A Guide to General Liability Insurance in Georgia

A Guide to General Liability Insurance in Georgia

At a Glance: General liability insurance protects Georgia businesses from third-party claims related to bodily injury, property damage, and personal injury that occur during normal operations. While Georgia does not have a statewide requirement for general liability coverage, many industries, local governments, and contracts require businesses to carry it.

A single accident at your business could result in a lawsuit that threatens your company's financial future. General liability insurance protects businesses from claims related to bodily injury and property damage that occur during normal business operations. It provides both legal defense and coverage for settlements or judgments.

While Georgia does not have a statewide requirement for general liability insurance, many industries, local governments, and contracts require businesses to carry coverage. Understanding what general liability insurance covers, when Georgia businesses need it, and how to obtain appropriate coverage helps protect your business assets from potentially devastating liability claims

What Is General Liability Insurance?

General liability insurance is coverage that protects businesses from third-party claims. Also called commercial general liability (CGL) insurance, it covers bodily injury, property damage, and personal injury claims arising from your business operations. This foundational coverage forms the basis of most business insurance programs and provides protection that businesses of all sizes need.

General liability has a straightforward process. Your business pays a premium for coverage. If a covered incident occurs, you file a claim with your insurer. The insurance company investigates the claim and provides legal defense if needed. The insurer pays settlements or judgments up to your policy limits, and your business is responsible for any deductible and amounts exceeding those limits.

What General Liability Covers

General liability insurance covers several types of claims:

- Bodily Injury Coverage: Applies when customers, vendors, or other third parties are injured on your premises or as a result of your operations.

- Property Damage Coverage: Pays when your business operations cause damage to someone else's property.

- Personal Injury Coverage: Covers medical bills for minor injuries regardless of fault and pays legal defense costs even if claims against your business are groundless.

