How Does Management Liability Coverage Protect Businesses?

How Does Management Liability Coverage Protect Businesses?

In today's complex business environment, management decisions face intense scrutiny from shareholders, employees, regulators, and the public. A single allegation of mismanagement, discrimination, or breach of fiduciary duty can result in costly litigation that threatens both the company and the personal assets of its leaders.

Management liability coverage is a category of insurance designed to protect from lawsuits alleging wrongful acts, governance failures, or workplace violations. These potential risks are typically excluded from standard commercial general liability policies, leaving a significant gap in protection. While many business owners assume management liability is only for large corporations, companies of all sizes face these exposures and benefit from appropriate coverage.

What Is Management Liability Insurance?

Management liability insurance protects businesses and their leadership from claims related to management decisions and workplace practices. It covers directors, officers, managers, and the organization itself against allegations of wrongful acts committed in their official capacities.

This coverage pays for legal defense costs, settlements, judgments, and investigation expenses arising from covered claims. Unlike general liability insurance, which addresses bodily injury and property damage, management liability focuses specifically on the risks that come with running a business and making decisions that affect employees, shareholders, and other stakeholders.

Management liability is often structured as a package policy that bundles several related coverages together. This approach provides comprehensive protection against the various types of claims that can arise from business operations and leadership decisions.

How Management Liability Coverage Protects Businesses

One of the most important functions of management liability coverage is shielding leaders' personal assets. Directors and officers can be held personally liable for decisions made in their official capacity. Without coverage, personal assets such as homes, savings, and investments could be at risk in a lawsuit. Directors and Officers Insurance (D&O) protects individual leaders from personal financial ruin and provides peace of mind for those making difficult business decisions.

