Should Your Nonprofit Have D&O Insurance?

Should Your Nonprofit Have D&O Insurance?

At a Glance: Most nonprofits should have D&O insurance because volunteer board members can be held personally liable for decisions made on behalf of the organization. D&O coverage protects directors, officers, and the organization itself from claims alleging mismanagement, breach of fiduciary duty, regulatory violations, and employment-related issues.

Nonprofit board members and officers often assume they are protected from personal liability because they serve without compensation, but this assumption can be costly. Directors and officers insurance, commonly known as D&O insurance, protects nonprofit leaders from claims alleging mismanagement, breach of fiduciary duty, or other wrongful acts committed in their leadership capacity.

Nonprofits face many of the same liability risks as for-profit organizations, and in some cases face unique exposures related to donor expectations, regulatory compliance, and charitable asset management. For organizations that rely on volunteer leadership, understanding D&O coverage is important for protecting both the individuals who serve and the organization itself.

What Is D&O Insurance for Nonprofits?

Directors & Officers Liability Insurance protects directors, officers, and the organization from claims alleging wrongful acts in their management capacity. It covers legal defense costs, settlements, and judgments, and is designed to protect the personal assets of board members as well as organizational resources. Coverage amounts can range from $500,000 to over $5 million depending on the size and risk profile of the organization.

What It Covers

A D&O policy protects board members, executive directors and officers, committee members and volunteers in leadership roles (depending on the specific policy), and the nonprofit organization itself through entity coverage. This protection covers allegations of mismanagement or poor decision-making, breach of fiduciary duty, failure to comply with regulations, employment-related claims in some policies, and errors in financial reporting or governance.

Coverage Exclusions

Criminal acts or intentional misconduct are usually excluded, as are claims covered by other policies such as general liability or employment practices liability. Bodily injury and property damage fall under general liability coverage, and known claims or pending litigation before the policy begins are also excluded. Professional liability for services provided may need separate coverage.

Why Nonprofits Need D&O Insurance

Risks for Board Members

Volunteer board members can be held personally liable for decisions made on behalf of the organization. Without coverage, personal assets such as homes, savings, and investments could be at risk in a lawsuit. Volunteer status does not eliminate liability exposure, and qualified candidates may hesitate to serve on a board without liability protection in place.

Unique Risks for Nonprofits

Nonprofits face accountability pressure from regulators, donors, and the public. They carry fiduciary responsibilities for managing charitable assets, make employment decisions affecting staff and volunteers, and must comply with state and federal nonprofit regulations. Fundraising practices and donor expectations create additional areas where claims can arise.

Limited Statutory Protections

Statutory protections typically do not cover gross negligence or willful misconduct, and legal fees can be substantial even when claims are ultimately dismissed. The Volunteer Protection Act provides some immunity but has significant limitations. State charitable immunity laws vary widely and may not apply in all situations.

