Different Types of Surety Bonds

Different Types of Surety Bonds

At a Glance: A surety bond is a legally binding three-party agreement that guarantees one party (the principal) will fulfill their obligations to another (the obligee), with a surety company backing that guarantee. Surety bonds fall into two primary categories: commercial bonds and contract bonds. Unlike insurance, the principal must repay the surety for any claims paid out, making surety bonds a form of credit rather than traditional loss protection.

A surety bond is a legally binding document that guarantees one party will fulfill their obligations to another, with a third party (the surety) backing that guarantee. Surety bonds fall into two primary categories: commercial bonds and contract bonds. Each serves different purposes across different industries, and requirements vary by industry, state, and specific circumstances. Understanding the different types available can be confusing, but knowing which bond applies to your situation is essential for meeting legal requirements and protecting the parties involved.

What Is a Surety Bond?

A surety bond is a legally binding three-party agreement that guarantees one party will meet their contractual obligations to another. If those obligations are not met, the bond provides financial protection to the party that was promised performance. This arrangement differs from insurance in important ways that affect how claims are handled and who ultimately bears responsibility.

The three parties in every surety bond are the principal, the obligee, and the surety.

- Principal: The party required to obtain the bond, such as a business owner, contractor, or fiduciary.

- Obligee: The party requiring the bond and protected by it, which may be a government agency, project owner, or court.

- Surety: The company issuing the bond and guaranteeing the principal's performance.

The surety bond process begins when an obligee requires a principal to obtain a bond. The principal applies to a surety company, which evaluates the principal's creditworthiness and risk. If approved, the surety issues the bond and the principal pays a premium. If the principal later fails to meet their legal obligations, the obligee can file a claim against the bond. The surety pays valid claims but the principal must repay the surety for any amounts paid out.

Surety Bonds vs Insurance

This repayment requirement is what distinguishes surety bonds from insurance. An insurance policy protects the policyholder from financial losses, and the insurance company absorbs covered losses. Surety bonds protect the obligee (a third party) from losses, and the principal must repay claims to the surety. In essence, the surety is extending credit to the principal, guaranteeing their performance to the obligee.

Commercial Surety Bonds

Commercial bonds are a broad category covering many bond types required by government agencies and regulatory bodies. These bonds protect the public and consumers from business misconduct and ensure businesses operate in compliance with laws and regulations. Premiums for commercial bonds are based on the bond amount and the principal's credit history.

Many industries require commercial bonds as a condition of doing business, such as:

- Auto dealers and motor vehicle businesses

- Construction trades

- Mortgage brokers and financial services companies

- Collection agencies

- Freight brokers and transportation companies

- Healthcare providers

- Security services

License and Permit Bonds

License and permit bonds are the most common type of commercial surety bond. These bonds are required to obtain certain business licenses or permits and guarantee that the business will comply with state and local laws. They protect consumers and the public from business misconduct by providing a financial guarantee if a business violates regulations.

Common license and permit bonds include contractor license bonds, auto dealer bonds, mortgage broker bonds, and tax preparer bonds.

During the process, a business applies for a license that requires a bond, obtains the bond from a surety company, and submits it to the licensing authority with the application. The bond remains active throughout the license period. If the business violates regulations, affected parties can file claims against the bond.

Fiduciary Bonds

Fiduciary bonds, also called probate bonds, are required when someone is appointed to manage another person's assets. These court-ordered bonds protect wards, creditors, and heirs from mismanagement or theft by ensuring fiduciary responsibility.

Fiduciary bonds ensure proper management of assets under fiduciary control and protect beneficiaries from theft, fraud, or mismanagement. They provide financial recourse if the fiduciary breaches their duties and give courts an oversight mechanism for asset management. The bond amount is typically based on the value of the estate or assets being managed.

The process begins when a court appoints an individual as fiduciary and requires a bond to protect interested parties. The fiduciary obtains the bond from a surety company, and if they mismanage assets, beneficiaries can file claims. The bond remains active until fiduciary duties are completed and the court releases the fiduciary from their responsibilities.

Court Bonds

Court bonds, also called judicial bonds, are required during legal proceedings to protect parties from potential losses in litigation. Courts order these bonds to ensure financial responsibility and balance the interests of both parties involved. They provide financial security during a court proceeding and protect parties from potential losses while ensuring compliance with court orders.