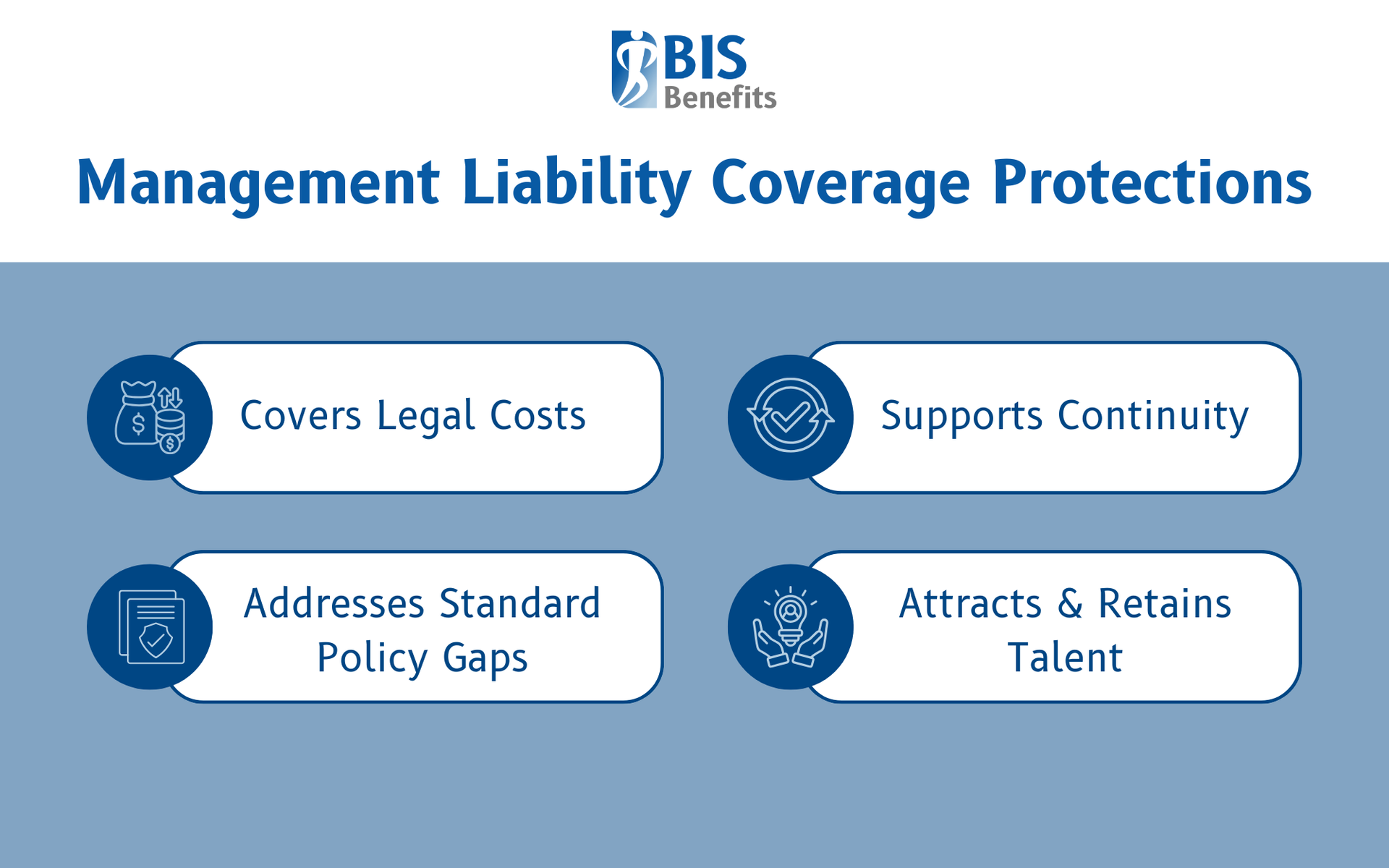

Covers Legal Costs

Management liability coverage also pays for defense costs, which can be substantial. Lawsuits involving management decisions are often complex and expensive to defend. Coverage pays for legal fees, attorney costs, expert witnesses, court expenses, settlements, and judgments. It also covers investigation costs related to regulatory inquiries or internal reviews. This protection applies regardless of whether the allegations are ultimately proven valid.

Addresses Gaps in Standard Policies

Commercial general liability policies typically exclude management-related claims, and standard business insurance does not cover allegations of mismanagement, discrimination, or fiduciary breaches. Management liability fills these critical coverage gaps and works alongside other policies to create a complete risk management program.

Supports Business Continuity

Costly legal battles can drain company finances and distract leadership from day-to-day operations. Uninsured claims may force businesses to divert resources away from growth and operations. Comprehensive coverage prevents lawsuits from threatening the company's financial stability and allows leadership to focus on running the business rather than managing litigation. It also helps protect company reputation and stakeholder confidence during legal challenges.

Attracts & Retains Talent

Many qualified directors, officers, and executives expect liability protection as part of their compensation package. Coverage demonstrates a commitment to protecting leadership from personal risk and makes it easier to recruit experienced board members and senior managers who might otherwise be reluctant to take on roles with significant personal exposure.

Key Components of Management Liability Coverage

Directors and Officers Liability insurance (D&O)

D&O insurance protects directors and officers from claims alleging wrongful acts in their management capacity. This coverage is important for both public companies, private companies, and non-profit companies. Common claims include breach of fiduciary duty, mismanagement, negligence, and failure to comply with regulations.

