engineering: These professionals face liability for design errors, code violations, or project cost overruns.

- Medicine: The medical field requires malpractice insurance, a specialized form of E&O coverage.

- Technology & IT: Technology professionals risk liability from inadequate security implementations, system failures, or advice that leads to data loss.

- Insurance: Insurance agents and brokers risk claims from coverage gaps, policy misrepresentation, or failure to recommend appropriate coverage.

- Legal: Attorneys and law firms face E&O exposure from missed filing deadlines, inadequate legal research, conflicts of interest, and poor client communication.

- Real Estate: Real estate agents and brokers encounter claims from property disclosure issues, transaction delays, or valuation disputes.

- Consulting & Advising: Consultants face claims when their recommendations don't produce expected results, when implementations fail, or when clients suffer losses following their advice.

Georgia Legal Environment and Regulations

State Liability Laws

Georgia operates under modified comparative negligence rules, allowing plaintiffs to recover damages if they're less than 50% at fault for their losses. Professional standard of care requirements hold Georgia professionals to the standards reasonably expected of practitioners in their field. Statutes of limitations vary by claim type.

Regulatory Requirements

Georgia licensing boards for various professions establish minimum insurance requirements. The state maintains approved insurance carrier lists for certain regulated professions. Professionals must demonstrate compliance through a Certificate of Insurance or other documentation.

Court System Considerations

Recent legal precedents in Georgia have reevaluated premises liability and truth-in damages, making awareness of evolving case law important for risk management. Courts encourage

alternative dispute resolution for professional liability disputes, including mediation and arbitration.