Common court bonds include:

- Appeal Bonds: Guarantee that a party appealing a judgment will pay if the appeal fails

- Attachment Bonds: Protect defendants when their property is attached before trial

- Injunction Bonds: Protect defendants if an injunction is later found to be wrongful

Contract Surety Bonds

Contract surety bonds are primarily used in the construction industry to guarantee contractors will fulfill their contract obligations. These bonds protect project owners from contractor default and are required for most public construction projects. Many large private projects also require contract bonds to protect the owner's investment.

Contract bonds exist because construction projects involve significant financial risk. Project owners need assurance that contractors can complete the work they have been hired to perform. Bonds provide financial protection if a contractor fails to deliver, and public agencies are required to protect taxpayer investments through bonding requirements. Additionally, subcontractors and suppliers need protection to ensure they receive payment for their work and materials.

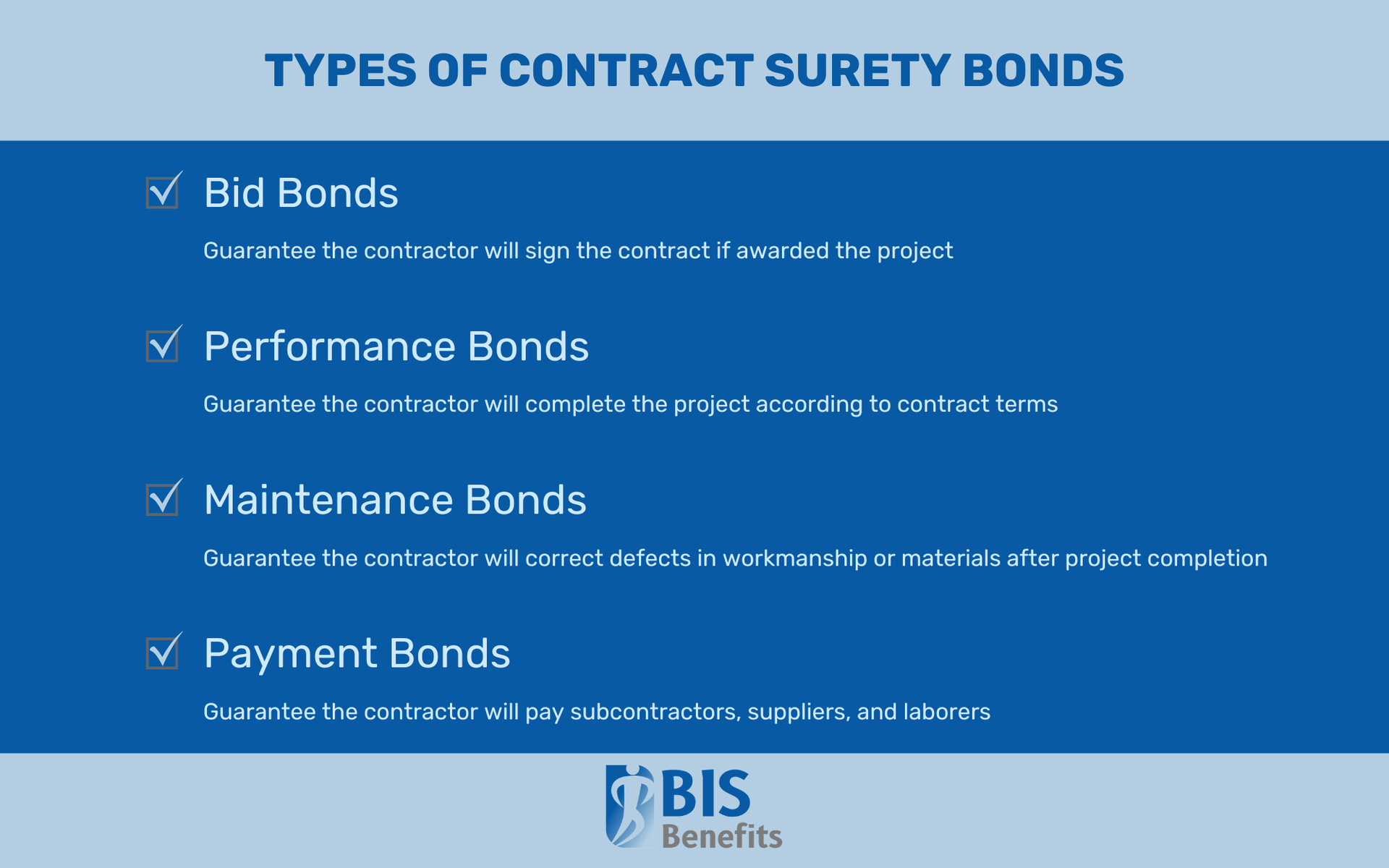

The main types of contract bonds are bid bonds, performance bonds, maintenance bonds and payment bonds. These are often required together for public construction projects, forming a complete package of protection for the project owner and all parties involved in the construction process.

