What Does Cyber Insurance Not Cover (And Why It Matters for Your Business)

What Does Cyber Insurance Not Cover (And Why It Matters for Your Business)

At a Glance: Cyber liability insurance provides valuable protection for data breaches, ransomware attacks, and business interruption, but it doesn't cover everything. These policies often exclude crime and theft, insider threats, contractual liability, regulatory fines, and reputational losses. Understanding these coverage gaps helps businesses build a complete risk management strategy that combines cyber insurance with strong cybersecurity practices and any necessary additional coverage.

Cyber insurance has become a critical component of modern business risk management, offering protection against the financial devastation that can follow a data breach or cyberattack. As cyber threats continue to evolve and multiply, more businesses are recognizing the importance of having cyber coverage in place. However, many business owners make a dangerous assumption: that cyber insurance provides comprehensive protection against all digital risks. This misconception can prove costly when a claim is denied due to policy exclusions or coverage gaps.

While these cyber insurance policies provide valuable protection in many scenarios, they also contain significant exclusions that could leave your business financially exposed when you need coverage most. Understanding what cyber insurance does and doesn't cover can help you build a more complete understanding of your protection and where you might need to fill the gaps.

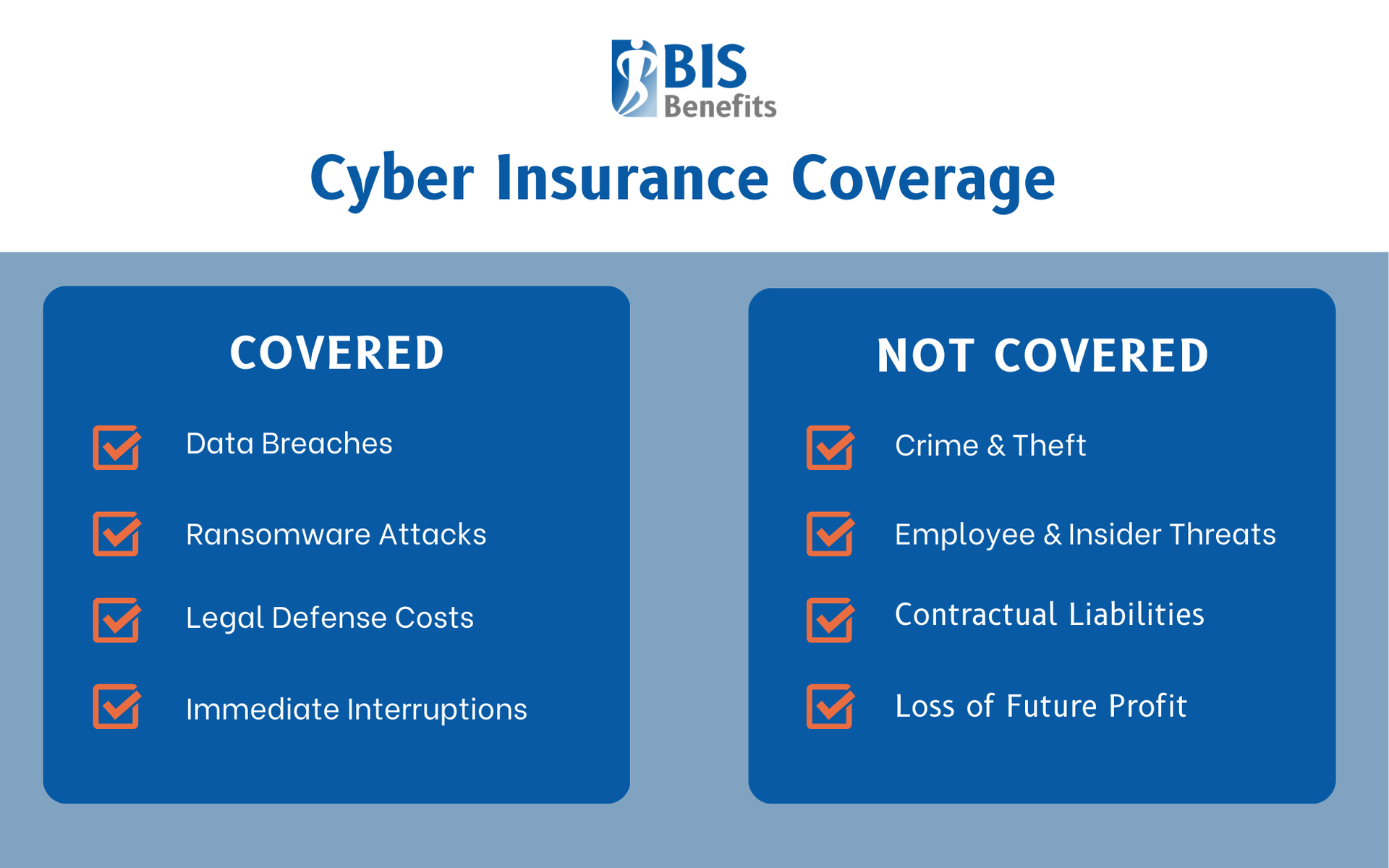

What Cyber Insurance Does Cover

Before examining the limitations, it's important to understand the valuable protections that cyber insurance typically provides. Most comprehensive cyber insurance policies cover several key areas that can help businesses recover from cyber incidents.

Data Breach Response

This represents one of the most fundamental cyber coverages, including the costs associated with notifying affected customers, regulatory bodies, and other stakeholders as required by law. This often extends to providing credit monitoring services for affected individuals, which can cost thousands of dollars per person over multiple years. The policy may also cover the expenses of hiring specialized forensic investigators to determine the scope and cause of the breach.

Ransomware Payments and Recovery

Coverage for these events has become increasingly important as these attacks surge across all business sectors. Cyber insurance can cover both the ransom payments themselves (where legally permitted) and the associated costs of data recovery, system restoration, and business interruption during the recovery period. These payments, both the initial amount and total recovery costs, can create substantial losses for businesses.

