Large Group vs Small Group Health Insurance: What Employers Need to Know

Large Group vs Small Group Health Insurance: What Employers Need to Know

At a Glance: Small group health insurance typically offers simplified administration and community-based pricing but limited plan customization. Large group insurance provides greater flexibility and potential cost savings through experience rating, but requires complex compliance and administrative oversight. Crossing the 50-employee threshold triggers the Affordable Care Act (ACA) employer mandate, which opens up significantly more plan design options alongside increased regulatory responsibilities.

Choosing the right health insurance for your employees represents one of the most important decisions you'll make as an employer. The type of coverage you provide directly impacts your ability to attract and retain quality talent while managing your business's healthcare costs. However, many employers don't realize that their group size fundamentally determines not only what insurance options are available to them, but also their legal obligations, pricing structure, and administrative requirements.

Understanding the difference between small group and large group health insurance is crucial for making informed decisions about your employee benefits strategy. The distinction between small and large group health insurance affects everything from the benefits you must provide to how your premiums are calculated. As your business grows, these classifications can change, potentially opening up different coverage options.

What Defines a Small Group vs Large Group Plan

The classification of your business as either a “small group” or “large group” for health insurance purposes depends primarily on the number of full-time equivalent employees (FTEs) you have, though the exact thresholds can vary by state.

