How Does Group Health Insurance Differ From Individual Health Insurance?

How Does Group Health Insurance Differ From Individual Health Insurance?

At a Glance: Group health insurance is provided through an employer who selects the plan and pays a portion of premium costs, while individual health insurance is purchased directly by a person who pays the full premium. Group coverage offers lower costs and simplified enrollment but is tied to employment, while individual coverage provides portability and customization but often has higher out-of-pocket expenses.

Choosing the right health insurance is one of the most important financial and healthcare decisions you can make. Health insurance generally falls into two main categories: group coverage provided through an employer or organization, and individual coverage purchased directly by the person seeking protection. Each type has distinct advantages and trade-offs that affect cost, flexibility, and portability.

Understanding the differences between group and individual health plans matters whether you are an employee evaluating benefits, a business owner considering coverage options, or a self-employed professional shopping for a plan.

What Is Group Health Insurance?

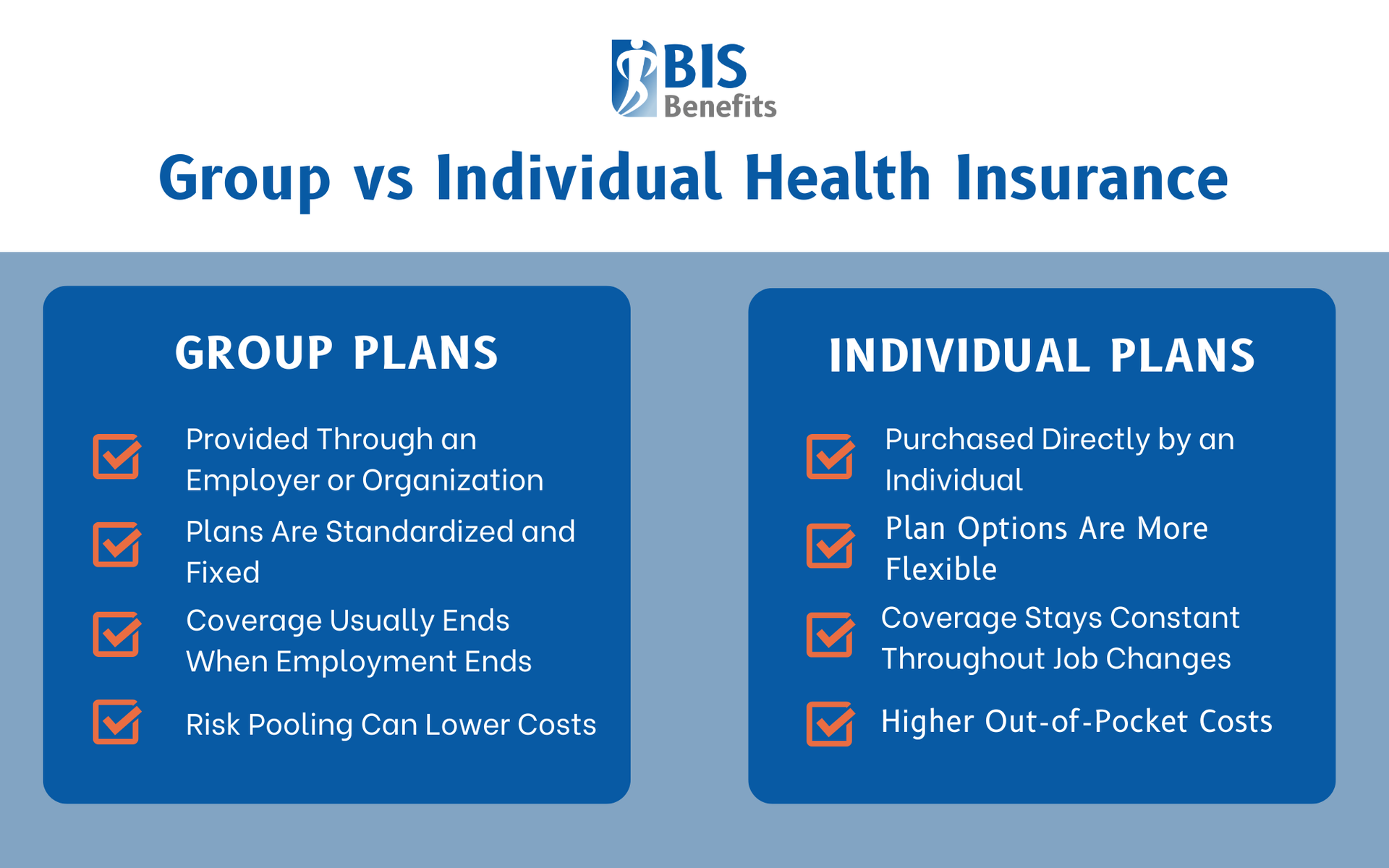

Group health insurance is coverage provided through an employer or organization. The employer sponsors the plan, selects coverage options, and typically contributes to premium costs on behalf of employees. Risk is spread across all employees in the group, which generally lowers per-person costs compared to individual coverage. Common sponsors include employers, unions, professional associations, and other organizations.