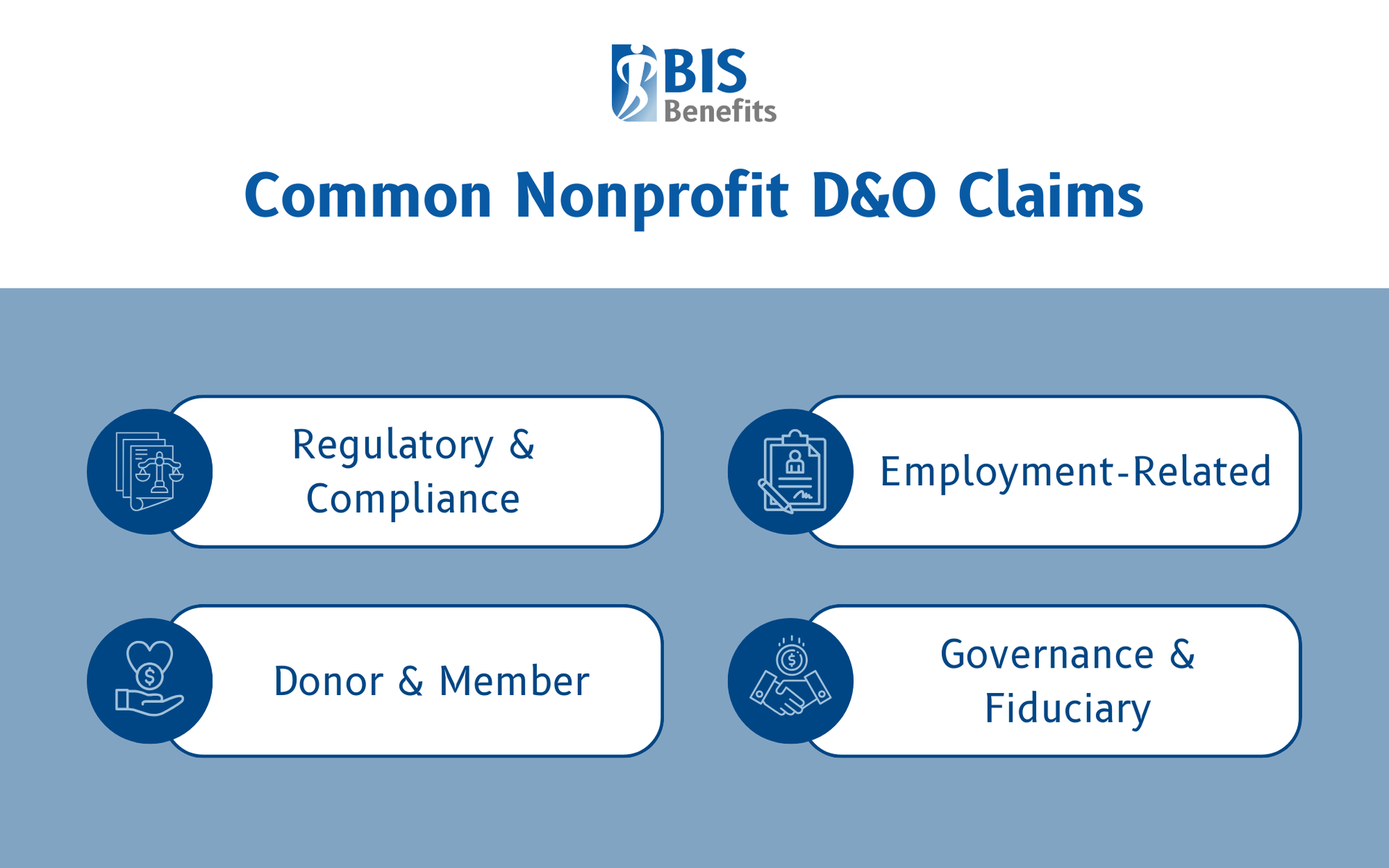

Common D&O Claims Against Nonprofits

Governance & Fiduciary Claims

These include allegations of mismanagement of funds or assets, conflicts of interest, failure to oversee executive compensation, poor investment decisions affecting endowments or reserves, and self-dealing by board members or officers. Any decision that appears to prioritize personal interests over the organization's mission can lead to claims.

Employment-Related Claims

These include wrongful termination of an executive director or staff, discrimination or harassment allegations, retaliation claims, and failure to follow employment policies. Even organizations with strong HR practices can face employment claims, and defense costs add up quickly.

Regulatory & Compliance Claims

These claims arise from failure to file required reports such as Internal Revenue Service (IRS) Form 990 or state registrations, misuse of restricted funds or grant violations, violation of charitable solicitation laws, and non-compliance with tax-exempt status requirements. Regulators and state attorneys general actively oversee nonprofit compliance, and violations can result in claims against leadership.

Donor & Member Claims

These include misrepresentation in fundraising materials, failure to use funds as donors intended, breach of fiduciary duty to members in membership organizations, and disputes over organizational direction or governance decisions.

Third-Party Claims

Claims from vendors, contractors, partner organizations, or beneficiaries alleging harm from organizational decisions also fall under D&O coverage.

Who Should Consider Nonprofit D&O Insurance?

Certain organizations should prioritize D&O coverage:

- Nonprofits with paid staff and employment relationships

- Organizations with significant assets or endowments

- Nonprofits that receive government grants or contracts

- Organizations with active fundraising programs

- Nonprofits operating in regulated industries such as healthcare, education, or social services

Smaller Nonprofits & Startups

Even small organizations face liability exposure, and limited resources make uninsured claims more damaging. Coverage demonstrates professionalism to donors and funders and helps attract qualified board members who expect protection before agreeing to serve.

Organizations Undergoing Transitions

Mergers, acquisitions, or dissolutions create situations where claims are more likely. Leadership transitions can lead to disputes between incoming and outgoing leaders. Program expansions into new areas may create new exposures, and financial difficulties increase scrutiny and potential claims from creditors or stakeholders.

How Much D&O Coverage Does a Nonprofit Need?

D&O coverage should reflect potential defense costs plus settlement exposure. Several factors influence appropriate coverage limits, including:

- Organization size measured by budget, staff, and assets

- Scope of operations and programs

- Number of board members and officers

- Risk profile and claims history

- Industry or sector-specific exposures

Balancing Cost & Protection

Higher limits provide greater protection but increase premiums. Deductibles affect both premium cost and out-of-pocket exposure when claims occur. Consider worst-case scenarios when evaluating limits, and review coverage annually as the organization grows or changes.