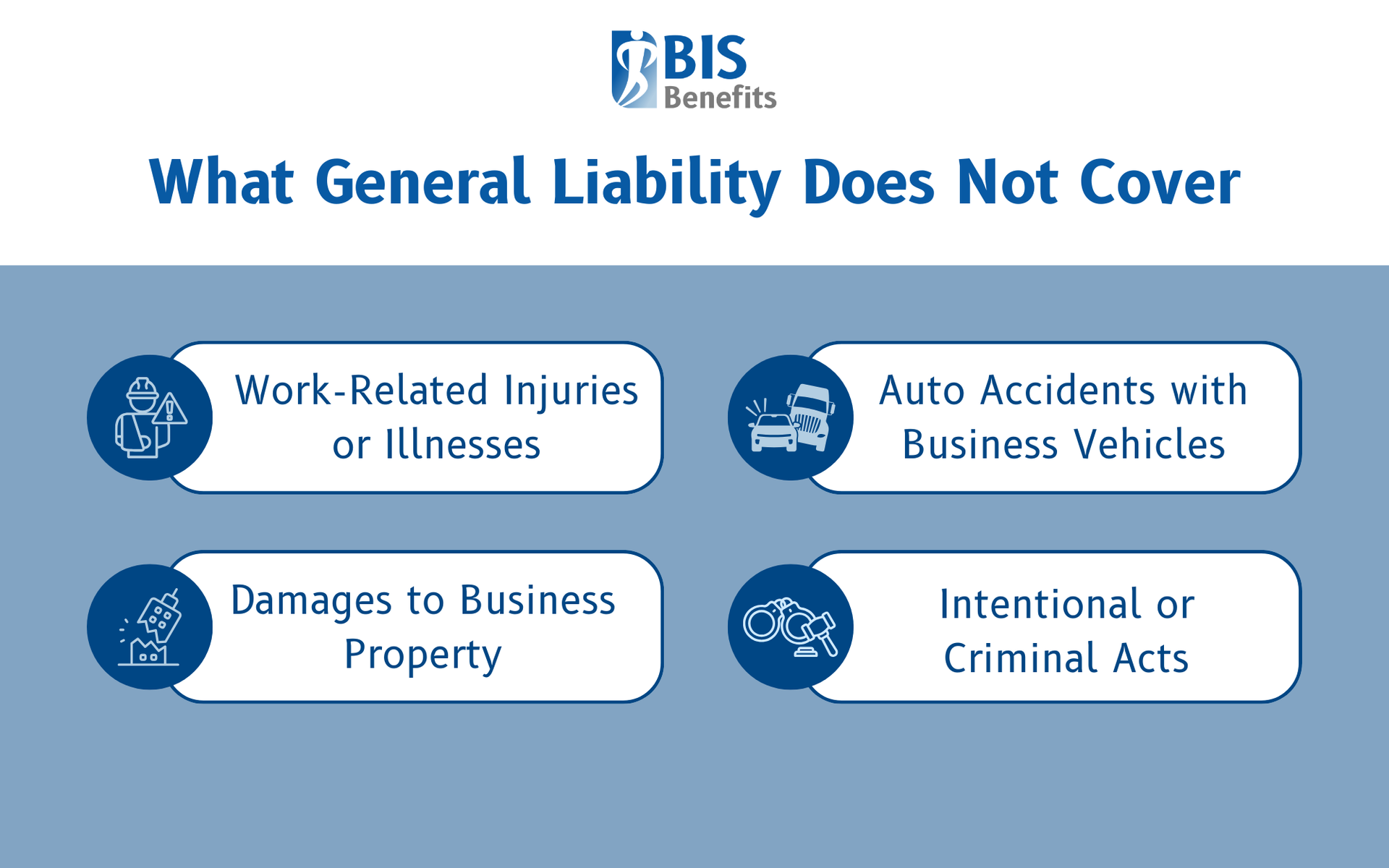

What General Liability Does Not Cover

When an employee experiences a work-related injury or illness, it is covered by workers' compensation, not general liability. Professional errors and omissions require separate professional liability coverage. Auto accidents need commercial auto insurance, and damage to your own property requires commercial property insurance. Intentional acts, criminal conduct, and employee discrimination claims are also excluded from general liability policies.

Georgia General Liability Insurance Requirements

Georgia does not require all businesses to carry general liability insurance. Business owners can legally operate without coverage if no other requirement applies to their situation. However, operating without coverage could expose your business to significant financial loss. A single liability claim could result in legal fees, settlements, or judgments that threaten your business assets and personal finances. Many situations effectively require coverage even without a statewide legal mandate.

Industry-Specific Requirements

- Licensed professions may require coverage as a condition of licensure.

- General contractors must meet Georgia state liability requirements.

- Subcontractors may also need coverage depending on their contracts with general contractors.

- Other regulated industries may have similar requirements, so checking with your licensing board is essential.

Local government requirements add another layer. Some Georgia cities and counties require general liability insurance as a condition for obtaining a business license. Requirements vary by municipality and business type, so checking with your local licensing office before starting operations is important. You may need to provide a certificate of insurance along with your business license application.

How Much General Liability Coverage Do Georgia Businesses Need?

The standard general liability plan for small businesses provides $1 million per occurrence and $2 million aggregate coverage. Per occurrence limits represent the maximum payout for any single claim, while aggregate limits cap the total payout during the policy period, typically one year. Both limits appear on your certificate of insurance. Understanding how they apply to multiple claims helps you evaluate whether standard limits are sufficient for your business.

Several factors affect how much coverage your business needs:

- The type of business and industry

- The number of employees and customers who interact with the business

- Annual revenue and contract values

- Business location and property exposure

- Any history of claims or lawsuits

Higher limits may be necessary in certain situations. Contracts with larger clients often specify minimum coverage requirements that exceed standard limits. High-value projects increase exposure and may warrant additional protection. Additionally, industries with significant liability exposure, such as construction or manufacturing, often need higher limits.

How to Get General Liability Insurance in Georgia

Working with an insurance agent or broker offers several advantages when obtaining general liability coverage. These professionals can compare quotes and coverage options across different insurance carriers. They also help identify appropriate coverage limits based on your operations and assist with certificates of insurance when contracts require proof of coverage. A local broker understands Georgia-specific requirements and coverage needs for businesses in different industries.

