2026 HSA Contribution Limits: What to Know

2026 HSA Contribution Limits: What to Know

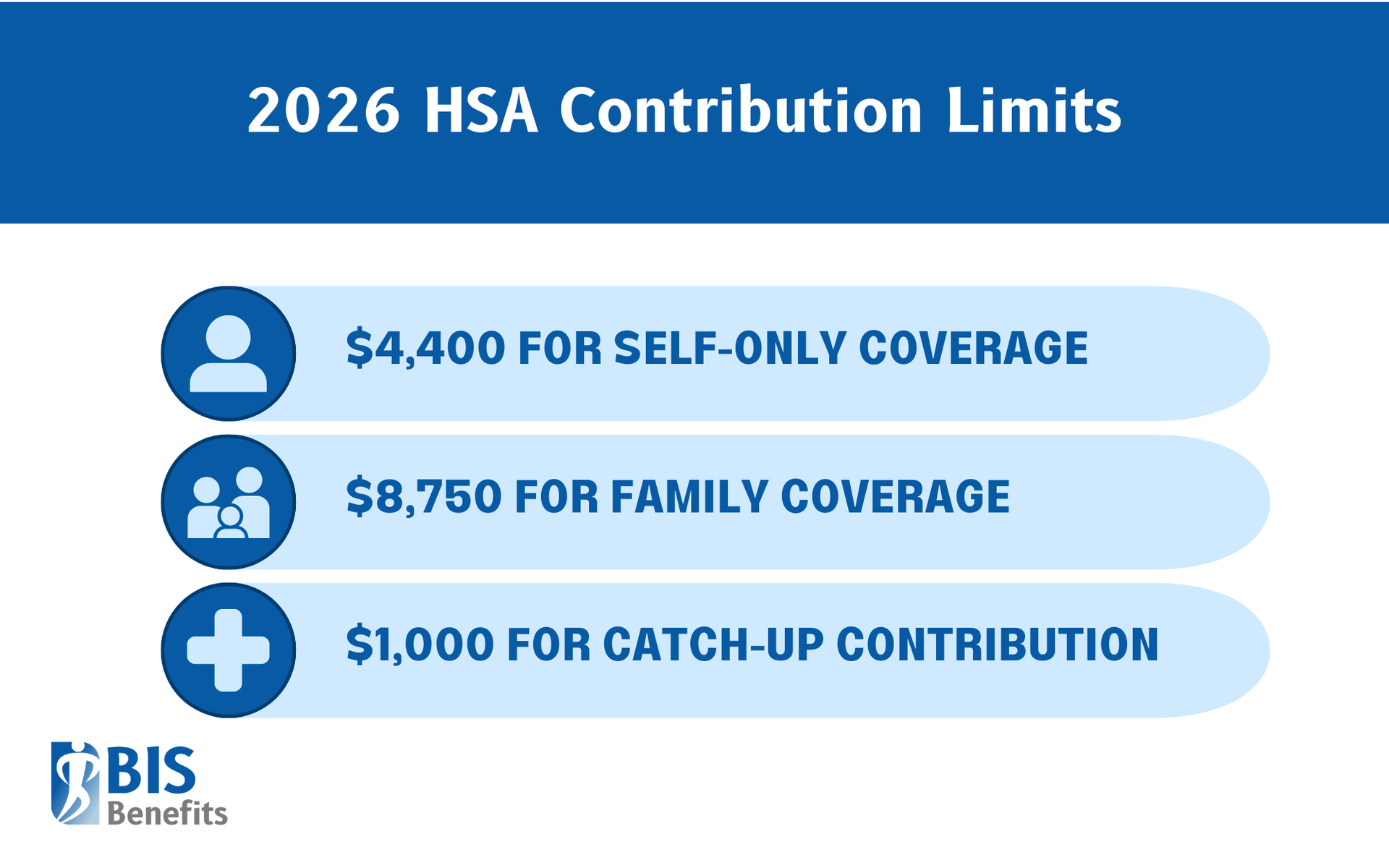

At a Glance: A Health Savings Account (HSA) is a tax-advantaged savings account for qualified medical expenses, available to individuals enrolled in a High Deductible Health Plan (HDHP). For 2026, the IRS has set contribution limits at $4,400 for individual coverage and $8,750 for family coverage, with an additional $1,000 catch-up contribution allowed for those age 55 and older.

Healthcare costs continue to rise, and for many individuals and families, finding ways to manage those costs efficiently has never been more important.

Health Savings Accounts, commonly known as HSAs, remain one of the most powerful tools available for saving money on healthcare while also reducing taxes. Because HSAs come with unique tax advantages, understanding how much you can contribute each year is critical to getting the most value out of them.

Each year, the

Internal Revenue Service (IRS) sets contribution limits for HSAs based on inflation and economic conditions. For 2026, those limits are increasing again, giving eligible individuals and families more room to save. Whether you are an employee enrolling in benefits or a business owner designing a benefits package, understanding these contribution limits can help you plan more effectively and avoid costly mistakes.

What Is a Health Savings Account (HSA)?