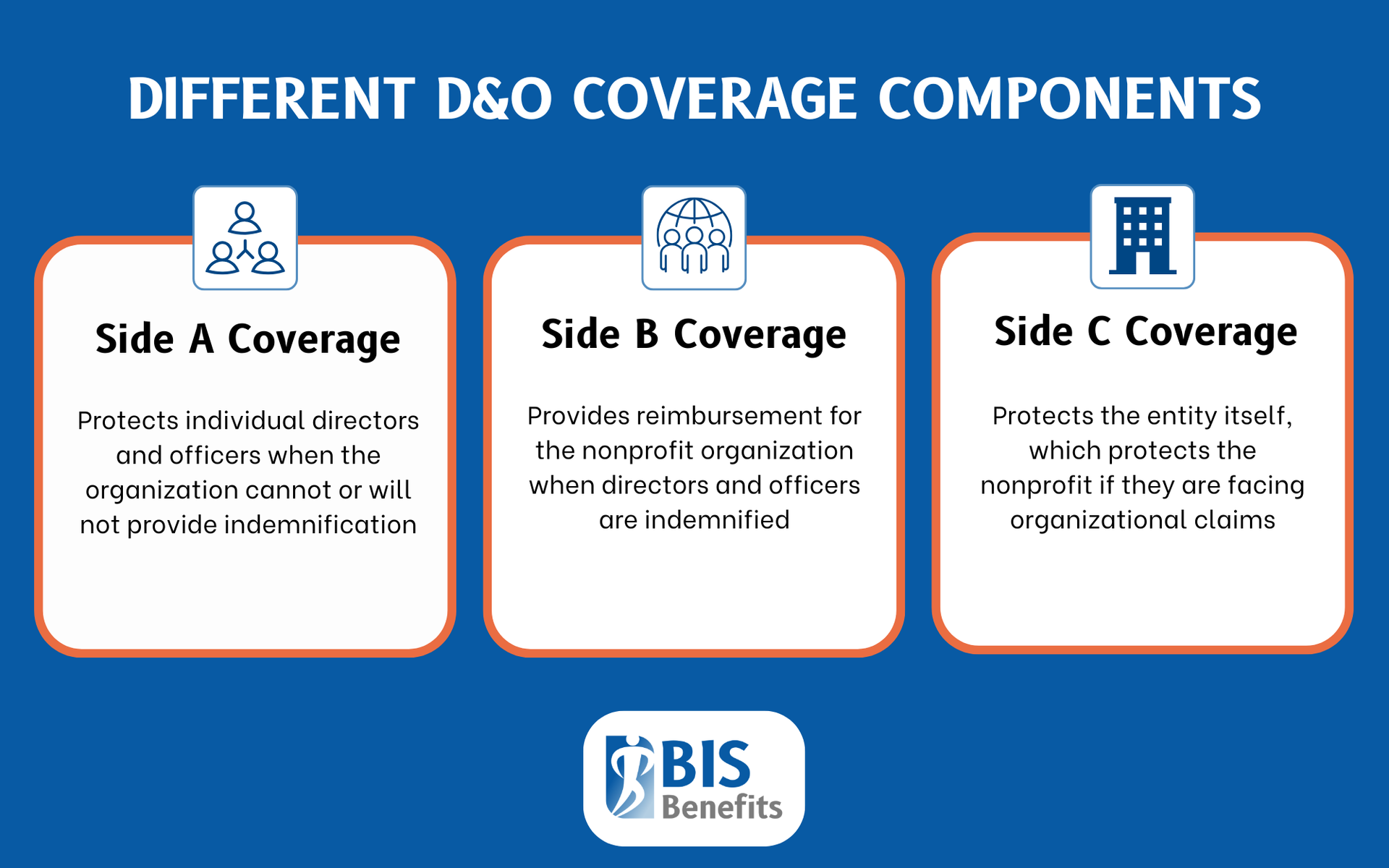

Key Insurance Policy Features to Look For

D&O policies include different coverage components:

- Side A Coverage: Protects individual directors and officers when the organization cannot or will not indemnify them

- Side B Coverage: Reimburses the organization when it indemnifies directors and officers

- Side C Coverage: Protects the entity itself, which is important for nonprofits facing organizational claims

Important policy features to evaluate include:

- Defense cost coverage (duty to defend vs reimbursement)

- Prior acts coverage for claims arising from past conduct

- Extended reporting period options, sometimes called tail coverage, that allow claims to be reported after the policy ends.

- Coverage for volunteers and committee members

- Whether employment practices liability is included or if coordination with a separate policy is required

D&O Insurance as Part of Nonprofit Risk Management

D&O insurance works best as part of a comprehensive risk management program. Additional insurance coverage can include:

- General liability insurance for bodily injury and property damage

- Employment practices liability insurance (EPLI) for employment claims

- Professional liability insurance for services provided

- Cyber liability for data breaches and other potential risks

- Crime or fidelity coverage for theft and fraud

Beyond insurance, strong governance practices reduce claims risk. Clear policies, documentation, and board training help prevent situations that lead to claims. Legal counsel for significant decisions and compliance matters provides guidance that helps avoid problems before they arise.

Find the Right Coverage with BIS Benefits

D&O insurance protects nonprofit directors, board members, and the organization itself from claims alleging mismanagement or wrongful acts. Volunteer status does not eliminate personal liability exposure, and even well-intentioned decisions can result in costly legal expenses. Even small nonprofits benefit from appropriate protection from a D&O plan.

Working with an experienced insurance broker helps ensure your leadership team and organization are properly protected. At BIS Benefits, we help Georgia organizations find

group health insurance and

commercial insurance solutions that fit their business’s unique needs.

Request a Quote to get in touch with one of our professionals today!