Bid Bonds

Bid bonds are submitted with a contractor's bid on a project. They guarantee that the contractor will sign the contract if awarded the project and can provide the required performance and payment bonds. Bid bonds protect project owners from bid shopping and withdrawal by ensuring only serious, qualified contractors submit bids.

The project owner requires a bid bond with bid submission, and the contractor obtains the bond from a surety before bidding. Bid bonds are typically set at 5-10% of the bid amount. If the contractor wins and signs the contract, the bid bond is released. However, if the contractor fails to sign or cannot provide the required performance and payment bonds, the owner can file a claim against the bid bond. The claim covers the difference between the winning bid and the next lowest bid the owner must accept.

Performance Bonds

Performance bonds guarantee that a contractor will complete a project according to the contract terms. They protect project owners from contractor default during construction and ensure work meets specifications, quality standards, and timeline requirements. Performance bonds are typically required along with payment bonds when the contractor signs the construction contract.

The bond amount typically equals the full contract value, providing 100% coverage. If a contractor defaults, the owner notifies the surety, which investigates the claim and determines its validity. The surety may complete the project using another contractor, hire a replacement contractor directly, or pay the owner to arrange completion. The original contractor is responsible for repaying the surety for any claims paid.

Claims against performance bonds occur when a contractor abandons a project, fails to meet quality standards, cannot complete the project on time, becomes insolvent or bankrupt, or otherwise breaches the contract terms. The performance bond ensures the project owner is not left with an incomplete project and no recourse.

Maintenance Bonds

Maintenance bonds, also called warranty bonds, guarantee that a contractor will correct defects in workmanship or materials that appear after project completion. They protect project owners during a specified warranty period, typically one to two years following substantial completion. Maintenance bonds ensure that if problems arise due to faulty construction, the contractor will return to make necessary repairs at no additional cost to the owner.

The bond amount is usually a percentage of the contract value, often ranging from 10% to 50% depending on project requirements. If defects appear during the warranty period and the contractor fails to address them, the project owner can file a claim against the maintenance bond. The surety then arranges for repairs or compensates the owner for the cost of correcting the defects. This protection gives project owners peace of mind that their investment is covered beyond the completion date, holding contractors accountable for the quality and durability of their work.

Payment Bonds

Payment bonds guarantee that a contractor will pay subcontractors, suppliers, and laborers who provide work and materials to the project. They protect those who contribute to the project and prevent mechanic's liens from being filed against the property. Payment bonds are required alongside performance bonds on public projects.

Payment bonds ensure subcontractors and suppliers get paid for their contributions and protect project owners from mechanic's liens that could cloud title to the property. On public projects where liens cannot be filed against government property, payment bonds provide an alternative recourse for unpaid parties. This keeps payment disputes from affecting project completion.

The bond amount typically equals the contract value. If a contractor fails to pay a subcontractor or supplier, they can file a claim against the payment bond. The surety investigates and pays valid claims, and the contractor is responsible for repaying the surety. This system protects all parties involved in the construction process while ensuring projects can proceed without payment disputes causing delays.

Find the Right Insurance or Bonding Solution for Your Needs with BIS

Commercial bonds, including license and permit bonds, fiduciary bonds, and court bonds, protect consumers and the public from business misconduct and ensure proper management of assets and legal proceedings. Contract bonds, including bid bonds, performance bonds, and payment bonds, protect project owners and construction industry participants from contractor default and payment failures.

Understanding which types of bonds apply to your situation helps you meet requirements and obtain appropriate protection. Requirements vary by industry, state, and specific circumstances, so consulting with a surety bond professional can help determine which bond type meets your specific needs.

At BIS Benefits, we can help businesses with 15 employees or more navigate

surety bonds,

commercial insurance,

group benefits, and more.

Request a Quote today to get in touch with one of our expert insurance brokers.