Key Characteristics of Group Health Insurance

Group health insurance has several key characteristics:

- The employer or organization purchases and administers the plan, and employers usually pay a significant portion of premiums, often 50 to 80 percent or more.

- Larger groups spread risk effectively, often resulting in lower individual costs.

- Plans are standardized with limited options and fixed benefits, deductibles, and provider networks.

- Coverage cannot be denied or priced higher for pre-existing conditions

- Employee premiums are typically paid with pre-tax dollars, reducing taxable income.

Employer-sponsored coverage generally ends when employment ends, though Continuation of Health Coverage (COBRA) allows temporary continuation at full cost.

What Is Individual Health Insurance?

Individual health insurance is coverage purchased directly by an individual rather than through an employer. The person selects and purchases a plan from an insurance carrier or through the Affordable Care Act (ACA) health insurance marketplace. Common purchasers include self-employed individuals, freelancers, gig workers, early retirees, and those whose employers do not offer coverage. Plans are available during Open Enrollment periods or after qualifying life events through the marketplace, with some plans available year-round.

Key Characteristics of Individual Health Insurance

Individual health insurance has its own distinct characteristics:

- The individual purchases and owns the policy directly and pays 100 percent of premiums without employer contribution.

- Many people qualify for government subsidies through premium tax credits based on income when purchasing through the ACA health insurance marketplace.

- Individual coverage offers a high degree of flexibility to choose plans, coverage levels, networks, and benefits that fit specific needs.

- ACA-compliant plans cannot deny coverage or charge more for pre-existing conditions.

- Coverage stays with you regardless of job changes, moves, or life transitions.

Premiums are generally paid with after-tax dollars unless using specific arrangements like Individual Coverage Health Reimbursement Arrangement (ICHRA) or the self-employed health insurance deduction.