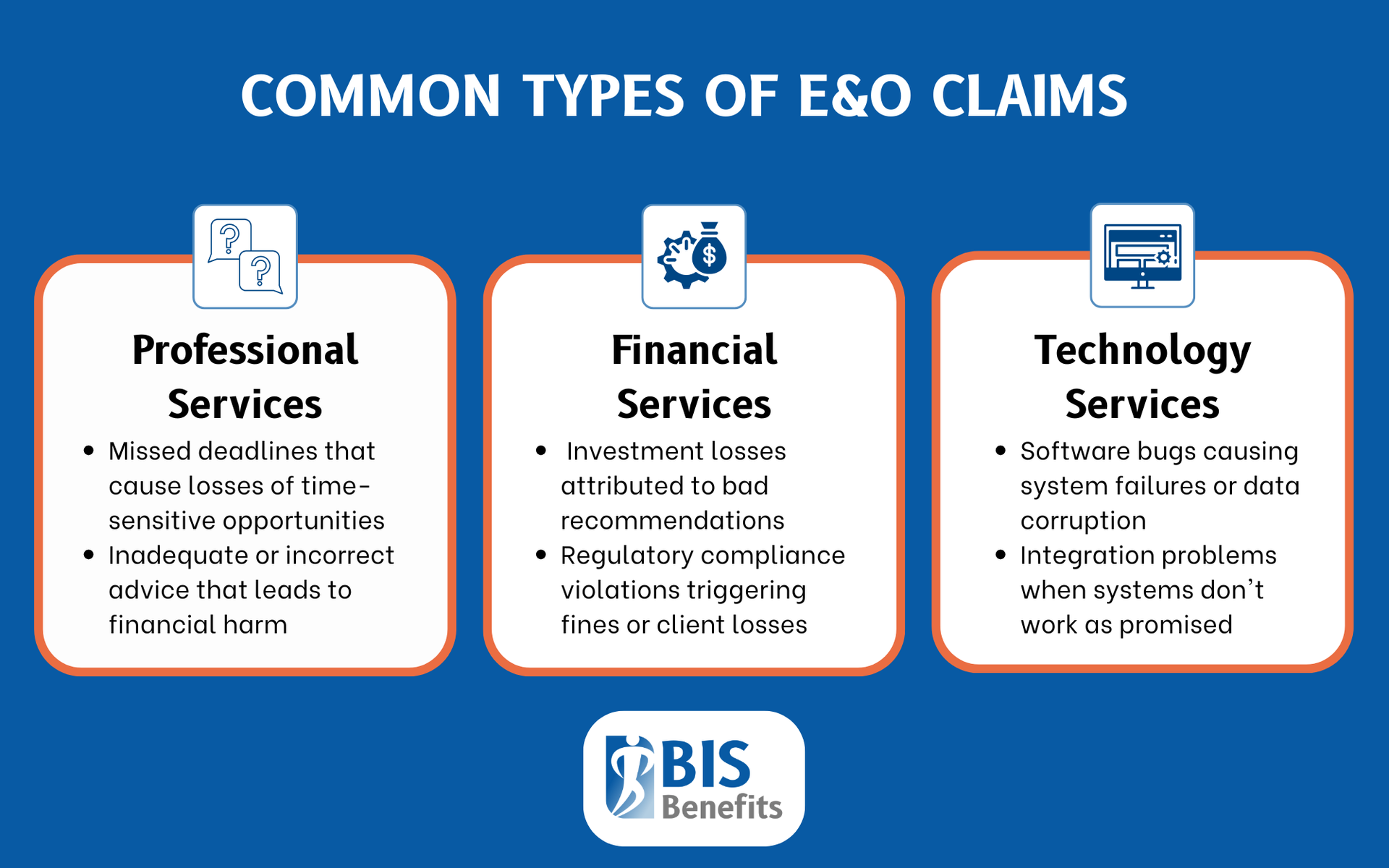

Common E&O Claims

Professional Service Failures

Missed deadlines cause client losses when time-sensitive opportunities are lost. Inadequate or incorrect advice leads to financial harm when clients rely on professional recommendations. Scope of work misunderstandings occur when deliverables don't match client expectations due to communication failures.

Technology-Related Claims

These stem from software bugs causing system failures or data corruption, data loss from inadequate backup systems, integration problems when systems don't work together as promised, and project delays that cause financial losses or missed market opportunities.

Financial Services Claims

These arise from investment losses attributed to bad recommendations, disclosure failures when material information isn't communicated, and regulatory compliance violations triggering fines or client losses.

Policy Features and Coverage Options

Standard E&O policies define covered professional services specifically, limiting coverage to services within stated business descriptions. Many policies include regulatory proceeding coverage for licensing board investigations. Some provide reputation management and crisis response services following claims.

Optional Endorsements

- Cyber Liability Coverage: Addresses data breaches and privacy violations.

- Employment Practices Liability: Covers discrimination and wrongful termination claims.

- Intellectual Property Coverage: Protects against infringement allegations.

Some policies offer regulatory fines and penalties coverage subject to insurability under law.

Policy Limits

E&O coverage limits can vary significantly. Defense costs may share policy limits or apply separately, affecting available coverage for settlements. Aggregate limits cap total payouts during the policy period while per-claim limits apply to individual claims.

Deductibles

Per-claim deductibles apply to each claim separately, while annual aggregate deductibles cap total deductible payments during the policy period. Defense cost deductible applications vary, since some policies apply deductibles only to settlements while others include defense costs.

Cost Factors and Premium Considerations

Determining factors for premium costs include:

- Industry Classification: Higher-risk professions often end up paying more.

- Business Size: Larger businesses face greater exposure, which can affect pricing.

- Claims History: This dramatically impacts costs, since claim-free businesses earn lower rates while those with losses pay premiums reflecting increased risk.

- Coverage Limits & Deductible Selections: These directly affect premiums, with higher limits and lower deductibles increasing costs.

Cost management strategies include:

- Implementing risk management programs

- Professional development for staff members

- Favorable client contract terms limiting liability exposure

- Claims-free discounts rewarding positive loss experience

Risk Management and Claims Prevention

Following best practices can help prevent claims before they occur.

- Clear client contracts documenting scope, deliverables, timelines, and limitations manage expectations from project inception.

- Regular communication and progress updates keep clients informed and identify issues early.

- Professional development and continuing education ensure current knowledge and best practices.

- Quality control and peer review processes catch errors before delivery to clients.

- Client relationship management proves essential.

- Setting and managing expectations prevents misunderstandings.

- Regular check-ins maintain alignment throughout engagements.

- Formal complaint handling procedures address issues before they escalate to litigation.

Selecting the Right E&O Coverage

Working with qualified insurance agents experienced in professional liability ensures appropriate coverage selection. Agents understanding industry-specific needs can identify coverage gaps and recommend suitable solutions. Comparing coverage options across carriers reveals differences in terms, exclusions, and pricing.

Coverage evaluation should consider insurance carrier financial strength to ensure claim-paying ability, claims handling reputation and processes, and policy terms, including coverage breadth and exclusions.

Trust BIS Benefits to Find the Right E&O Coverage

E&O insurance provides essential protection for Georgia businesses delivering professional services. The right coverage protects against financial devastation from professional liability claims while providing peace of mind to focus on serving clients.

BIS Benefits specializes in helping Georgia-based companies navigate

group benefits and

business insurance. Our experienced brokers understand industry-specific risks and Georgia's regulatory environment. We assess your business’s specific requirements, explain coverage options, and connect you with insurance carriers offering competitive rates and comprehensive protection. In addition to

E&O coverage, we also offer several other types of business insurance, including

general liability insurance,

commercial auto insurance, and

workers' compensation insurance.

If your Georgia business has 15 employees or more,

Request a Quote today to discover how BIS Benefits can help you find the right coverage solution.