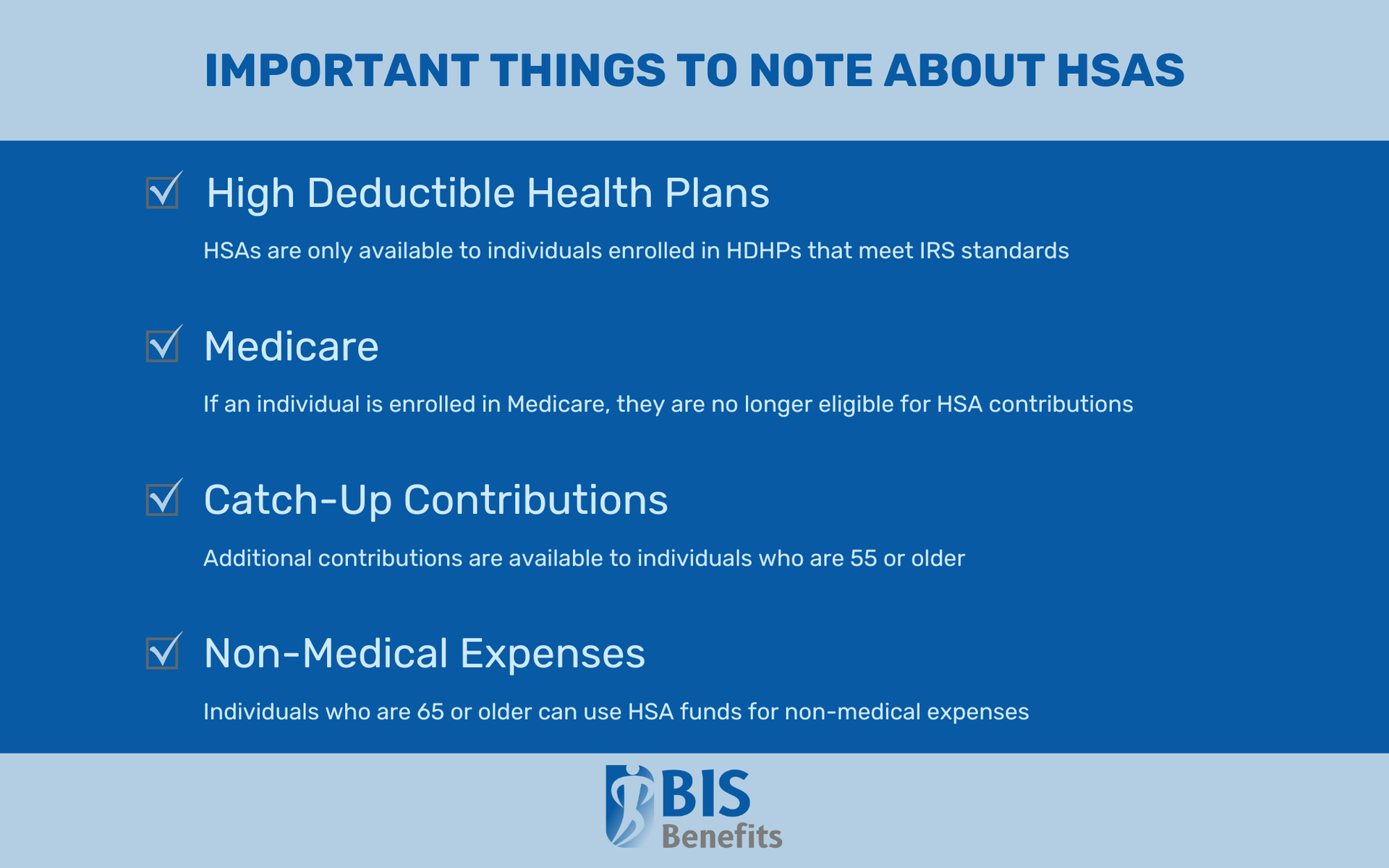

A Health Savings Account is a tax-advantaged savings account designed to help people pay for qualified medical expenses. HSAs are only available to individuals enrolled in an HSA-qualified High Deductible Health Plan (HDHP), but for those who are eligible, they offer significant financial benefits.

HSAs are often described as “triple tax-advantaged.” Contributions are made with pre-tax dollars or are tax-deductible if made outside of payroll. The money in the account grows tax-free through interest or investment earnings. When funds are withdrawn for qualified medical expenses, those withdrawals are also tax-free.

Unlike other healthcare accounts, HSAs are owned by the individual, not the employer. If you change jobs, retire, or move to a different health plan in the future, the account stays with you. There is no use-it-or-lose-it rule, and unused funds roll over year after year.

Many HSAs also offer investment options once a certain balance is reached, allowing account holders to grow their savings over time. After age 65, HSA funds can be used for

non-medical expenses without penalty, although those withdrawals are taxed as ordinary income. This makes HSAs a flexible tool for both healthcare spending and long-term financial planning.

HSA Eligibility Requirements

Not everyone can open or contribute to an HSA. Eligibility is determined by IRS rules and depends largely on the type of health coverage you have.

To be eligible for an HSA, you must be enrolled in an HSA-qualified HDHP. You cannot be enrolled in Medicare, and you cannot be claimed as a dependent on someone else’s tax return.