Business Interruption

In cyber insurance, this can replace lost income when your business operations are disrupted by covered cyber events. This might include lost revenue from website downtime, inability to process orders due to compromised systems, or operational delays while systems are restored. Some policies also cover extra expenses incurred to minimize business interruption, such as renting temporary equipment or hiring additional staff.

Legal Defense Costs

Legal fees tied to covered events can quickly escalate into high expenses, particularly when dealing with regulatory investigations or customer lawsuits following a data breach. Cyber insurance typically covers settlement payments, regulatory proceedings, and other legal expenses related to covered incidents.

What Cyber Insurance Does Not Cover

Despite these valuable protections, cyber insurance policies contain numerous exclusions that can surprise business owners when they need coverage most. Understanding these limitations is crucial for comprehensive risk management.

Crime & Theft

These are the most common exclusions to catch many businesses off guard. Insurers increasingly require policyholders to maintain basic security standards, such as encrypting sensitive data or intellectual property, implementing multi-factor authentication, and maintaining updated software. Claims may be denied if losses result from the failure to meet these security requirements, leaving businesses that haven't invested in proper cybersecurity infrastructure without coverage when they need it most. Businesses need a separate crime policy to cover ransomware attacks and other incidents of cyber crime.

Insider Threats and Employee Misconduct

If an employee intentionally steals data, commits fraud, or sabotages systems, traditional cyber policies may not respond. This exclusion is particularly concerning, especially for small businesses, given that insider threats account for a significant percentage of data breaches and security incidents.

Contractual Liability

If your business has contractual obligations with third parties to protect client data and faces liability for failing to meet those obligations, you may need separate professional liability or Errors & Omissions coverage.

Physical Injury and Property Damage

Even if these damages result from cyber incidents, they are still generally excluded from cyber policies. For example, if a cyber attack on a manufacturing facility causes physical damage to equipment or injures workers, cyber insurance likely won't cover these losses.