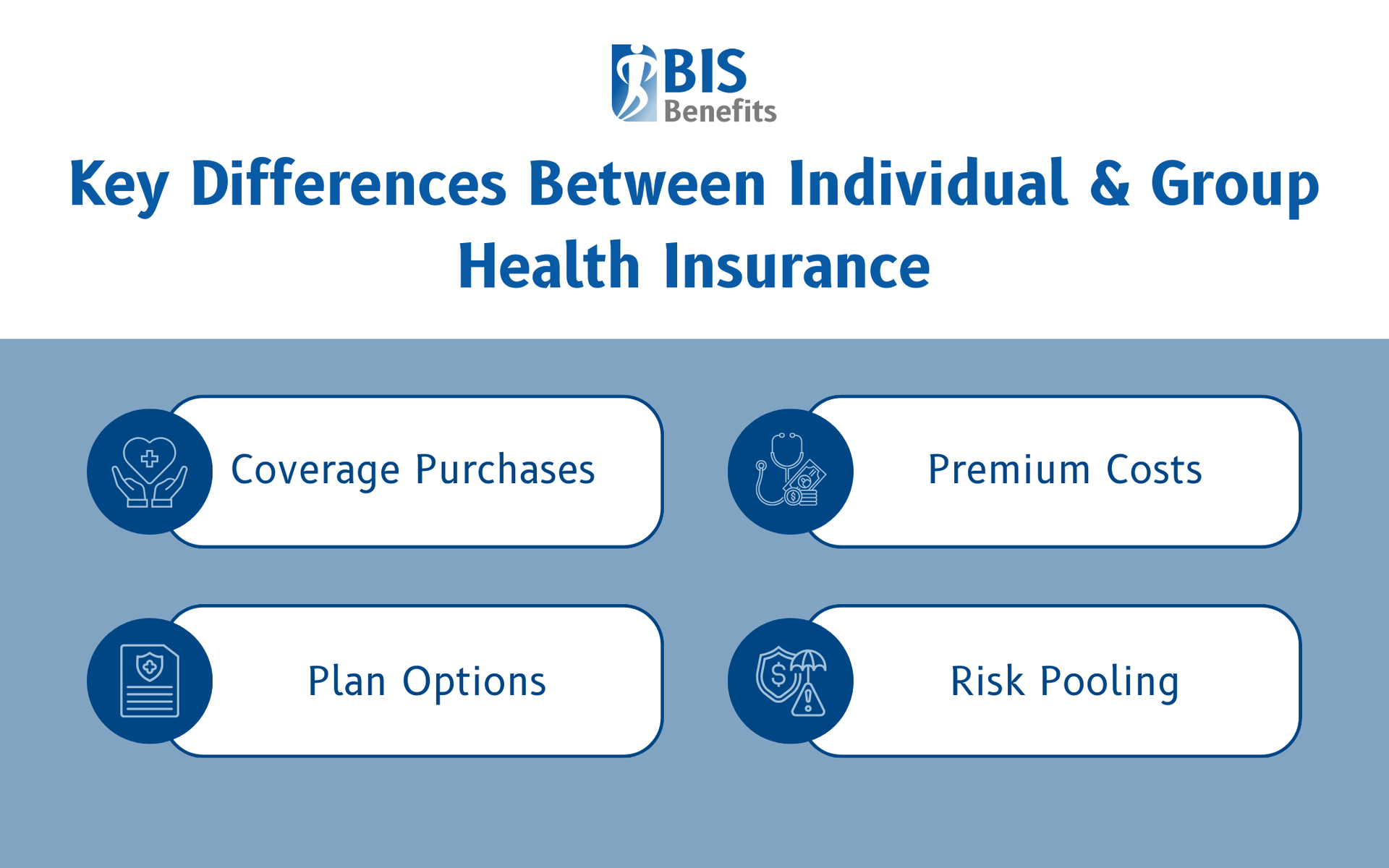

Key Differences Between Group and Individual Health Insurance

Coverage Purchases

With group insurance, the employer or organization selects and sponsors the plan, making coverage decisions on behalf of employees. With individual insurance, the person seeking coverage purchases directly from a carrier or marketplace and makes all decisions about plan selection.

Premium Costs & Sharing

Group insurance typically involves the employer paying a large portion of premiums, which reduces employee out-of-pocket costs. Individual policyholders pay the full premium, though subsidies may be available based on income. Group plans often have lower per-person costs due to risk pooling and employer contributions. Individual plans may be more expensive without subsidies but can be quite affordable with tax credits for those who qualify.

Risk Pooling

Group insurance spreads risk across all eligible employees, which can lower costs and stabilize premiums for everyone in the group. Larger employer groups often benefit from more favorable rates. Individual coverage assesses risk individually or within marketplace risk pools, though ACA regulations limit how much this affects pricing.

Plan Options

Group health plans are standardized with limited options since the employer chooses available plans. Individual coverage is highly customizable, allowing you to select specific plans, coverage levels, deductibles, and provider networks.

Portability

Group coverage is tied to employment and typically ends when you leave the job. COBRA allows temporary continuation coverage, but at full cost plus an administrative fee. Individual coverage stays with you regardless of employment changes, eliminating gaps when changing jobs, moving, or transitioning careers.

Tax Treatment

Group insurance employee premiums are often paid pre-tax through payroll deduction, and employer contributions are tax-advantaged. Individual insurance premiums are typically paid with after-tax dollars, though self-employed individuals may deduct premiums and ICHRA allows pre-tax treatment for some individual coverage.

Pros and Cons of Group Health Insurance

Pros

- Lower costs result from employer contributions and risk pooling across the employee population.

- Pre-tax premium payments reduce your taxable income.

- Enrollment is simplified through the employer, with no individual underwriting or health questions required.

- Group plans often include additional benefits like dental, vision, and life insurance, and the administrative burden is handled by the employer.

Cons

- Plan choices and customization options are limited to what the employer offers.

- Coverage is tied to employment and ends when you leave.

- Available plans may not fit your specific individual or family healthcare needs.

- Dependent coverage costs may be high, and you have no control over plan changes made by the employer from year to year.

Pros and Cons of Individual Health Insurance

Pros

- Individual options offer full control over plan selection and coverage options.

- Portability means coverage stays with you regardless of job changes.

- There is greater flexibility and more opportunities to tailor coverage to your specific healthcare needs and preferences.

- Government subsidies may be available to lower costs for those who qualify.

- You are not dependent on employer offerings or decisions, and coverage is available to self-employed workers, freelancers, and those without employer coverage.

Cons

- You pay the full premium without employer contribution, which can be expensive without subsidies.

- Finding the right plan requires research and decision-making during enrollment periods.

- You handle administrative tasks and interactions with the insurer directly.

- Enrollment is generally limited to Open Enrollment periods unless you meet the eligibility requirements for a Special Enrollment Period due to a qualifying life event.

Which Health Insurance Coverage Is Right for You?

Group insurance may be the best choice if you:

- Have employer-offered coverage with a meaningful premium contribution

- Prefer lower out-of-pocket costs and simplified enrollment

- Are comfortable with standardized plan options

- Value the convenience of employer-administered health benefits

- Consider your healthcare needs to be generally well-served by the available plan options

Individual insurance may be better if you:

- Are self-employed, a freelancer, or a gig worker without access to employer coverage

- Do not have health coverage through your employer or the available options do not meet your needs

- Need specific coverage options not available through group plans or are supplementing group coverage for yourself or dependents

Some individuals combine both options, using group coverage as primary insurance while adding individual supplemental policies. Families may split coverage between employer plans and marketplace options depending on costs and needs. Evaluate total costs, coverage quality, and flexibility when making decisions about how to structure your health insurance.

Find the Right Fit with a Benefits Broker

Group and individual health insurance each have distinct advantages depending on your situation. Group coverage offers lower medical expenses through employer contributions and risk pooling, but it provides less flexibility and portability. Individual coverage offers customization and portability but comes with higher premiums unless you qualify for subsidies. Evaluate your employment situation, healthcare needs, budget, and priorities when deciding which option is right for you.

Consulting with a benefits advisor can help you find the health insurance plan that best fits your needs. AT BIS Benefits, ouremployee benefits brokers help Georgia businesses with at least 15 employees find the insurance options that best fit their needs.

Request a Quote to get in touch with one of our experts today.