You also cannot have other disqualifying health coverage. This includes general-purpose healthcare

Flexible Spending Accounts (FSA) or

Health Reimbursement Arrangements (HRA) that pay for medical expenses before you meet your deductible. However, certain exceptions exist.

Limited Purpose FSAs, which cover only dental and vision expenses, and post-deductible HRAs are generally allowed and do not disqualify HSA eligibility.

Eligibility rules can become more complex for households with access to multiple benefits, so it is important to review plan details carefully during open enrollment.

2026 HSA Contribution Limits

For 2026, the IRS has increased the annual limits for HSA contributions to account for inflation.

The maximum contribution limit for individuals with self-only HDHP coverage is $4,400. Those with family coverage can contribute up to $8,750. These limits combine employee and employer contributions.

HSA contributions can be made through payroll deductions or directly to the account. Contributions for a given tax year can generally be made up until the tax filing deadline of the following year, which gives account holders additional flexibility if they want to top off their contributions after the year ends.

The IRS adjusts HSA contribution limits annually based on inflation, so increases from year to year are common. Staying aware of these changes helps ensure you are maximizing your available tax benefits.

2026 HSA Catch-Up Contributions

Account holders who are age 55 or older by the end of the calendar year are eligible to make an additional catch-up contribution. For 2026, the catch-up contribution limit is $1,000. Unlike the standard HSA limits, this amount is not indexed for inflation.

Catch-up contributions are allowed per individual. If both spouses are age 55 or older, each spouse must have their own HSA to make a catch-up contribution. A single HSA cannot receive two catch-up contributions, even if both spouses are eligible.

It is also important to note that

individuals enrolled in Medicare are no longer eligible to contribute to an HSA, including catch-up contributions. Timing Medicare enrollment carefully can help avoid unintended contribution penalties.

HDHP Requirements for HSA Eligibility in 2026

HSAs are only available to individuals enrolled in a High Deductible Health Plan that meets IRS standards. For 2026, an HDHP must meet both deductible and out-of-pocket maximum requirements.

The

minimum annual deductible for individual coverage is $1,700. For family coverage, the minimum deductible is $3,400. These are the amounts you must pay out-of-pocket before most plan benefits begin.

The maximum out-of-pocket limits for 2026 are $8,500 for individual coverage and $17,000 for family coverage. These limits cap the total amount you are responsible for paying through deductibles, copays, and coinsurance during the year.

Not all plans with high deductibles qualify as HDHPs, so it is important to verify that a plan is HSA-qualified before contributing.

Consequences of Overcontributing to an HSA

Contributing more than the annual HSA limit can lead to penalties. Excess contributions are subject to a 6% excise tax for each year the excess remains in the account.

The good news is that excess contributions can usually be corrected if addressed before the tax filing deadline. This typically involves withdrawing the excess amount and any associated earnings.

Tracking both personal and employer contributions throughout the year is essential to avoiding these issues, especially for individuals who change jobs or coverage midyear.

Employer HSA Contributions

Employers can contribute to employee HSAs as part of a benefits package. These contributions count toward the annual HSA limit and must be coordinated with employee contributions to avoid exceeding the maximum.

Employer contributions offer tax advantages for both parties. Contributions are tax-deductible for the employer and are not subject to payroll taxes. For employees, employer contributions are excluded from taxable income.

Common

employer contribution structures include flat annual contributions, matching employee contributions, or seed contributions made at the beginning of the year. These contributions can help offset the higher deductibles associated with HDHPs and encourage employee participation.

What Business Owners Should Know

For business owners, offering an HDHP paired with an HSA can be an effective benefits strategy. Employer HSA contributions can help attract and retain employees while reducing payroll tax liability. Employees need to understand eligibility rules, contribution limits, and how HSAs differ from FSAs or traditional health plans. A well-communicated HSA program can improve benefit satisfaction without significantly increasing benefit costs.

Strategies for Maximizing an HSA

- For those who can afford it, contributing the maximum allowed amount each year can create significant tax savings.

- Many people also choose to invest HSA funds once their account balance allows, treating the HSA as a long-term savings vehicle rather than a short-term spending account.

- Some account holders pay for current medical expenses out-of-pocket and let their HSA balance grow, saving receipts for future reimbursement.

- Coordinating HSA contributions with a spouse’s benefits and other tax-advantaged accounts can further improve overall savings.

Discover HSA Solutions & More with Group Benefits Brokers From BIS Benefits

An HSA can provide more opportunities to save for healthcare expenses while reducing taxes. With limits of $4,400 for individual coverage and $8,750 for family coverage, plus catch-up contributions for those 55 and older, HSAs remain one of the most flexible and valuable benefits available. By working with an experienced HSA broker, businesses can protect themselves and their employees and prepare for a prosperous future.

BIS Benefits is dedicated to helping Georgia-based businesses with 15 or more employees find the right

group benefits and

commercial insurance solutions. Our insurance brokers have years of experience and a full understanding of programs like

Flexible Spending Accounts and

Health Savings Accounts.

Request a Quote from BIS today to find out how we can help your business find the coverage that fits your needs.