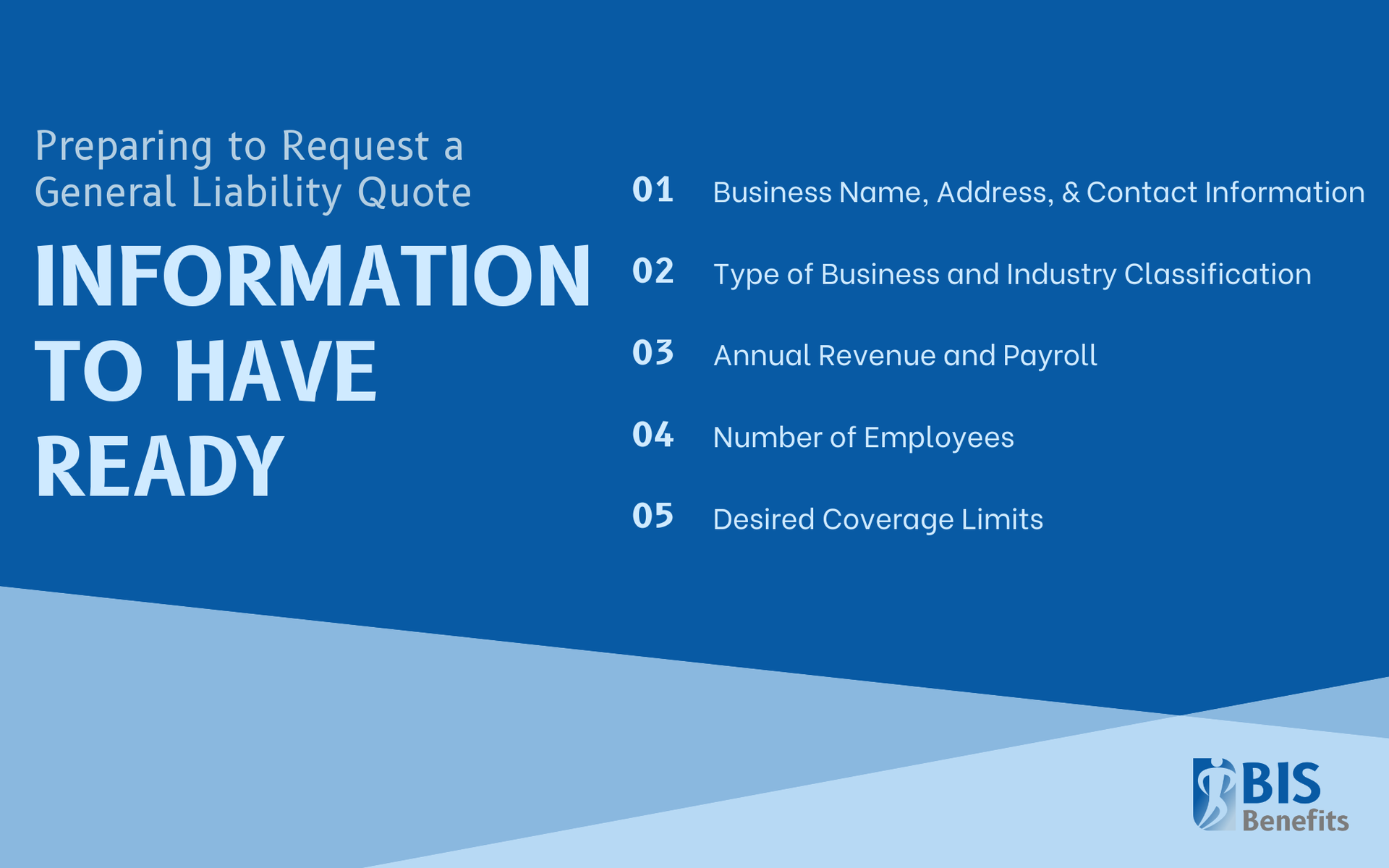

When requesting quotes, having this information ready speeds up the quote process:

- Business name, address, and contact information

- Type of business and industry classification

- Annual revenue and payroll

- Number of employees

- Description of your operations

- Desired coverage limits

When evaluating quotes and policies, compare coverage rather than just price:

- Review policy exclusions carefully to understand what is not covered

- Make sure you understand deductibles and how they apply to claims

- Check the insurer's financial strength and reputation through rating agencies and reviews

- Ask about the claims process and customer service to ensure you will receive support when you need it

Other Types of Business Insurance to Consider

General liability is foundational coverage, but most businesses need additional insurance types.

Workers' Compensation Insurance

Workers' comp is required in Georgia for employers with three or more employees and covers employee injuries on the job. This is separate from general liability insurance, and penalties apply for operating without required coverage.

Commercial Property Insurance

This insurance covers your business property and equipment, protecting against fire, theft, and other perils. This coverage is not included in general liability and is essential for businesses with physical assets like buildings, inventory, or equipment.

Commercial Auto Insurance

These policies cover vehicles used for business purposes. Personal auto policies often exclude business use, so separate commercial coverage is required for any business-owned vehicles.

Errors and Omissions Insurance (E&O)

E&O coverage, also called professional liability insurance, covers mistakes or negligence in professional services. This coverage is important for consultants, accountants, architects, and similar professions and is not covered by general liability.

Business Owner's Policy (BOP)

A BOP bundles general liability with commercial property coverage in a single policy. This package is often more affordable than purchasing separate policies and provides convenient coverage for small businesses with straightforward insurance needs.

Protect Your Georgia Business with a BIS Benefits Broker

General liability insurance protects Georgia businesses from claims related to bodily injury, property damage, and personal injury, providing essential coverage for legal defense and settlements. While Georgia does not mandate coverage statewide, many industries, including general contractors, local governments, and contracts require businesses to carry general liability insurance. Even when not legally required, general liability coverage protects your business assets from potentially devastating lawsuit costs.

The right general liability policy provides peace of mind and financial protection so you can focus on running your business. Working with an insurance professional can help you explore general liability plans and discover appropriate coverage options. BIS Benefits offers

general liability and more

business insurance options for Georgia-based companies that have at least 15 employees.

Request a Quote today to get in touch with our insurance brokers.