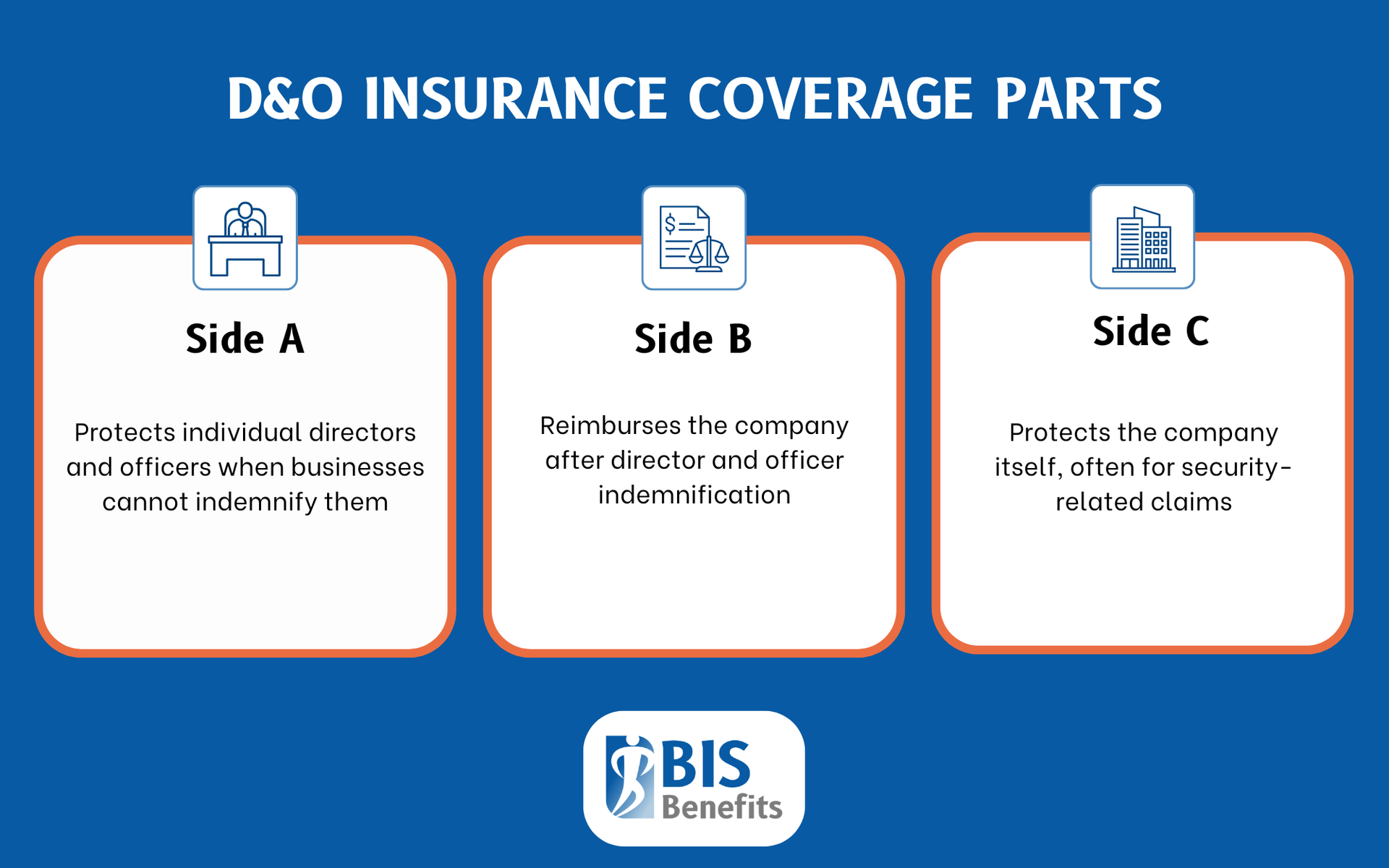

D&O coverage typically includes three coverage parts:

- Side A: Protects individual directors and officers when the company cannot indemnify them

- Side B: Reimburses the company when it indemnifies directors and officers

- Side C: Protects the entity itself, often for securities-related claims.

Employment Practices Liability (EPLI)

Employment practices liability insurance covers claims brought by employees, former employees, or job applicants. Common claims include discrimination, harassment, wrongful termination, retaliation, and failure to promote.

EPLI protects against claims based on race, gender, age, disability, religion, and other protected characteristics. One of the most frequently used components of management liability coverage, it covers defense costs and financial loss from employment-related lawsuits.

Fiduciary Liability Insurance

Fiduciary insurance coverage protects those responsible for managing employee benefit and retirement plans. It covers claims alleging breaches of fiduciary duty under the Employee Retirement Income Security Act (ERISA). Common claims include mismanagement of plan assets, failure to act in participants' best interests, and improper investment decisions. This coverage applies to 401(k) plans, pension plans, health plans, and other employee benefits.

Crime & Fidelity Coverage

Crime insurance policies protect against losses from internal fraud, embezzlement, theft, and dishonest acts by employees. It covers stolen money, securities, and property and may include coverage for computer fraud, funds transfer fraud, and social engineering schemes. This coverage is often bundled with management liability or available as standalone coverage.

Who Makes Claims Against Business Leadership?

Claims against business leadership can come from internal and external sources.

Internal Sources

Internal sources include employees alleging discrimination, harassment, wrongful termination, or hostile work environment. Shareholders may claim mismanagement, breach of fiduciary duty, or securities violations. Board members or partners may bring disputes over governance decisions, and benefit plan participants may allege fiduciary breaches related to retirement or health plans.

External Sources

External sources of claims include regulators investigating compliance failures or governance issues, competitors alleging unfair business practices, customers claiming deceptive practices or misrepresentation, creditors in bankruptcy or insolvency situations, and vendors or business partners in contractual disputes involving management decisions.

Common Triggers for Claims

Certain events commonly trigger management liability claims. These include:

- Mergers, acquisitions, or major corporate transactions

- Financial performance issues or missed projections

- Layoffs, restructuring, or workforce changes

- Regulatory investigations or compliance failures

- Changes in leadership or board composition

- Public controversies or reputational events

Considerations When Purchasing Management Liability Coverage

When purchasing management liability coverage, start by assessing your unique risk profile:

- Evaluate company size, industry, and governance structure

- Consider employment practices, workforce size, and HR policies

- Review benefit plans and fiduciary responsibilities, and identify areas of potential regulatory exposure

Risk Management

Management liability coverage should be integrated with your overall risk management strategy. It should complement other business insurance policies and coordinate with general liability, cyber liability, and professional liability coverage. Beyond insurance, implementing strong governance practices, HR policies, and compliance programs helps reduce risk in the first place. Coverage works best as part of a comprehensive approach to managing business risk.

Working with an Insurance Broker

Management liability policies can be complex. Experienced brokers help identify appropriate coverage limits and policy structures, ensure policy language addresses your specific exposures, and review exclusions and coverage limitations carefully. The right broker can help you avoid coverage gaps that could leave your business or leadership exposed.

Find the Right Business Insurance Coverage with BIS Benefits

Management liability coverage protects businesses and their leaders from costly claims related to management decisions, employment practices, and fiduciary responsibilities. It shields personal assets, covers legal expenses, fills gaps in standard policies, and supports business continuity during challenging legal situations.

In an environment of increased litigation, this coverage is valuable for businesses of all sizes. Working with an experienced insurance broker helps ensure your coverage adequately protects your business and leadership team.

At BIS Benefits, our brokers help Georgia-based businesses findmanagement liability coverage,

group health plans, and more insurance solutions tailored to their company's needs.

Request a Quote today to find out what BIS can do for you.