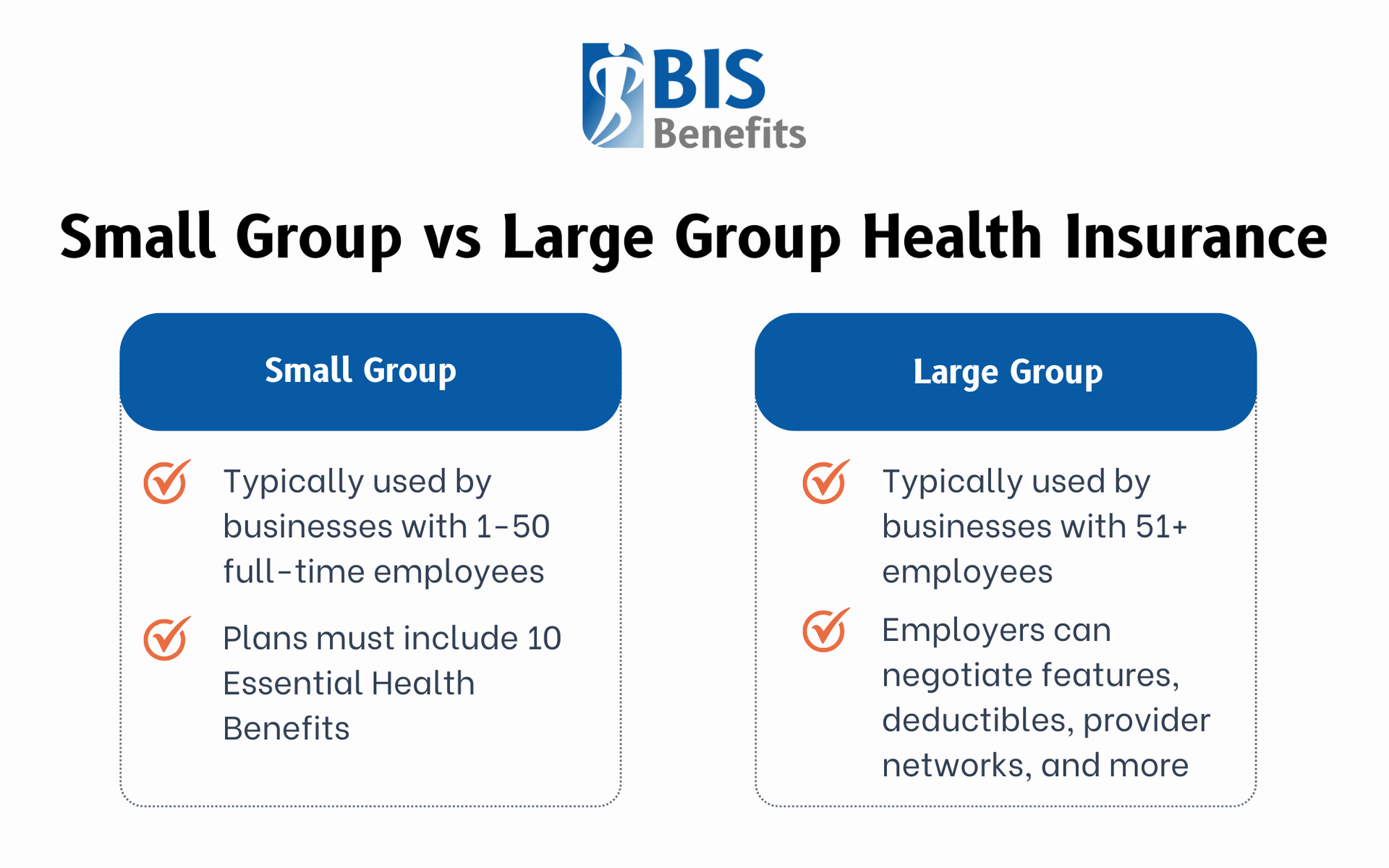

Small Group Classification

This typically includes businesses with 1-50 full-time employees. Full-time equivalent employees include both full-time workers and part-time employees whose combined hours equal full-time positions. For example, two employees working 20 hours per week would count as one FTE. This calculation becomes important when you're near the threshold, as seasonal fluctuations or part-time staffing changes can potentially shift your classification.

Large Group Classification

This generally applies to businesses with 51 or more full-time equivalent employees. Once you cross this threshold, you enter a different regulatory environment with distinct advantages and obligations. Large group status typically provides more flexibility in plan design but comes with increased compliance requirements and administrative complexity.

Some states set different thresholds or additional requirements for these classifications. It's essential to understand your specific state's regulations and how they impact your classification, since they can impact what options are available to your business.

Plan Design & Coverage Differences

The differences in plan design flexibility between small and large group health insurance are substantial and can significantly impact both employers and employees.

Small Group Requirements

Under the Affordable Care Act (ACA), these requirements are quite specific. Small group plans must include the 10 Essential Health Benefits, which cover services including:

Ambulatory patient services- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative services

- Laboratory services

- Preventive care

- Pediatric services, including vision and dental care

These requirements ensure comprehensive coverage but limit customization options. Small group plans typically offer standardized benefit designs with predetermined deductibles, copayments, and coinsurance levels. While this standardization provides consistency and makes plan comparison easier, it may not perfectly match your employees' specific needs or your budget constraints.

Large Group Flexibility

The ability to self-insure also becomes available to large groups, allowing them to assume the financial risk of their employees' healthcare costs rather than paying fixed premiums to an insurance company. With more employees to insure, large groups have greater leverage to negotiate favorable terms with insurance carriers. This allows for significantly more customization in plan design. Large groups can:

Negotiate custom features- Adjust deductibles and copayments

- Offer multiple plan options

- Select specific insurance provider networks

- Exclude certain benefits that aren't required by law

This flexibility enables large employers to create plans that better align with their workforce demographics and budget requirements. While this option requires careful consideration and professional management, it can provide significant cost savings for the right organizations.

Pricing & Rating Structure

The fundamental difference in how small and large group health insurance premiums are calculated can have dramatic impacts on your costs and budgeting predictability.

Small Group Community Rating

This means that premiums are based on community-wide factors rather than your specific group's health history. Insurance carriers consider factors like your employees' average age or geographic location, but they cannot adjust premiums based on your group's past claims experience or health status.

This community rating system provides several advantages for small groups. Businesses with older or less healthy employee populations aren't penalized with higher premiums, making health insurance coverage more accessible and predictable. However, community rating also means that healthier small groups may pay higher premiums than their actual risk would warrant.

Large Group Experience Rating

This allows insurance carriers to adjust premiums based on your group's actual claims history and health status. This means that groups with lower healthcare utilization and healthier employees can benefit from reduced premiums, while groups with higher claims may face increased costs.