Fines and penalties present a gray area in many policies. While some cyber insurance policies cover certain regulatory fines, others exclude them entirely. The coverage often depends on whether the fines are considered "insurable" under applicable law, which varies by jurisdiction and type of violation.

Reputational Damage or Loss of Future Profit

While cyber insurance coverage policies may cover immediate financial losses from business interruption, they generally don't compensate for long-term revenue decline due to damaged customer trust or brand reputation following a cyber incident.

Why These Exclusions Matter

These coverage gaps matter significantly because small and medium-sized businesses often assume they're fully protected once they purchase cyber insurance. Many small businesses purchase a Business Owner's Policy (BOP), which can provide broad coverage for various aspects of their operations. However, a more general BOP policy will have lower limits, and a BOP’s cyber insurance provisions might not provide protection for several common cybersecurity issues.

This false sense of security can lead to inadequate risk management and devastating financial consequences when excluded events occur. Claims may be denied if basic security measures aren't in place, leaving businesses that view insurance as a substitute for proper cybersecurity without any protection at all. Discovering coverage gaps during an active incident, when your business is already under stress, is far too late to address these limitations. Businesses need to understand their policies thoroughly, asking specific questions about exclusions and requirements.

How to Protect Your Business Beyond the Policy

Given these limitations, businesses must implement comprehensive risk management strategies that extend beyond cyber insurance coverage.

Investing in Strong IT and Cybersecurity Systems

This forms the foundation of effective cyber risk management by implementing firewalls, intrusion detection systems, endpoint protection, and regular security updates. These investments not only improve your security posture but may also help satisfy insurance requirements and potentially reduce premiums.

Training Employees on Phishing & Secure Behavior

Employees are common targets for scammers looking to access a company's sensitive information. Regular training programs, simulated phishing exercises, and clear security policies help create a culture of cybersecurity awareness that can prevent many incidents from occurring.

Conducting Regular Risk Audits

These assessments should examine both technical systems and business processes, providing a comprehensive view of your cyber risk exposure to identify vulnerabilities before attackers do.

Exploring Add-On Coverages

Additional coverages can help fill gaps in your cyber liability policies. Technology errors and omissions insurance, property insurance, crime insurance, and specialized coverages for specific industries may provide financial protection where traditional cyber policies fall short.

Working with a Knowledgeable Broker

An experienced insurance broker who understands cyber risk and policy exclusions ensures you're making informed decisions about coverage. One of these professionals can help you navigate policy language, understand exclusions, and identify appropriate coverage limits for your business.

Building Comprehensive Protection

Cyber insurance provides valuable protection against many digital risks, but it's not a complete solution. Understanding what your policy does and doesn't cover enables you to build a comprehensive risk management strategy that combines insurance protection with strong cybersecurity practices and additional coverage where needed. In today's modern, increasingly digital landscape, this multi-layered approach is essential for business survival.

By taking a realistic view of cyber insurance limitations and implementing complementary risk management strategies, you can better protect your business against the ever-evolving landscape of cyber threats. Cyber insurance is an important tool in your risk management toolkit, but it is meant to work hand-in-hand with, not replace, strong cybersecurity practices and comprehensive business planning.

Find Cyber Insurance Protection That Covers Your Real Risks with BIS Benefits

A good cyber insurance broker will explain what standard policies don't cover and help you identify additional coverage options when appropriate. They should acknowledge when basic cyber policies have significant gaps that could leave your business exposed, helping you make informed decisions about comprehensive protection strategies.

At BIS Benefits, we take the time to understand your industry-specific cyber risks, regulatory requirements, and business vulnerabilities. Our team helps companies navigate the complex landscape of cyber insurance exclusions and create tailored strategies that provide adequate protection where standard policies fall short. We'll work with you to identify coverage gaps like insider threats or regulatory fines and explore solutions such as crime insurance or specialized

E&O coverage.

If your company is based in the Metro Atlanta area,

give us a call to find out what our

Business Insurance and

Cyber Liability brokerage services can do to protect your business from both covered and excluded cyber risks. Don't let policy exclusions leave you vulnerable when you need protection most.