Experience rating provides more direct control over premium costs through effective wellness programs, preventive care initiatives, and claims management. However, this can also cause increased volatility and potential for significant premium increases if your group experiences high claims.

Compliance & Administrative Impact

The regulatory burden and administrative requirements vary significantly between small and large group health insurance, with large groups facing substantially more complex obligations.

Small Group Compliance

Under the ACA, this is relatively straightforward. Small employers (under 50 FTEs) are not subject to the employer mandate and therefore don't face penalties for not offering health insurance. Small groups enjoy simplified reporting requirements with minimal IRS paperwork beyond basic tax filings.

Large Group Requirements

Large group coverage is substantially more complex. Once you reach 50 or more full-time equivalent employees, the ACA employer mandate kicks in, requiring you to offer affordable, minimum value health coverage to full-time employees or face potential penalties.

Large groups must navigate extensive reporting requirements. Compliance oversight for large groups includes potential IRS audits, Department of Labor investigations, and state insurance department reviews. The complexity increases further with

COBRA administration and

HIPAA compliance.

What Happens When A Business Grows Past 50 Employees?

Crossing the 50-employee threshold represents a significant milestone that triggers new obligations and opportunities requiring careful planning and preparation.

The Employer Mandate

This becomes effective for applicable employers once the business has 50 or more full-time equivalent employees, typically measured using a 12-month lookback period. This means you must offer affordable, minimum value health coverage to full-time employees or face potential penalties.

Plan Reassessment

As a small business transitions from community-rated to experience-rated pricing, the current small group plan may no longer be available. This requires you to evaluate new options for larger organizations that may have different provider networks, benefit structures, or cost-sharing arrangements.

Administrative Changes

Business infrastructure needs significant upgrading to handle large group compliance requirements. You'll need systems to track eligible employees, generate required reports, and manage the increased complexity of benefits administration.

Broker and Vendor Relationships

As your needs become more complex, you might need to transition to brokers with more sophisticated large group capabilities or consider working with a Professional Employer Organization (PEO) that can provide large group access and administrative support.

Tips for Choosing the Right Health Plan

Making the right health insurance decision requires careful consideration of your current situation and future growth plans.

Assess Employee Needs and Budget

You can evaluate these by conducting surveys or focus groups to understand what your employees value most in health benefits. Consider demographic factors like average age, family status, and income levels that might influence plan preferences.

Plan for Growth

If you're approaching the 50-employee threshold, consider how your benefits strategy will evolve as your business grows. Start preparing for the transition to large group status well in advance.

Explore Alternative Solutions

Other options, like PEOs, can provide access to large group pricing and administrative support even while you're still technically a small group.

Consider Total Compensation Strategy

Sometimes, investing in a more expensive health insurance plan can reduce pressure for salary increases or help attract higher-quality candidates. Evaluate how health benefits fit into your overall employee value proposition.

Work with Specialized Brokers

Small group specialists who understand your market segment and the community rating environment can help you navigate standardized plan options effectively. As you approach or exceed 50 employees, consider brokers with large group expertise.

Picking the Right Plan for Your Business with BIS Benefits

The decision between small and large group health insurance isn't just about current employee count. Employers must also understand how your choice aligns with your business strategy, growth plans, and employee needs. Small group plans offer simplicity and predictability, while large group plans provide flexibility and potential cost advantages for the right organizations.

As your business evolves, your health insurance strategy should evolve with it. Working with a knowledgeable health insurance agent who will honestly explain the differences between small and large group options can help you build a benefits strategy that grows with your business while keeping you compliant and competitive.

Don't let the wrong group classification leave you with less-than-optimal coverage or unnecessary compliance burdens. At BIS Benefits, we take the time to understand your workforce demographics, growth trajectory, and budget constraints to help you plan for whatever changes and transitions lie ahead. Whether you're approaching the 50-employee threshold or just looking for a more personalized brokerage experience, BIS will work with you to find the small group or large group health insurance plan that best serves your business.

If your business is located in the Metro Atlanta area, give us a call to find out what our Group Health Insurance brokerage services can do for you!